Address to Conference:

Network Pricing, VoLL Interconnection in the NEM

Melbourne, 29 September 1999

ENERGY PRICE PATHS

DEVELOPMENTS SINCE THE MARKETS BEGAN OPERATING

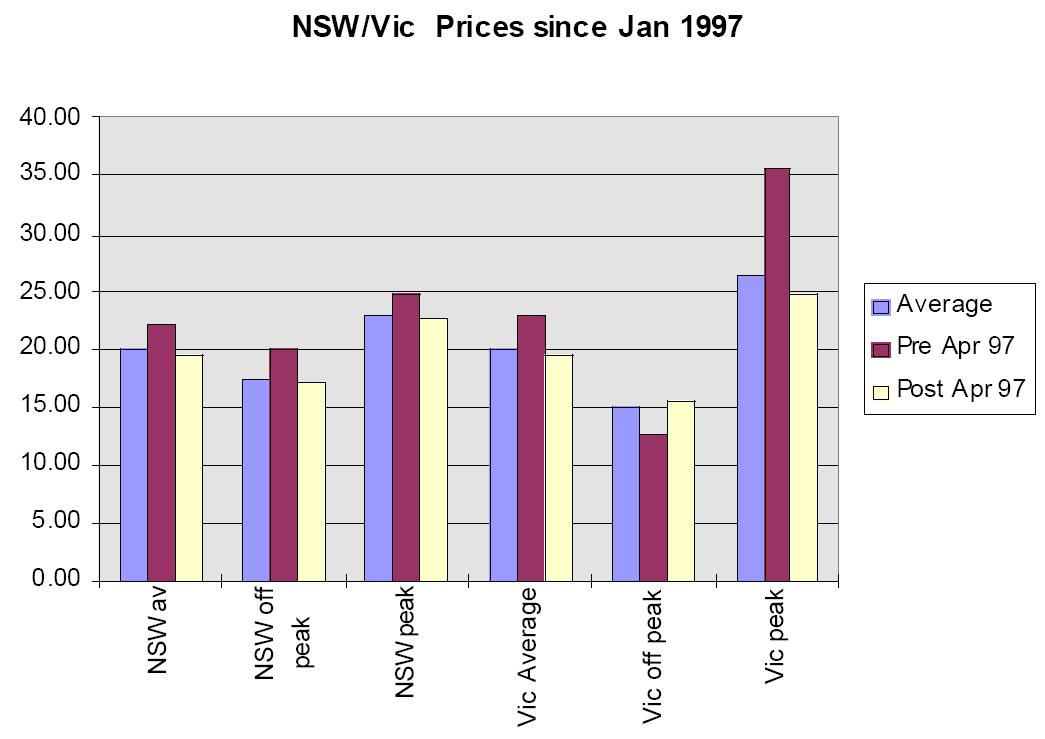

Most of us remember the confident forecasts of 1994 where the world's most prestigious consultancies estimated the shadow price of new generation at something like $38 per MWh. Those forecasts still haunt the smaller consumer as they are the basis of vesting contracts. As the following chart shows, average prices have been around $20.

The frustration of the generators at this level of pricing has not been relieved over time. The joining of the NSW and Vic markets reduced prices as the greater producer depth tended to reduce the incidences of price spikes. The one exception to this generally downward pressure was the Victorian off-peak prices where the interconnector allowed higher prices.

Chart 1

In reducing Victorian volatility, the link with NSW made an entrepreneurial Basslink, always a questionable proposition, even more remote. In Victoria, for example, there were almost as many days (16) when the average price was above $50 in the four months to April 1997 as there have been in the 27 months since. Basslink's viability, requires a volatile price to amortise the cost of the transmission line.

