Backgrounders

Until the advent of the Financial Services Reform Act, ethical investment had been a matter of free choice. Investors were free to choose those products that suited their values, and indeed their financial needs. This is no longer the case.

The new Act imposes disclosure obligations on superannuation, life insurance and managed funds which will, in effect, force them to inquire into the labour, environmental, social and ethical standards of the Australian corporate sector.

Those obligations will impose values on investors and the industry to the detriment of financial return. The values to be applied are vague and not of a kind that can or should be enforced by government in a liberal society.

The Act will provide a means for intrusion by numerous political and anti-business interest groups into the already heavily regulated operations of Australian companies.

The rights of shareholders will be diminished at the behest of groups that are self-appointed and bear no risk of loss.

The Act is a threat to the future of the majority of Australian investors. Most Australians now look to funding their retirement from the savings invested in superannuation. The Act, by inducing trustees and other fiduciaries to pursue non-financial goals and the interests of people other than the unit-holder, can be expected significantly to undermine the returns in superannuation funds.

The Act is a thoroughly bad piece of legislation and the parts that pertain to reporting labour, environmental, ethical and social standards should be repealed.

"It is a general popular error to imagine the loudest complainers for the public to be the most anxious for its welfare"

Edmund Burke 1769

INTRODUCTION

On 27 September 2001, Parliament passed the Financial Services Reform Bill into the Corporations Law.

New disclosure provisions now apply to any offer of financial products, such as superannuation, managed investment and life insurance. Those provisions are very extensive and are designed to give prospective investors sufficient financial information to decide whether or not to invest.

Late in the process of drafting, a disclosure requirement of an unusual kind was added to the Bill. This covered matters unrelated to the financial and contractual terms of the products. It imposed reporting obligations for labour standards and environmental, social and ethical considerations -- that is, general behavioural standards.

If these obligations could be limited to those funds that freely choose without coercion to apply them, there would be no concern. Indeed it would make a substantial contribution to a better informed investing public and offer protection from fraud and potential loss of money.

However, it will not, and probably cannot, be quarantined and will extend beyond its immediate legislative ambit. It has potentially far-reaching effects on the corporate sector as a whole through the allocation of the funds managed by financial institutions. Moreover, it is a manifestation of a much wider movement, whose aim is to force acceptance of activist agendas by business -- at the expense of business and their shareholders.

The provision applies particular disclosure requirements to all superannuation, life insurance and managed investment products. It is thus imposed on approximately $650 billion of Australian savings, including the principal government-enforced form of savings -- superannuation.

This is the first codification of the so-called "triple bottom line". For the first time, the Government is helping to enforce the political agendas of the multitude of activist and essentially anti-capitalist Non Government Organisations (NGOs). Few of these NGOs are concerned with the financial health of the funds or of the business sector, nor are their goals aligned to those of shareholders or the majority of Australians whose future depends upon returns in superannuation funds.

THE ACT

The Financial Services Reform Act 2001 is almost 600 pages long and covers vital areas of licensing and conduct of financial institutions. It also places extensive obligations on providers of retail financial products to make product disclosure statements for such products (Section 1012A). (1)

While prudential regulation is appropriate for a sector which controls a significant proportion of the savings of the general public, the regulations imposed by the Act are excessive. It not only seeks to cover every eventuality, but greatly enlarges the exercise of bureaucratic discretion and the uncertainties and risks of investing.

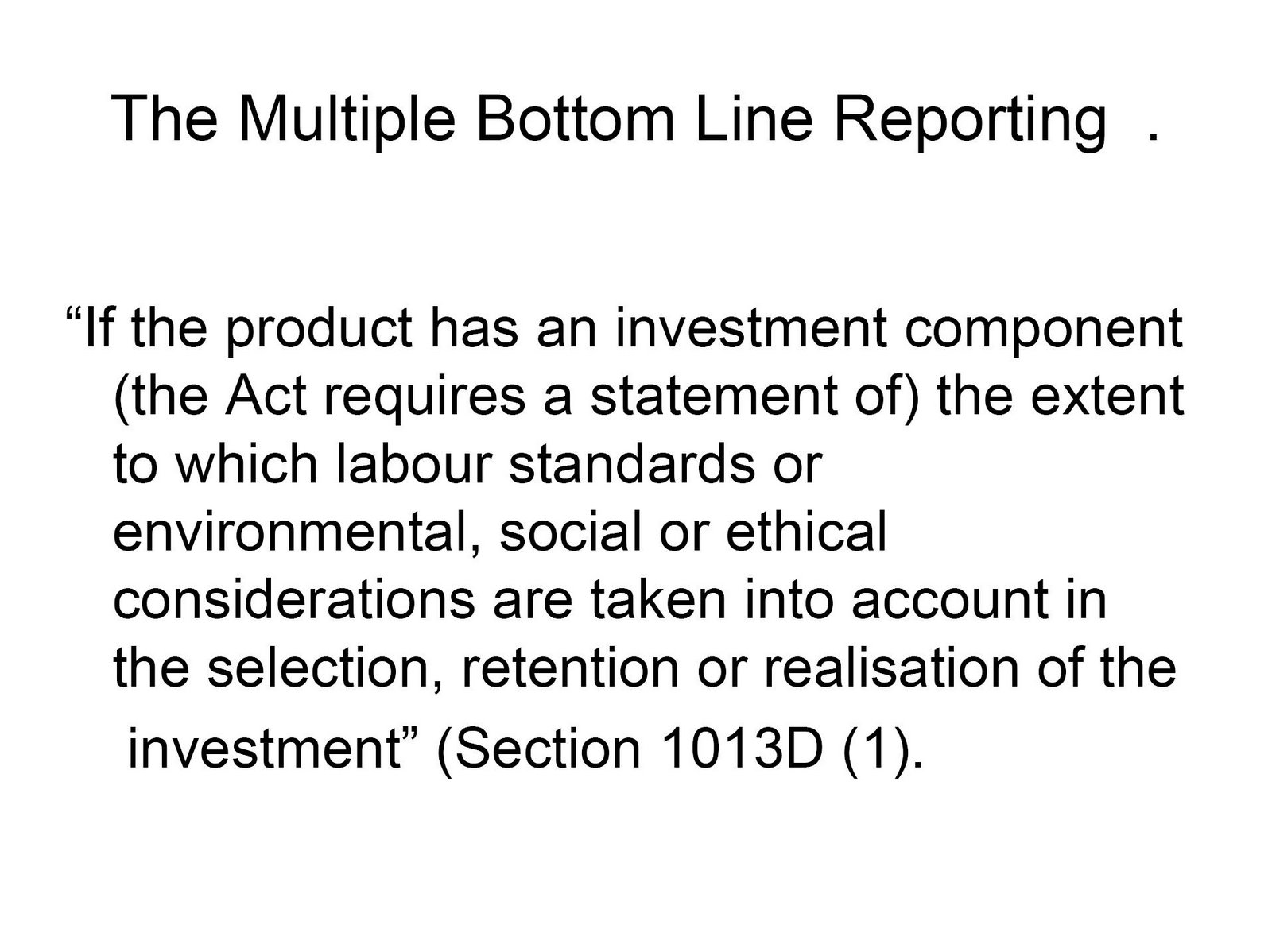

Nowhere is this more evident than in the novel provision relating to disclosure of non-financial considerations. Regulations accompanying the Act oblige the financial institution to state whether it takes the specified non-financial matters into account. "If the product has an investment component (the Act requires a statement of) the extent to which labour standards or environmental, social or ethical considerations are taken into account in the selection, retention or realisation of the investment" (Section 1013D (1).