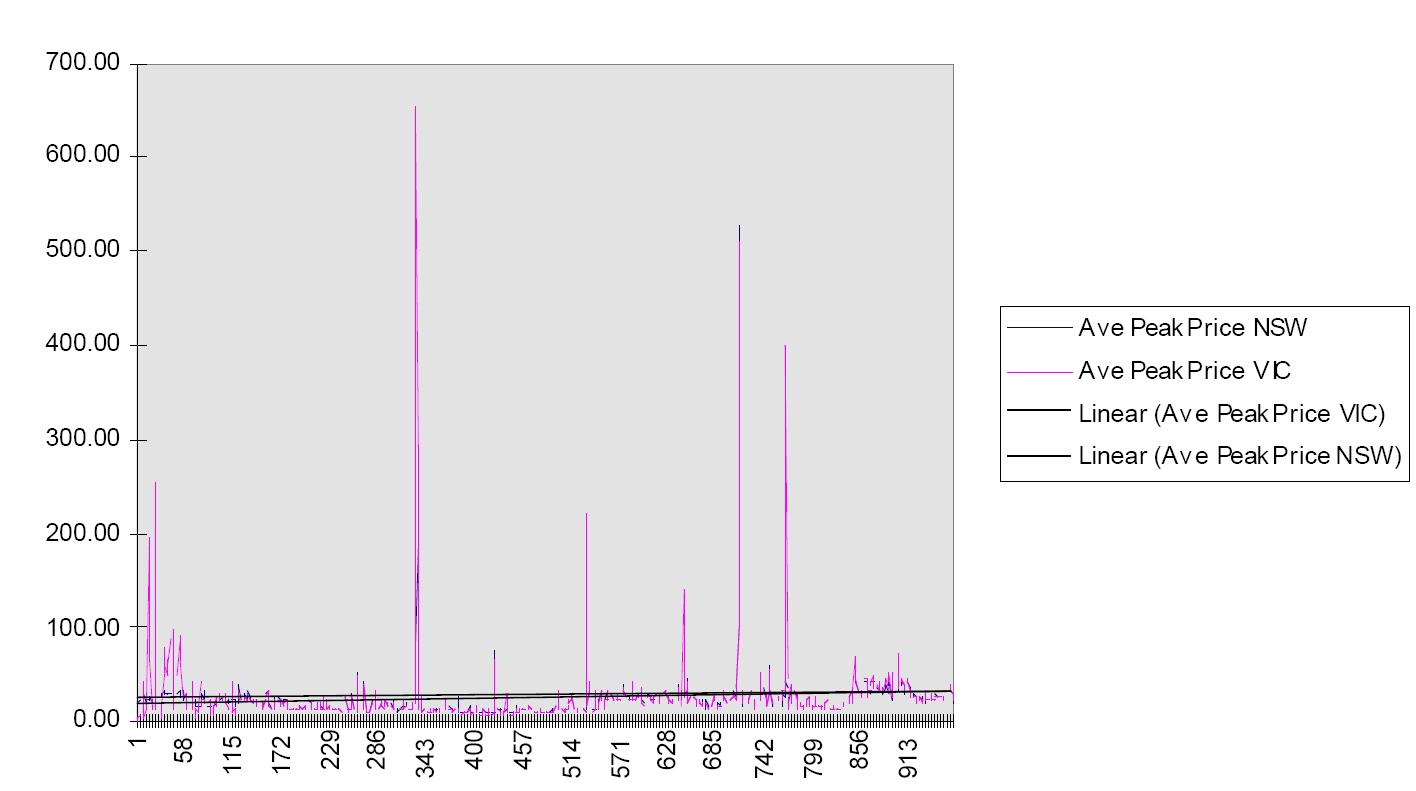

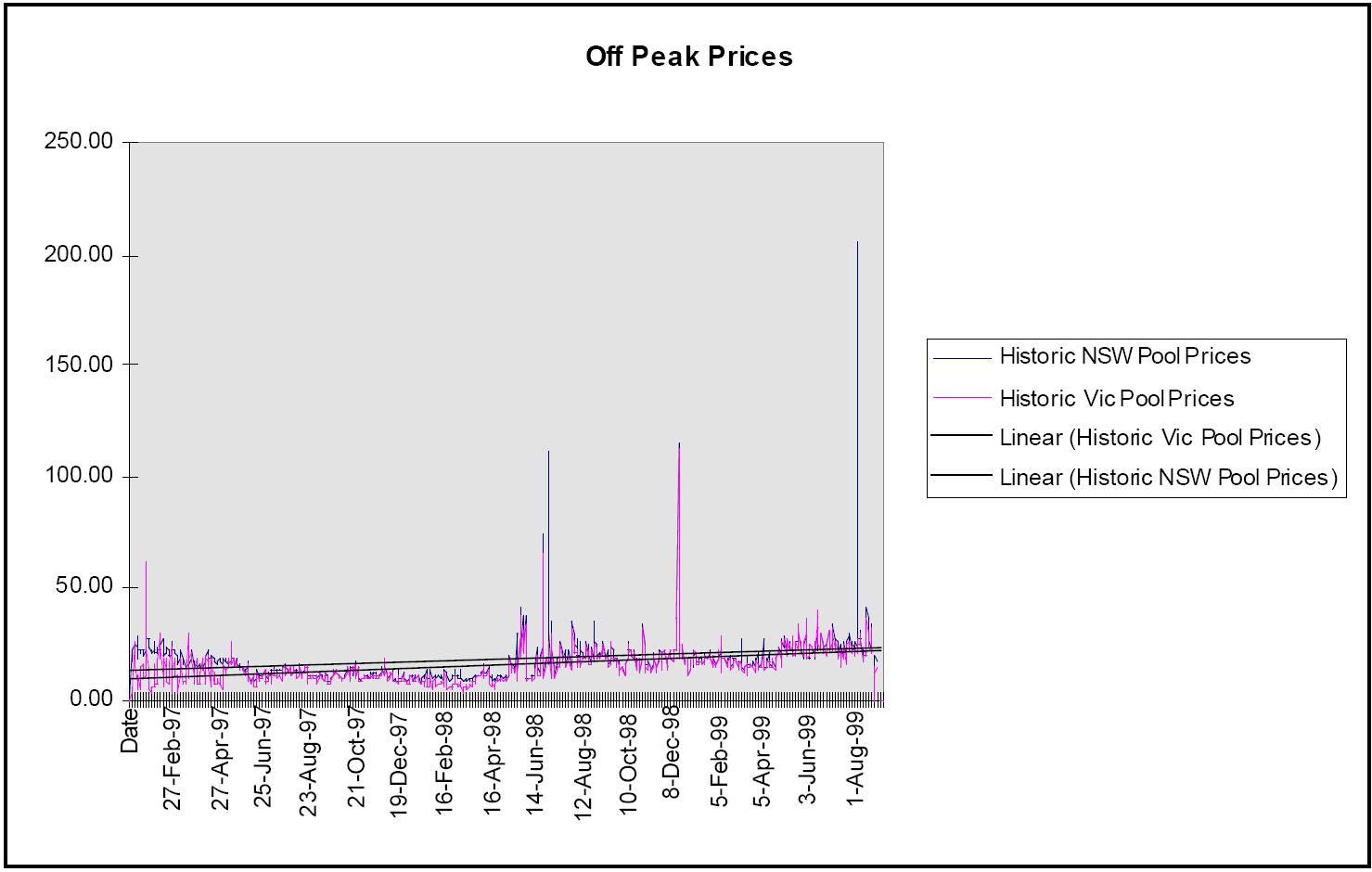

The following two charts show a relatively trendless electricity price trend.

Chart 2

Chart 3

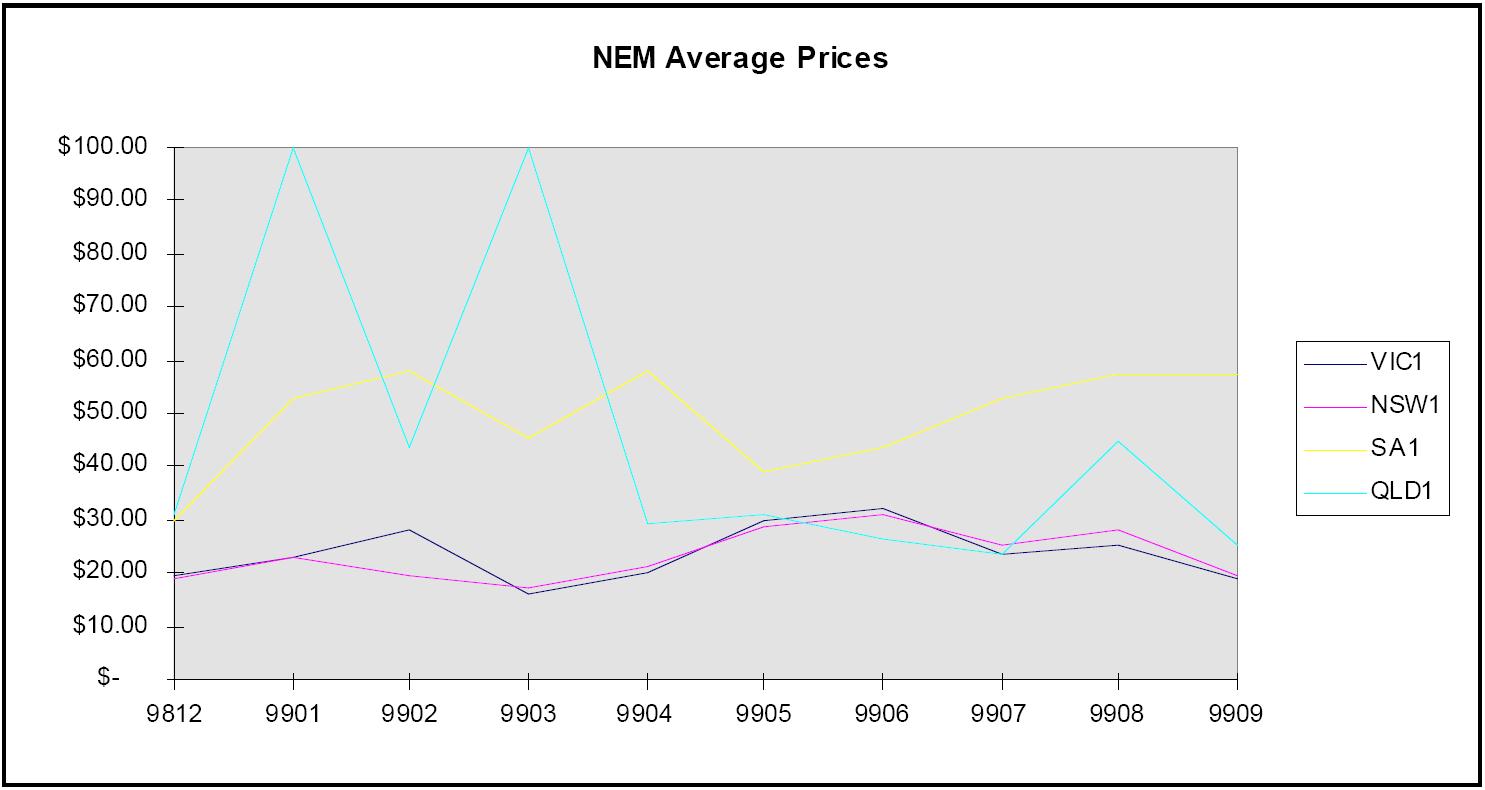

Prices in SA and Queensland have been far more volatile.

Chart 4

SA prices have been more than double those of the linked market and Queensland has been not much less.

FUTURE PRICE DEVELOPMENTS

Futures Markets

The Societe Generale one year forward data provides some useful market information. As can be seen in Chart 5, there is an optimistic and a less optimistic (realistic?) way of reading this data. A least squares regression has the market price trending towards a heady $35. A log curve has the market trending ever-so-slightly upwards.

Chart 5

Several developments have caused the price to shift. These include:

- a close to VoLL event in late November 1997, accompanying interconnector maintenance, which caused a repricing in the market, shifting the contract price up from about $18 to $22-26; as memories faded, the price drifted down again

- an upward shift in May 1998 as a result of the one year hedges from the early contestability tranche being renewed

- some increase in prices early this year which may have been due to the Pacific Power/Powercor dispute causing Pac Power to cease seeking contracts thus relieving pressure on the market. This period also coincided with an increase in the spot price possibly resulting from Pac Power being undercontracted and reducing its generation.

- a further softness in pool prices, reflected in lower contract prices, has taken place since June of this year as a result of AES Yarra (Ecogen) bidding more aggressively, presumably because it has access to take-or-pay gas. This softening of the market offset the effect on future contract prices of the ACCC forcing some reduction in the NSW vesting prices. (The lifting of VoLL is likely to have some effect but will not have an effect over the next two years.)

The trends in these prices reflects the reality of an over-supplied market. The Victorian generators claim the state owned nature of the NSW generators causes them to bid on a market share rather than profit maximising fashion. There may be something in this but the overwhelming cause of the low prices is excess capacity.

Planned Capacity and Future Prices

Major new licks of capacity in SA are in train with Pelican Point, Osborne 2 and the Transenergie link. These should bring the price down somewhat as they start to come on line in about a year's time, though SA is always likely to be higher priced than other states. That would doubtless be the major incentive for an entrepreneurial interconnect and Pelican Point may have been encouraged by especially low gas prices.