THE PRACTICAL IMPLICATIONS FOR BUSINESS

At first sight, the legislation might appear relatively innocuous. Who could object to disclosure on labour, environmental, social and ethical matters? No doubt the Minister was persuaded that the amendment was harmless and would even aid "transparency" -- a key policy buzzword.

Upon closer examination, however, the legislation is much more intrusive than it seems. And the transparency is more apparent than real.

In practical terms, disclosure requires the institution to formulate and express its attitudes and practices to four matters which range from difficult to impossible to define.

In theory, businesses could state that they do not take these matters into account in their investment decisions and avoid scrutiny and the subsequent paper chase that will accompany disclosure. In practice, however, no institution will state that it does not take such matters into account, in part because if it did, pressure groups and the media would label it as unethical or anti-social. Silence would be treated as guilt.

In any case, it is also a reality of business that those matters are almost always "taken into account" in some degree, so a nil return would, in most cases, be misleading. The normal investment selection processes will involve winnowing out from corporate practices fraudulent (that is, unethical) propositions or those with high risk exposures. "Taking into account" is vague enough to embrace even the most casual process, let alone normal vigilance.

It is also theoretically open to institutions to be selective among the four matters and choose or discard one or more of them. For the reasons outlined in the preceding paragraphs, this is not a real option. Moreover, omitting any matter would involve a lengthy explanation of the omission, equivalent to that accompanying the product statement for those matters left in. There would be no point.

In short, the legislation gives the pretence of voluntarism but not the reality. And it goes well beyond mere reporting.

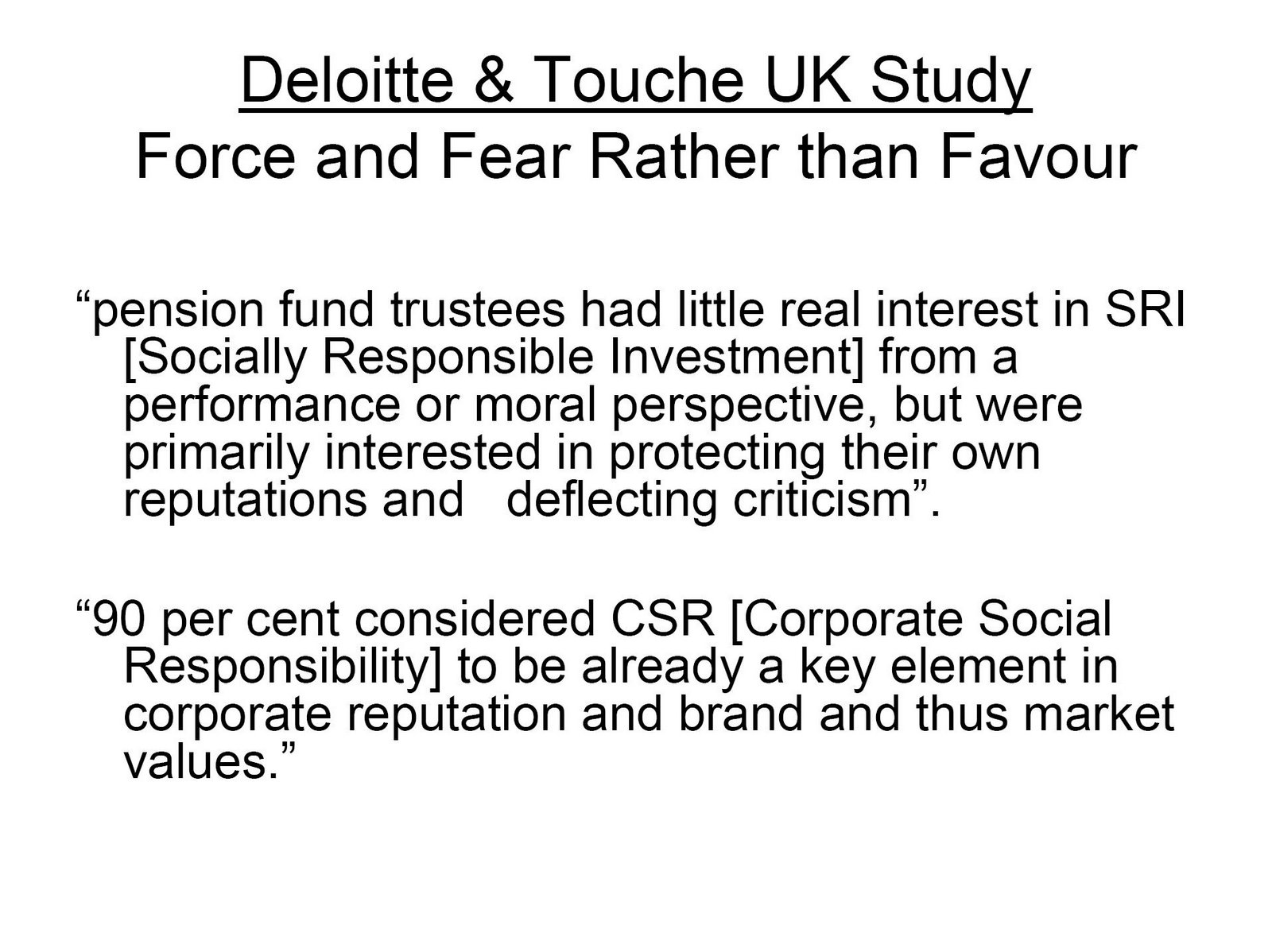

If proof were needed of the likely impact, we can turn to the UK where similar, though much milder, legislation came into effect two years ago. According to studies, "pension fund trustees had little real interest in SRI [Socially Responsible Investment] from a performance or moral perspective, but were primarily interested in protecting their own reputations and deflecting criticism". However, "90 per cent considered CSR [Corporate Social Responsibility] to be already a key element in corporate reputation and brand and thus market values. More than 50 per cent thought that CSR would be a significantly important part of investment decision-making within three years". (2) In short, the UK trustees are being forced in large number to pursue SRI, not by the commercial logic of SRI itself or by the interest of their unit-holders, but rather by the desire to protect their good names from attack by SRI activists. Additional costs are being generated for internal and external advice and monitoring. Despite this, funds are being criticised for poor practice and inadequate measurement of performance before the legislation has had time to bed down. The threat of more intrusive regulation is already being made.

THE EXTENSION OF STATE AND THIRD-PARTY

CONTROL AT FOUR LEVELS

The Act extends state control and third-party interference at four levels.

First, the Act requires the Australian Securities and Investment Corporation (ASIC) to produce regulations that define extra-legal social, environmental, labour and ethical standards. ASIC will be required to spell out performance standards on a wide range of issues which go far beyond the standards currently deemed appropriate by the Australian parliaments. In short, ASIC rather than Parliament will be required to write law, something that is profoundly undemocratic.

Second, trustees and managers of investment funds will be required to define and then disclose the extent to which they take into consideration the non-financial interest of third parties in their investment. This goes expressly against the legal obligations of trustees and other fiduciaries.

At a third level, the disclosure obligation will extend to all those companies in which the institutions invest, thus spreading its influence, creating more red tape and spawning new interest groups throughout the economy.

At a fourth, deeper level, the new rules have significant practical implications for all businesses. The intent is not only to oblige institutions to describe their attitudes, but also to determine those attitudes and to direct their behaviour.

As summarised in Insert 1 and Insert 2, the amendments were seen by their proponents as a means of exerting leverage on business operations, through the allocation of capital, to advance the agendas of labour, environmental, social and ethical pressure groups. The amendment was also supported by a number of "progressive" businesses including Westpac (the largest provider of ethical funds in Australia) and BP Australia (the leading proponent of corporate engagement) which see commercial advantage in the regulation of their competitors and other investors.