Queensland has both PNG gas looking for a market and some of the lowest cost coal available anywhere. The ESAA's survey of new power stations counts some 2,400 Megawatts of gasfired and 4,690 Megawatts of coal-fired electricity planned between now and 2003. That's getting close to the existing generation capacity in the State. Obviously it won't all go ahead in the time frame but there is a coming glut.

These developments have a bearing on price trends. The SG prices appear to have been ratchetting-up but only to the dizzy heights of $25-30! The link between NSW and Queensland may bring some price increase in the period prior to the latter part of the year 2000 -- even though it is less than 200 MW, as can be seen in Victoria with Newport generating, the price is often quite sensitive to small additional supplies. However this is likely to be short-lived if the avalanche of new capacity in Queensland eventuates. The more substantial regulated link between NSW and Queensland in 2001 seems likely to result in power moving south from an over-supplied Queensland market. Even so, notwithstanding a renewed price softening over the past month or so, it does not look like we'll plumb the price depths we saw a year and a half ago, possibly because some contracts for unwanted coal have expired.

MARKET STRUCTURE REGULATION

The First Steps

The general pattern of electricity restructuring involving the three way split:generation, transmission, and distribution was adopted worldwide.

Shifting from the nationalised or government franchised industry this was appropriate as the first stage. But we do not know whether energy suppliers are better run in an integrated or disaggregated fashion. Probably there is no one answer and, we should not try to impose a particular structure. It would seem that there are strong incentives on firms to integrate backward and forward to internalise risk. There is also some production specialisations that require markedly different skills of retailing, generating and distribution.

Privatisation

The process of unwinding government ownership in the industry has not yet reached the halfway stage. SA treasurer Rob Lucas has offered compelling reasons about why a Minister/shareholder cannot efficiently operate with rival businesses -- he knows that the strategies of one of his charges will adversely impact on others. It is impossible to apply strategic direction with such conflicts and the businesses become driven by the interests of the executives rather than attempting to maximise the wealth of the shareholders.

Beyond Privatisation

Assuming privatisation proceeds, how is the industry's structure to develop?

Crucial to this question are the relative efficiencies of producing in-house (integrated production) and contracting or selling through a production chain, together with the attitudes of the regulatory authorities. The ACCC is crucial to the latter question. The indications of its attitude to a proposed merger is normally final -- its position is seldom contested because of the costs and delay inherent in taking court action.

The ACCC applies a version of the Herfindahl-Hirschman Index. It may be "concerned" about a merger proposal where 70% of the market is held by the four largest firms with the merged firm to supply at least 15%; or where the merged entity is 40% of the market. These guidelines are similar to but somewhat more stringent than those of the US and Canada.

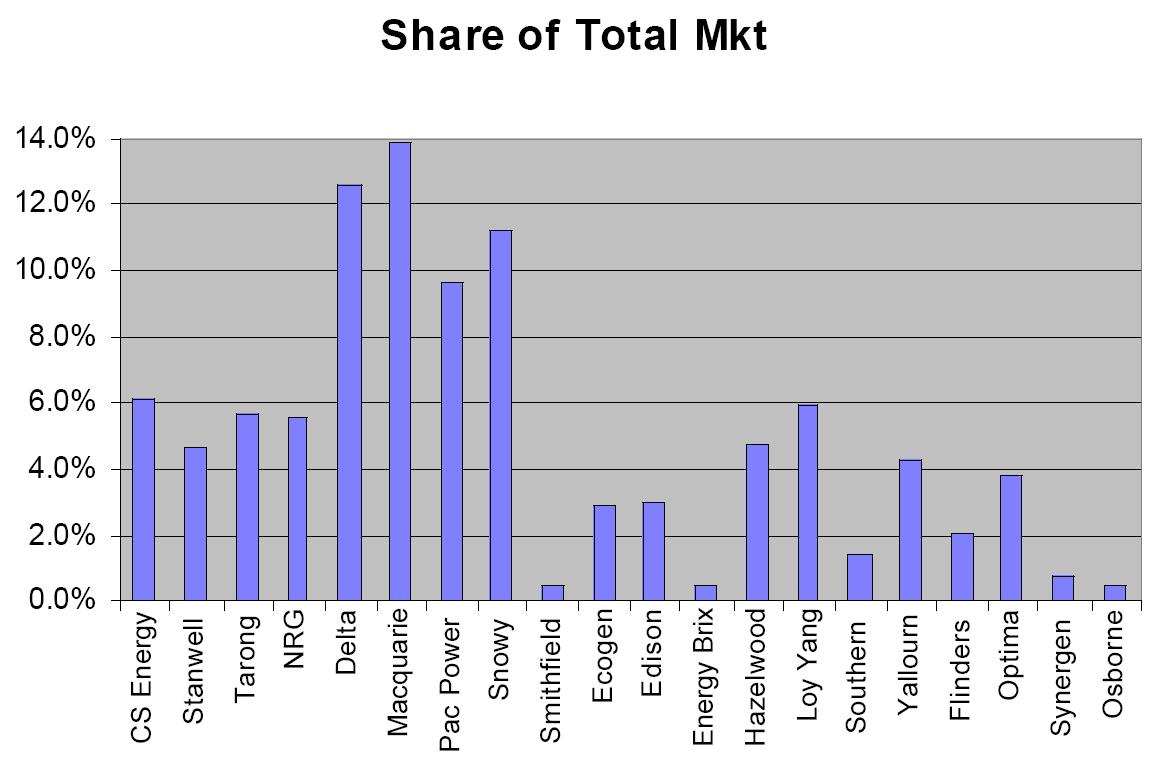

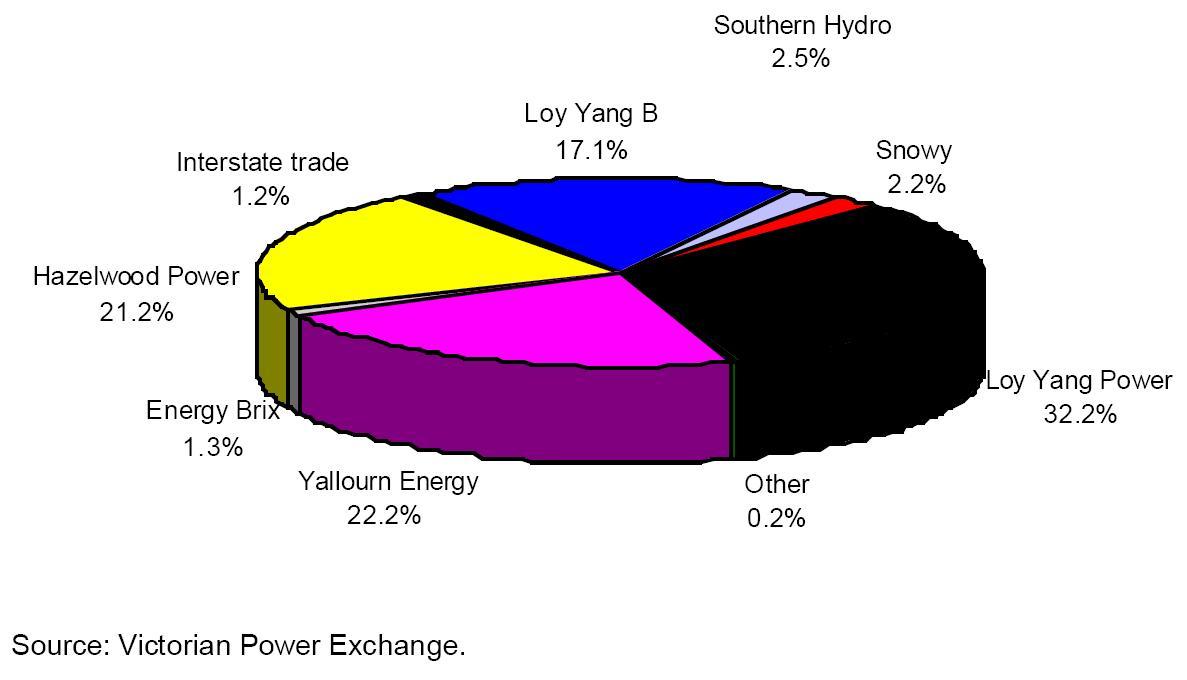

The ACCC has made some specific comments on electricity. Its merger guidelines say that an example of pro-competitive restructuring being undone would be the re-amalgamation of the five Victorian generators. That is clearly a very remote possibility (even so, the five firms concerned would comprise only 29% of the linked market).

In the past, the ACCC has often taken state markets as its frame of reference, even in areas like banking where the market is far from regional. Its statements on electricity may indicate a view that the national market is -- or was -- insufficiently connected. On a state based market, it is unlikely that two significant suppliers would be allowed to merge. In Victoria, any two of Yallourn, Mission, Loy Yang and Hazelwood would approach or exceed 40% of the market. It's also probable that merger attempts between Snowy, Southern Hydro and Newport would be heavily scrutinised in view of their combined importance to the peak market. The existing concentration in Victoria would bring any purchase by one of the big four outside of the ACCC's safe harbour provisions. Similar considerations would prevail in other states.