Insert 1: "Funds for Workers" by Paddy Manning It was just a couple of lines among hundreds of pages in the Financial Services Reform (FSR) Bill that passed the Senate in August 2001. A small amendment designed to promote ethical investment, based on a similar law introduced a year earlier in the UK, and pushed by an unusual coalition of green NGOs and trade unions on the one hand, and some more "progressive" companies like BP Australia and Westpac on the other. After lobbying led by Michael Kerr of the Australian Conservation Foundation and the Ethical Investment Association, Democrats Senator Andrew Murray and Greens Senator Bob Brown were both ready to move and support an amendment that all super funds and fund managers disclose: "the extent to which, if at all, ethical, social or environmental considerations are taken into account during the selection, retention and realisation of investments". Proponents stressed this was not a requirement for fund managers to take new things into account, or change their investment practices at all. It was just a new reporting requirement. But the motivation was clear to all sides: the new reporting would lift awareness of ethical investment, and funds' reluctance to publicly disclose that ethical concerns were "not considered at all" would prod them into greater consideration of the triple bottom line. Once financial institutions start taking more account of the triple bottom line, the thinking went, so must the companies that depend on the financial markets for capital. It was not an amendment welcomed by the Government, but nor was it strenuously opposed. By comparison the FSR Bill was a big deal. Since being first recommended five years ago as part of the Wallis Financial System inquiry, the Bill had caused the Government a degree of political pain. In particular the Bill's proposals for an integrated licensing system for investment advice-giving had struck trenchant resistance. New training, disclosure and remuneration rules had put financial planners -- part of the sensitive small business constituency still smarting over the GST -- offside. At the time the office of then Minister for Financial Services Joe Hockey, indicated tacitly the Government would not allow this drawn out financial services reform to fail on account of a relatively obscure ethical investment amendment. This acquiescence was tested somewhat at the last minute when, out of left field, Labor's Financial Services Spokesperson Senator Stephen Conroy moved his own crude two-word amendment to the Democrat's amendment: as a condition of crucial ALP support, "Labour standards" must be added to the list of things that would be reported upon. Being so explicit, it stuck out like a sore thumb from the woollier triple bottom line provisions. It is now law, and became effective (subject to a two year transition) on March 11th along with the rest of the FSR Act. As a result, suddenly, our banks, fund managers and super funds are put in the unlikely position of judging corporate Australia's labour standards. The irony is not lost on Conroy. Point out how this labour standards agenda must rankle with inherently conservative financial institutions and Conroy is blunt: "Great, isn't it?" Clearly when it came to drafting the FSR Regulations, Conroy's wording caused the Government some heartache. They are structured in such a way that "labour standards" will be reported separately from "ethical, social, or environmental considerations." Reading between the lines, the FSR Regulations say, "this is the Labor Party bit -- handle with care. The rest is safe, fluffy, triple bottom line stuff -- do what you like". From Ethical Investor Magazine,