The UK experience has coloured a great many views on market power. The ability of the two majors there to hold prices higher than was considered to be a likely outcome under a fully competitive system continues to have a bearing on the regulatory arrangements in the England and Wales market. Even though the duopoly is now a triopoly with the growth of Eastern (TUA) as a generator, the authorities consider prices have been manipulated, although not through direct collusion.

But such sustained manipulation in a market without entry barriers is difficult to explain. And the increased capacity outside of National Power and PowerGen is a predictable market response and one that undermines any market power -- the profitable opportunities caused by high prices sucks in new capacity. Even so, the Australian competition authorities, like those in most other countries, are rarely impressed by claims that markets self-correct at lower cost than those imposed by their own interventions. In Australia, the ACCC has blocked or amended mergers in industries without entry barriers. These have included merger proposals in paints, banking, and the Australian Stock Exchange/Australian Futures proposal.

There would seem to be less justification for ACCC objection to interstate mergers. However, a merger between a major Victorian generator and one of the three major NSW generators could easily fall outside the ACCC's "safe harbour" guidelines, especially if the nature of the power were broken down into fast start, baseload etc. Similar considerations may apply if one of the Victorian or NSW generators were to seek to buy South Australia's Optima or even Northern power stations.

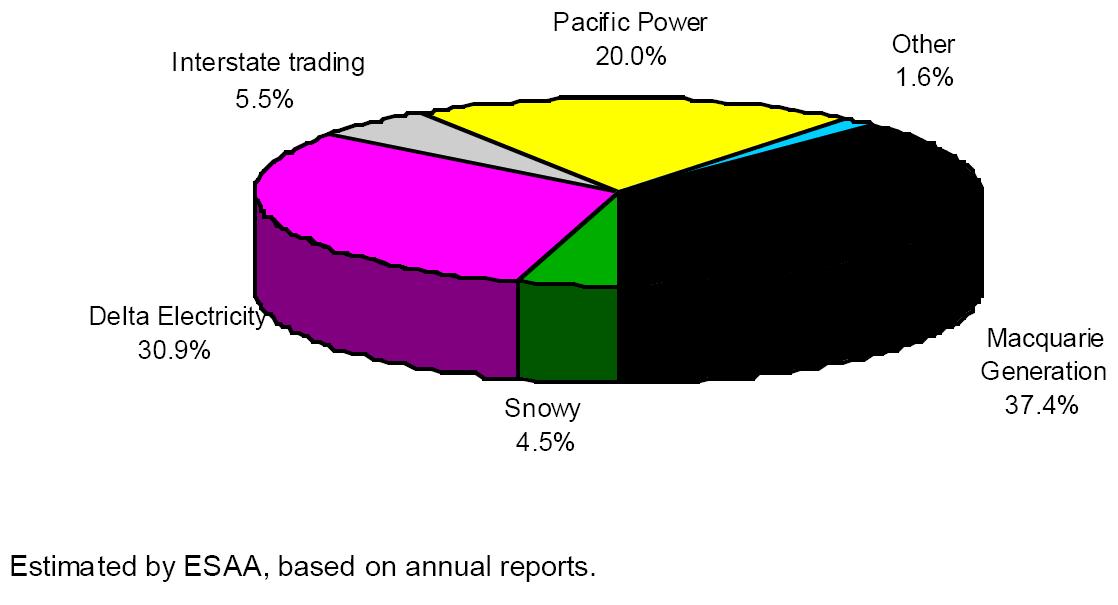

The ACCC has raised specific concerns about mergers in its authorisation of the NEM. In what, in the light of the low prices, reads like a sardonic statement, it drew off ABARE work to suggest that the excessive concentration in NSW could lead to "strategic" bidding. But the ACCC does had a point here. Even though there has been no sign of collusion, even of a non-overt kind, it would have been better to have started with a greater NSW disaggregation -- and such an approach is still possible prior to the NSW privatisation.

With regard to vertical integration, the ACCC NEM authorisation also expressed concern about generating businesses operating within retailing. This already occurs without any known adverse effects. However the ACCC may look closely on a more full-blooded integration. Some sort of indication of the ACCC's attitudes to mergers across and within sectors of the industry would be most helpful.