Issue 11, May 2002

www.ethicalinvestor.com.au |

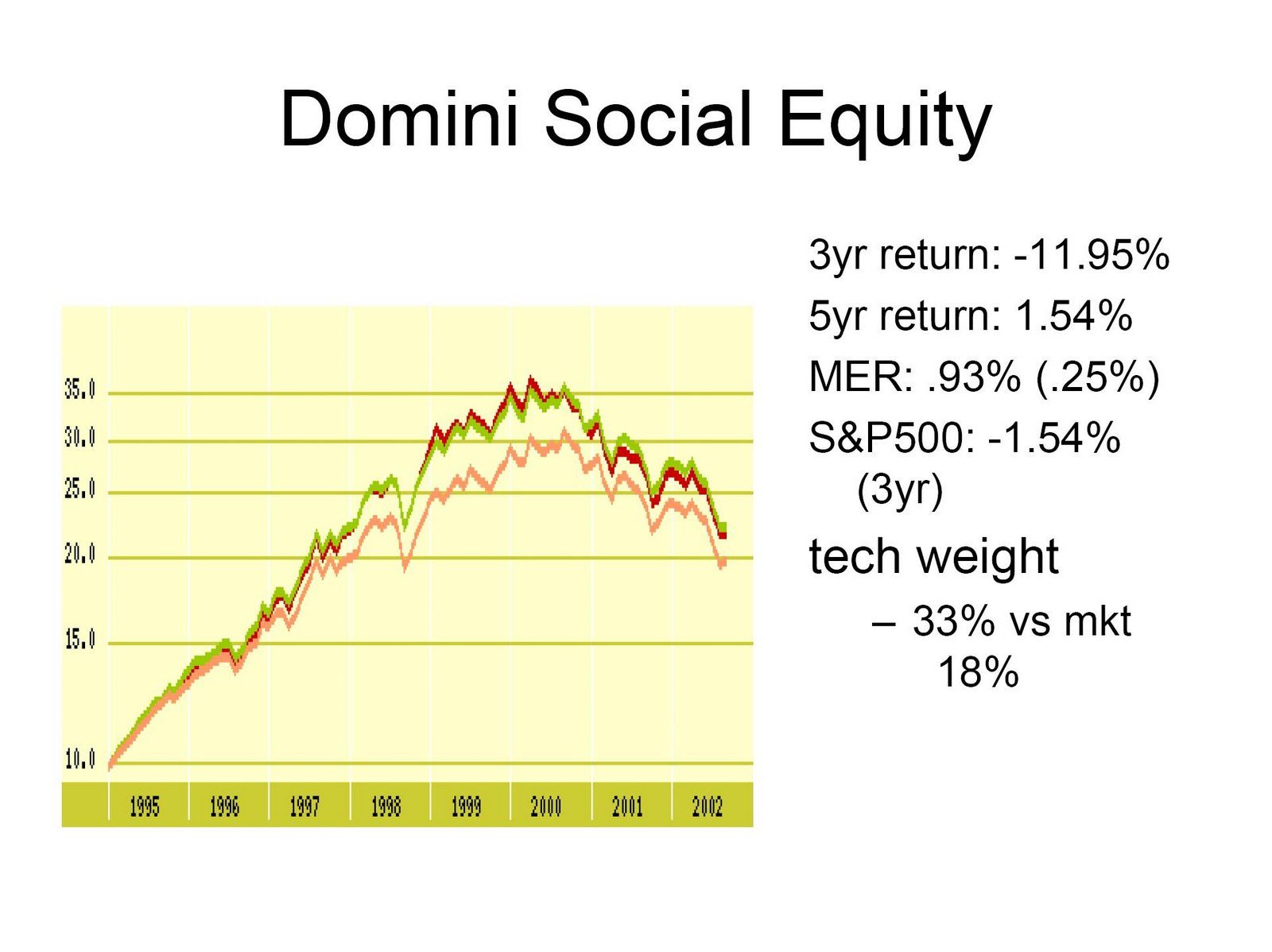

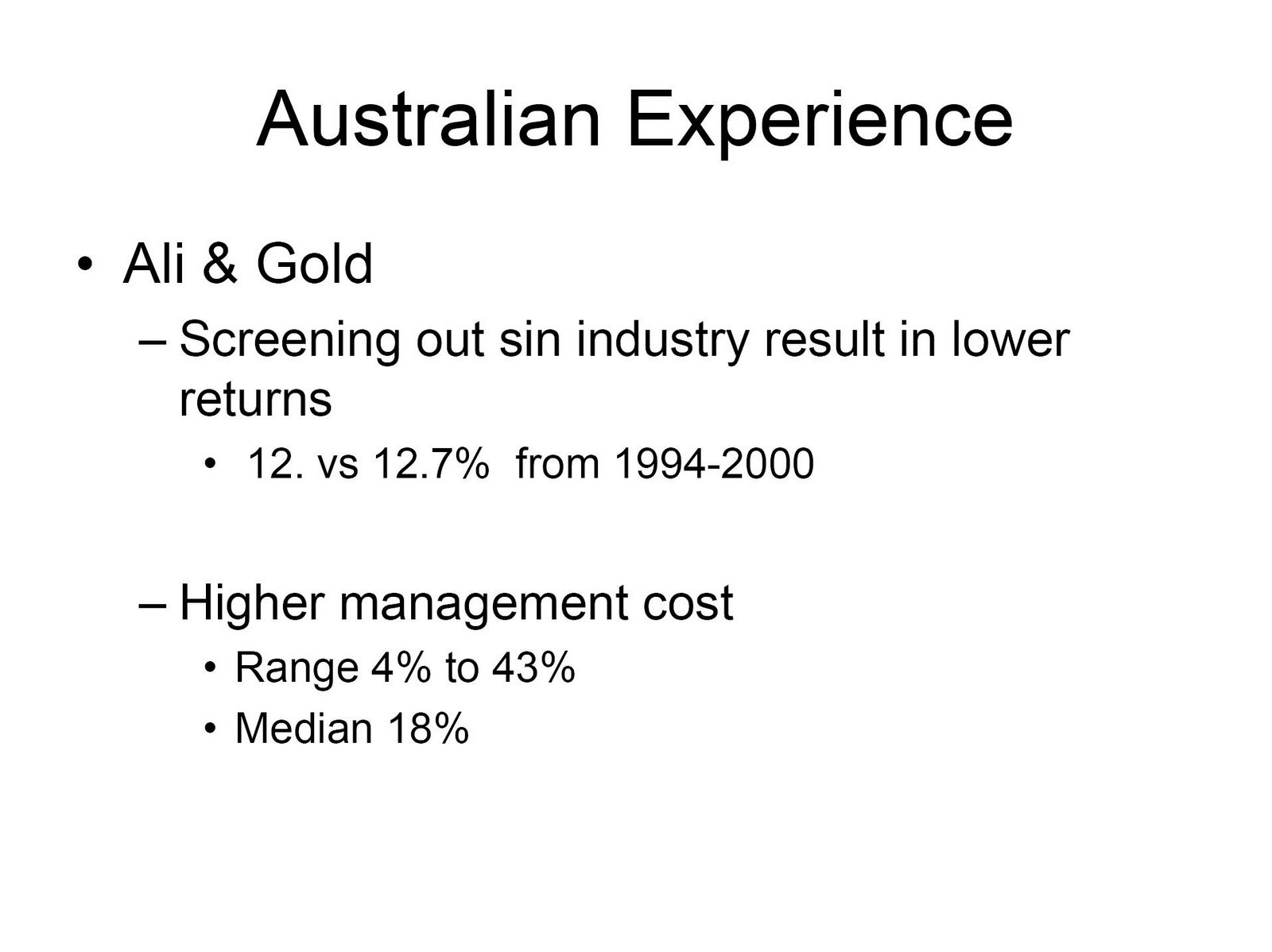

Insert 2: The High Cost of Ethical Funds While the promoters of Socially Responsible Investment (SRI) funds maintain that there is no trade-off between financial returns and the pursuit of social and other non-financial goals, their claims are based on outdated, overseas research and fail to consider the extra management and screening costs associated with SRI funds. US research does, on the whole, show that during the 1990s, (5) SRI funds were generally able to achieve gross returns on a par with the equity market as a whole. This is really not surprising, given the investment strategy employed. Most SRI Funds in the US have tended to invest in blue chip companies, in growing industries which, in the 1990s, tended to be socially "acceptable" industries, such as dotcoms, telcos, and services. In short, they have tended to invest in the leading firms in the fastest growing segments of the market. There are clear signs that this strategy is now failing and with it the relative returns earned by SRI Funds. Over the last few years, many of the firms in which the US SRI funds invested heavily, including Enron, WorldCom, Global Crossing and many dotcoms, have seen their share prices collapse, in part, ironically, because their managements behaved unethically. At the same time, the old, socially "incorrect" industries such as tobacco, mining, oil and gas are now the market leaders. While there is no detailed research which compares the relative performance of SRI funds during the last few years, there is some evidence that many SRI funds are haemorrhaging and leading the market in decline. (6) The US research also shows that the SRI Funds have high management costs. SRI funds will, of necessity, have higher costs. They not only need a team of financial analysts to pick the pool of stocks, but also a team of social engineers, ethicists, environmental scientists, and labour market analysts, to screen for good behaviour among the stock chosen by the financial people. Recent research in the US substantiates this. It found that SRI funds have expense ratios (management cost as share of funds invested) of between 1.5 and 2.5 per cent which compares very poorly with the average expense ratio of non-SRI Funds of about 1 per cent. (7) The high expense ratio means that in order for SRI funds to match non-SRI funds in terms of benefits to unit holders, they must achieve higher gross returns than non-SRI funds. And there is no evidence that they have been able to do so -- even during the dotcom bubble. It also means that the additional costs associated with SRI consume a sizeable proportion of unit holder earnings. Based on US research, the decision to invest in an SRI fund, as opposed to a non-SRI fund, will consume, on average, 14 per cent of expected lifetime earnings of a superannuation investment, which is an unacceptably high cost, particularly given the dubious benefits of the SRI process in the first place. (8) Given the fundamental differences in the composition and performance of US and Australian stock markets, great care should be taken when using US research to make decisions about SRI funds in Australia. In Australia, the old, socially incorrect industries such as uranium mining, gambling, electricity generation and, up until recently, tobacco production, make up a larger share of the Australian market than in the US. Ali and Gold (9) provide the first independent examination of the performance of SRI funds in Australia. They found that excluding "sinful" industries -- such as alcohol and gambling (which the majority of Australian SRI Funds do) -- between 1994 and 2001 would have resulted in a performance shortfall of 0.70 per cent per year, reducing the broad market return from 12.7 per cent to 12 per cent. They also found that "investors in Australian SRI Funds generally face additional fee imposts, compared with investors in mainstream Australian, managed investment schemes or superannuation funds. This is largely attributable to fund managers passing on to investors the development and marketing costs for SRI funds and the fees paid to external service providers (primarily, index vendors and SRI research providers)." (10) In summary, the available evidence indicates that SRI funds impose a significant cost on, and yield a lower net return to, investors than non-SRI funds. To the extent that the Act forces funds managers to undertake non-financial screening activities, then it will undermine the well-being of most Australians without adding much, if any, benefit. Of course, the high costs of SRI Funds are one of main benefits, from their perspective, of SRI promoters, as to them it means income. However, the livelihood of activists and promoters should have no bearing on the use of other people's funds. |

In practice, groups will undoubtedly exert pressure for highly detailed disclosure statements under each of the four headings and will seek to supervise the behaviour of the institutions concerned against these written statements. Draft "best practice" statements have already been drawn up, and a long line of consultants await the riches offered by the Act. ASIC will be pressured to produce compulsory guidelines which reflect the wishes of the groups. There will be a persistent pressure for all funds to become, in effect, ethical funds.

Funds and corporations will not be able to get away with the equivalent of vision or mission statements. There will be targets, monitoring, hectoring and punishment for perceived failure.

Nor will small business be immune from the effects of this provision. Such businesses have to raise capital through financial institutions and may then fall under the same strictures or find their funding restricted. Pubs, farms, and tobacco retailers are obvious candidates, but there are few limits once the moral censors are out.

In the end, this is an attempt, by indirect and stealthy means, to impose new and poorly defined community service obligations and prescribed behaviours on business generally. By means of legislation and mandatory guidelines, the corporate sector will be obliged to undertake actions (and report on them) that may adversely affect its profitability and that it would not necessarily undertake voluntarily.

If the community and governments wish companies to take on additional social responsibilities, then these ought to be funded through the public sector so that their costs are not concealed and so that their burden is equitably distributed.

THE ECONOMIC EFFECTS

In practical terms, the legislation opens a Pandora"s Box. It has far-reaching effects for that important group of financial institutions which control our savings, and for all the businesses in which they actually and potentially invest.

At 30 December 2001, $654 billion was held in what are described as Managed Funds (see Table 1). This effectively comprises the categories covered by the Act's disclosure provision. As can be seen, the bulk is held in life insurance and superannuation.

Table 1: Managed Funds -- Consolidated Assets

December Quarter 2001 ($billion)

| Life Insurance Offices | 176.6 |

| Superannuation Funds | 303.3 |

| Public Unit Trusts | 130.9 |

| Other | 43.6 |

| Total | 654.4 |

Source: ABS 5655.0, December Quarter 2001.

Managed Funds have grown very rapidly, almost doubling in nominal value in the last five years. (3)

The growth in Managed Funds is perhaps the major financial reflection of our national saving effort. It should be said that our national saving effort has been nothing short of dismal in the last decade. In particular, the government sector only ceased dissaving a few years ago and slipped back into it again in 2001-2002. The corporate sector saving effort has also been patchy. The result is that only the household sector has had a uniformly positive, though still weak, saving performance. At 2.5 per cent of GDP, household saving is nothing to celebrate.

Total national net saving in 2000-01 was estimated at $18.5 billion (4) and was almost all saving by households. The growth in Managed Funds was $40 billion, which would incorporate a substantial proportion of household saving and would be a significant support to total net capital formation of $37.7 billion.

National aggregate figures such as those quoted above are subject to qualification and are not fully comparable. What they do demonstrate, however, is the vital importance of the managed-funds sector to our domestic savings and investment effort. They also suggest that we should be extremely cautious in developing new policies for the sector -- in particular, policies which might impede the flow of the savings of individual households to their most fruitful and efficient use.

The disclosure provisions of the Act are intended to influence the allocation of those funds and thus have unmeasurable but potentially significant effects. Most markets in Australia are imperfect and the financial markets are no exception. Subject to normal prudential limits, however, there is a strong case for allowing institutions to allocate their investments according to commercial advantage. In this way, savings will be allocated to their most productive use. The extent to which other considerations are taken into account should be subsidiary to this. Investors who favour these considerations are already able to give expression to that preference by selecting ethical funds.

The Act will encourage significant distortion of investment decisions and place pressure on management to placate critical and hostile groups which have little financial stake in the institutions or businesses affected. There is no doubt that at the very least, the Government should have consulted the wishes of the millions of savers whose money they have put at risk.

The weakening of the link with shareholders has many implications, not only for the financial soundness of companies but also for the property rights of all shareholders. Insofar as the government confers rights on other "stakeholders" that affect the return to shareholders, it erodes the rights of those shareholders which they purchased in good faith. When the government does this, there is a clear justification for some form of compensation to shareholders. It is implications like these which would have been revealed if there had been proper consultation with those affected.

THE ACT IN ITS BROADER CONTEXT

The disclosure provisions of the Act were not drafted in a vacuum. In Australia and overseas, interest groups of many kinds have exerted public, financial and political pressure to modify corporate behaviour to suit their own specific agendas. Many corporations and international institutions have already made a significant response to these pressures.

The Act is another manifestation of this process, albeit with an important difference. It is based in law, rather than through public pressure.

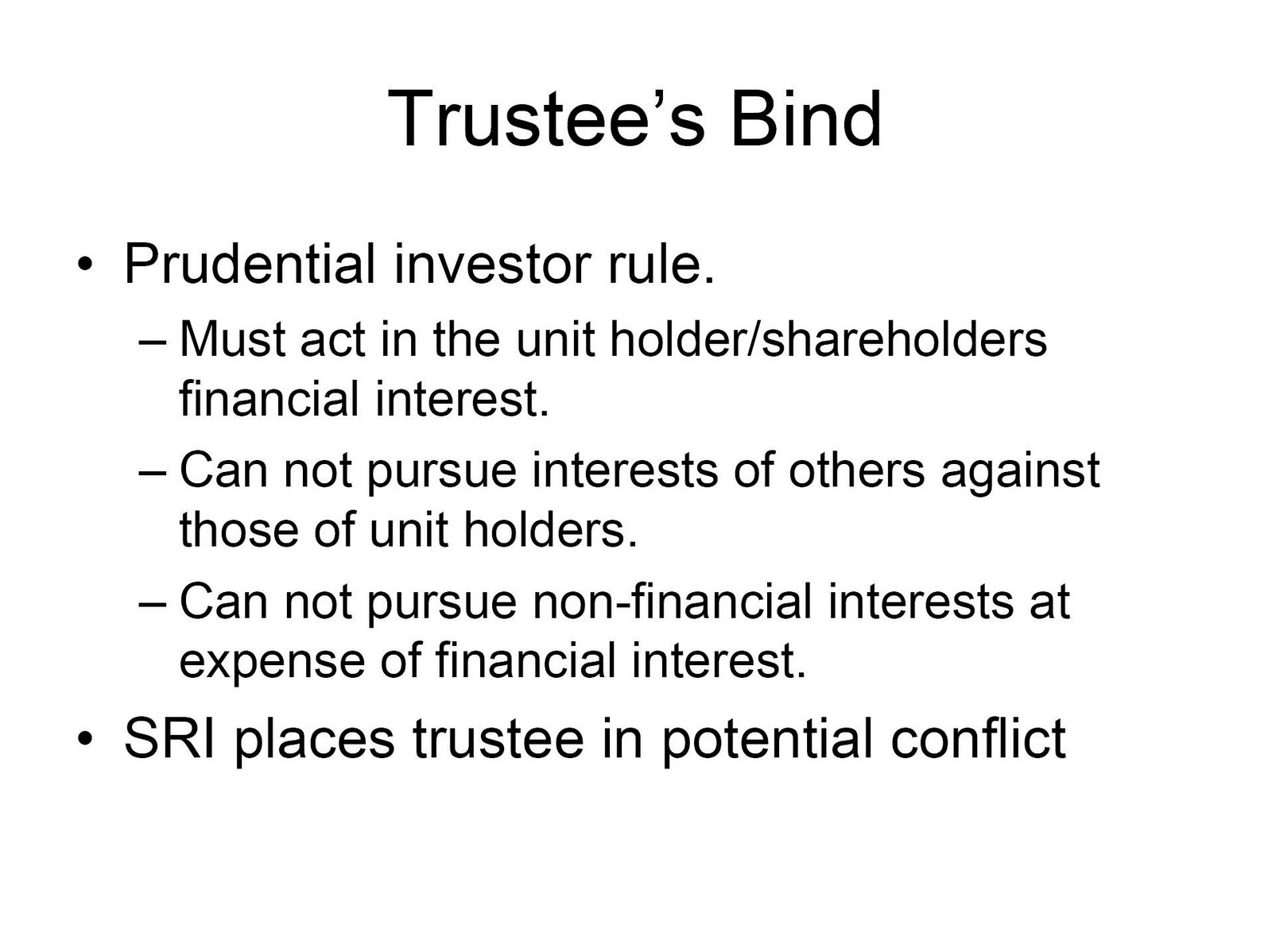

Insert 3: Threat to Trustees and Other Fiduciaries SRI funds, and more generally the Act, impose significant risks on trustees and others who have a fiduciary responsibility to manage funds. Under the so-called "prudent investor rule", trustees and other fiduciaries have a responsibility to unit-holders to maximise the financial return on the funds invested. Under the rule, trustees cannot sacrifice gains to unit-holders for gains to others, nor can they give priority to non-financial objectives over the financial objective of optimising the return on the fund assets. What this means is that trustees of SRI funds are not allowed, by law, to sacrifice financial returns in the pursuit of social, environmental, ethical or labour standards. If they do, they expose themselves to the risk of legal action by unit-holders. The existence of the "prudent investor rule" no doubt helps explain the vigorous denial by advocates that the returns are lower and the costs higher for SRI funds. In a court of law, the views of advocates will, however, count for little, and both logic and the available evidence indicate that SRI funds do entail a financial cost to unit-holders and therefore pose a risk to the trustee. The Act, by encouraging wider adoption of SRI Funds, will increase the level and spread of these risks and place trustees in real dilemmas. |