REGULATION OF THE "ESSENTIAL FACILITIES"

At the present time the area of regulation that occupies most of the industry's resources concern "essential facilities" -- the poles and wires. Both within the States and nationally, Australia's regulatory arrangements in these areas have been particularly intrusive. In contrast to the formalised processes for declaring that facilities must be opened to competitors and price fixing, some countries -- NZ and Germany for examplehave no specific regulation and simply rely on general competition law, backed up by the ability to by-pass.

In Australia, even where by-pass is clearly evident, as in Victoria's Docklands, the regulator is reluctant to leave things to market forces.

In terms of the outcome of reviews of price applications, the following itemises those that are presently available

Regulatory Inquiries and Outcomes

| ISSUE | REGULATOR | APPLICANT CHARGE | DETERMINED CHARGE | DATE |

| AGL gas contract market | IPART | Annual revenue reduction from $140m to $128m | Annual revenue reduction to $99m | May 1997 |

| Vic gas | ACCC/ORG | 9.7-10.2 return post tax | 7.75% return post tax | Oct 1998 |

| Wagga gas (GSN) | IPART | Original 11.1% later offer 9.0% | 7.75% | March 1999 |

| Telstra Interconnect | ACCC | 4.7c/minute | 2.0c/min. with 1.6c suggested Sept 1999 | June 1999 |

| Adelaide Airport | ACCC | 8.89% pre-tax or $3.66/ passenger | 8.25% pre-tax or $3.45/ passenger | June 1999 |

| Albury gas | IPART | 9.6% | 7.75% | July 1999 |

| NSW vesting contracts | ACCC | 43.64 cents | no more than 40 cents | Sept 1999 |

| NSW distribution prices | IPART | 8% average real price reduction 1999-2004 8.2-8.7% real pre-tax WACC (April 1999) | 16% real price reduction 1999-2004 7.5% (7.75% AIE, AE) 15% O&M reductions (10% AE, 5% AIE) | Sept 1999 Draft Determination |

Many of us will have waded through the material and attended the meetings behind these decisions. We know how resource intensive they are. In terms of outcomes, the authorities are moving towards a consistency, currently 7.75% but perhaps in the light of the latest IPART decision, trending down. Two major shortcomings of this approach are:

- the intrusive nature of intervention brings an insecurity over the stability of a decision. Dr Stephen Littlechild, formerly the UK electricity regulator, has discussed the re-opening of the England and Wales regulated tariffs after the 1994 price setting. Originally, the UK distribution rates were cut by between 11 and 17 per cent and an X factor established at 2 per cent per annum. A readjustment was sparked by public criticism that these measures offered excessive gains to the regulated businesses, evidence for which was provided by a steep rise in their market values. The tariff levels were subsequently adjusted down by a further 9 per cent compared to the rates set only some six months previously and a 3 per cent X factor was imposed. Dr Littlechild stressed that although regulators are intended to be independent of Government, they cannot be oblivious to the same pressures that impact upon Government in determining the just price.

- the setting itself is asymmetrical. If the regulator sets the price too high, the market provides the necessary discipline because the line is by-passed and, as a result, the owner will discount the regulated price. If the price is set too low, its sunk cost nature means it will not be withdrawn but:

- there is less incentive to ensure optimal maintenance levels, upgrade the line and offer premium services;

- there is a considerable disincentive to building new lines, a disincentive that has been attributed to underbuilding in US transmission, where since FERC Order 888 required open access, new transmission building has fallen 46 %.

CONCLUDING COMMENTS

In general price outcomes in the Australian electricity markets have been understandable, if not predicted.

Shortage of capacity in Queensland has shown the state, long considered to be the lowest cost generator, to be high priced ass a result of too little new capacity over recent years.

Higher prices in SA are prompting their own self-correction. Docklands demonstrates that a DB cannot seek higher prices than those a rival could provide the service for as long as by-pass is permitted.

Most discussion in the Australian energy industries has centred around issues of how to make the market work and how to prevent market power from having adverse effects on customers. But the upshot of all this is a considerable increase in regulatory oversight and resources allocated to persuade the regulators.

It is time to start a regulatory disengagement in this industry. The alternative is an industry that is regulator rather than customer focussed and one with a structure determined by the preferences of regulators rather than efficiency.

No comments:

Post a Comment