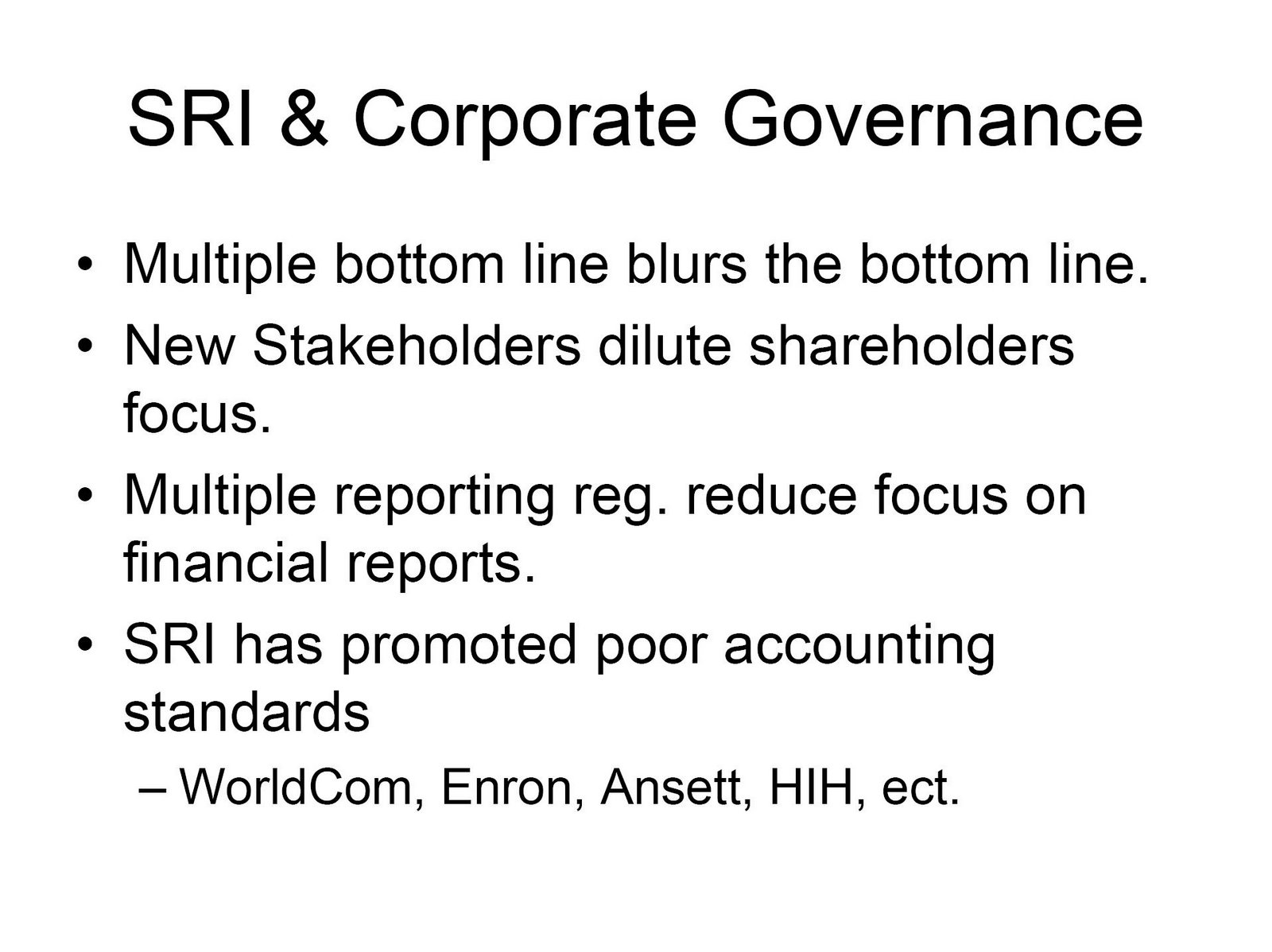

THE MULTIPLE BOTTOM LINE

One means by which the various social interest groups have tried to exert pressure on companies is through adoption of the "triple bottom line", where the financial reports and goals are put on a par with reports and goals on environmental and social outcomes.

It is in the nature of movements of this kind that, once the bandwagon gets moving, others will jump aboard. As well as requiring environmental and social reports, the trend is to take on other passengers, such as labour standards and ethics. As a result, the triple lines have evolved into the "multiple bottom lines", and again the Act reflects this.

THE EXPANDING STAKEHOLDER LIST

Business has long recognised the need to take into consideration the concerns and interest of "stakeholders". It is obvious that people and groups, such as lenders, employees, customers and suppliers, are to a degree integral to the success of a business and often invest or put at risk things of value to advance the business. Lenders put their money at risk. Suppliers often provide goods on short-term credit. Employees invest in firm-specific skills. The local community often shares the air, land and water with the business. To a degree, it is only reasonable for business to take into consideration the interest of these stakeholders and doing so is not necessarily incompatible with the primacy of shareholders. Indeed, traditional stakeholder theory argues that systematic consideration of stakeholders' interests enhances the firm's viability and therefore adds to shareholder value. Traditional stakeholder theory also makes no extra demands about business ethics or corporate social responsibility.

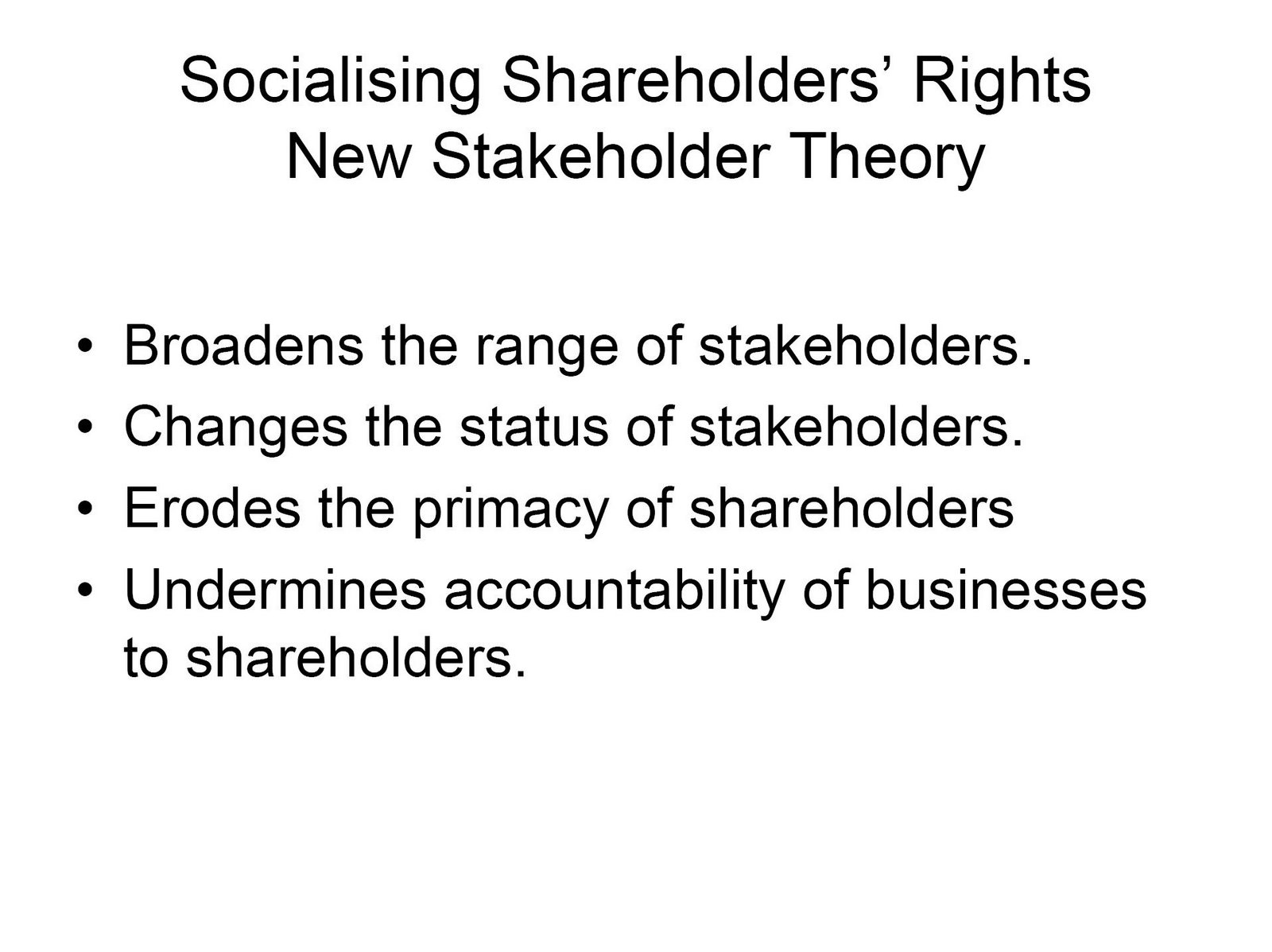

The multiple bottom line process is based on an entirely different stakeholder theory -- one which is explicitly antithetical to maximising shareholder value.

First, the new stakeholder theory greatly broadens the range of permissible stakeholders, to include "any group or person who can affect or be affected by the achievement of the organisation's objectives". (11) In practice, this translates into anyone who voices an opinion about the business and can attract the attention of the media, regulators or politicians.

Second, the new theory changes the status of stakeholders. Under the traditional theory, stakeholder interests are taken into consideration by management. Under the new theory, stakeholders are entitled by virtue of their self-proclaimed stakeholder status to directly influence the operation of the business.

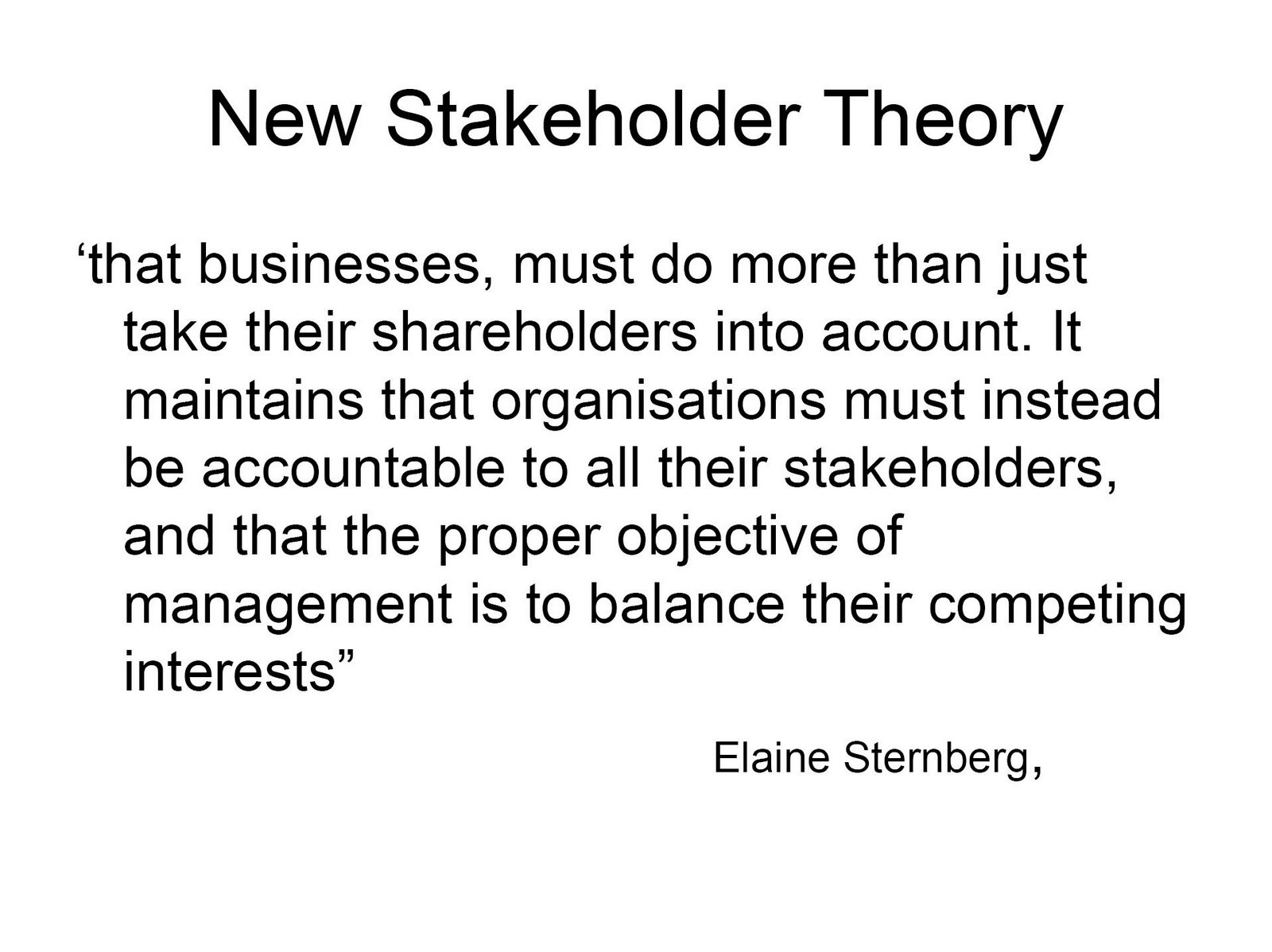

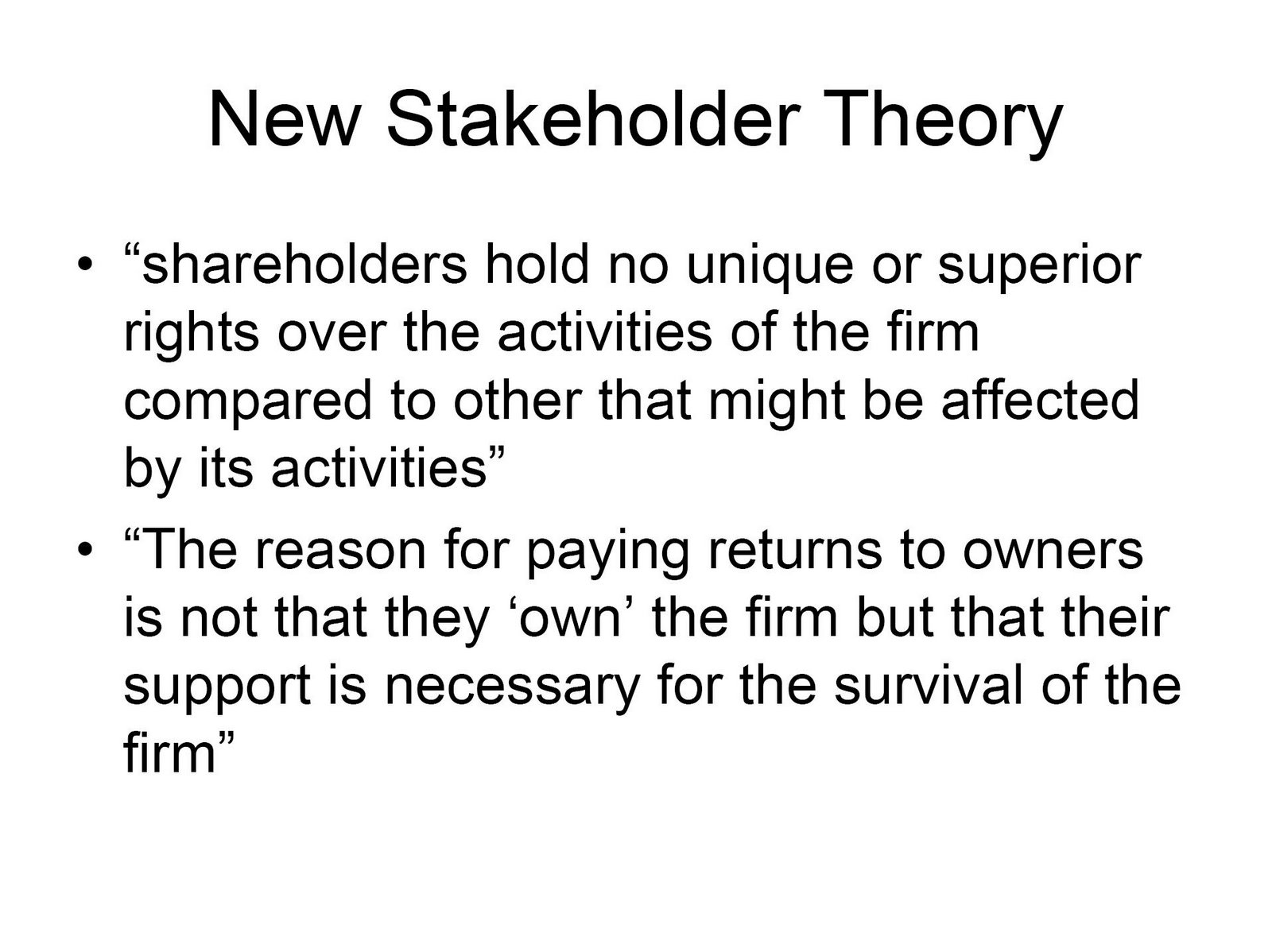

Third, the new stakeholder theory erodes the primacy of shareholders and the accountability of business to shareholders. Traditionally, stakeholder interests are considered because, in the end, doing so will advance the interests of shareholders. Traditionally, management accountability is not to stakeholders but to shareholders. The new stakeholder theory explicitly repudiates this type of accountability; indeed doing so is one of the defining features of the new stakeholder doctrine. (12) As described by Elaine Sternberg, the central tenet of the new stakeholder theory (which she defines as stakeholder entitlement) is: "that organisations, and particularly businesses, must do more than just take their shareholders into account. It maintains that organisations must instead be accountable to all their stakeholders, and that the proper objective of management is to balance their competing interests".

The stakeholder entitlements approach has a number of direct and serious practical implications for investors and business.

First, it will cost shareholders and traditional stakeholders. Of necessity, there will eventually be trade-offs between the extra-legal social, ethical, environmental and labour goals sought by the new stakeholders on the one hand and returns to shareholders and traditional stakeholders on the other. Additional performance targets don't come free, but since only the traditional stakeholders have something at risk, they will in the end bear the costs. And, as discussed in Insert 2, this is what the research shows.

Second, scarce managerial resources will be consumed in the compilation of multiple reports and pandering to the new army of non-riskbearing stakeholders. This again will be at the cost of shareholders and traditional stakeholders (see Insert 2).

Third, it will accentuate the agent-principal problem and thereby undermine accountability of the corporations and confidence in the market. One of the greatest challenges to business is to ensure that management (the agent) acts in the interest of shareholders (the principal) rather than in their own interest or some other party. Overcoming the agent-principal problem has been the focus of recent corporate and accounting reforms and ostensibly even of the Act. While some gains have been made, particularly in countries such as Australia, the recent demise of OneTel, HIH, Enron and WorldCom, indicates that the problem remains. Indeed, these recent corporate collapses and scandals show that accountability of management to traditional shareholders remains one of the significant issues facing corporate Australia and the community at large. By introducing diverse new demands, which dilute the rights of shareholders, the triple bottom line will actually weaken the accountability chain and hence the ethical response and social contribution of corporations to the owners, to real stakeholders and ultimately to the community at large. The new stakeholder capitalism will consume scarce management time and resources and will provide succour and comfort for management to pursue non-shareholder goals. It will provide multiple excuses for poor or even fraudulent management practices. It will also offer the thinning ranks of corporate headquarters' staff a new and expanding, but counterproductive, career path.

Fourth, the multiple bottom line processes promote destructive rent-seeking behaviour. Since the new stakeholders put nothing at risk except maybe the resources they expended in lobbying (which in turn are mainly paid for by someone else), they will push their goals beyond a level that is beneficial to shareholders, traditional stakeholders and the economy as a whole.

Fifth, the process promotes false prophets and destructive tactics. Most of the new stakeholders, in the final analysis, obtain their status, not by reference to their expertise, representative or ethical status, but rather by their ability to be heard in the media and to threaten the reputations of corporations and individuals. Greenpeace, for example, has no scientific expertise, is a tightly controlled multinational club run from Europe with next to no Australian input, and has a long history of stretching the truth and abusing people's rights. Yet it is regularly accorded stakeholder status by corporations and governments. Indeed, it is currently campaigning to become a stakeholder to investment managers under multiple bottom line provisions of the Act, and recently published a guide to socially responsible behaviour for businesses. (13) A quick perusal shows that this new stakeholder plans to act against the interest of Australia investors.

The Good Reputation Index of the Fairfax Press provides ominous indications of things to come under the Act.

The Good Reputation Index published in The Sydney Morning Herald and The Age attempts to measure the social, environmental, labour, and ethical as well as the financial and public relations reputations of the 100 largest companies operating in Australia and New Zealand. It is designed as a tool for the corporate social responsibility industry and as a guide to firms in their deliberations about corporate social responsibility, and is being used as such.

In constructing the index, the Fairfax Press adopted what is now the standard methodology in the corporate social responsibility industry -- that is, basing the index on the views of high-profile pressure groups. And it included the views of most of the leading lights of the corporate social responsibility industry.

As such, the Good Reputation Index provides a good indication of how corporate Australia will be rated by multiple bottom line provisions of the Act.

Table 2 lists the top ten firms ranked according to the overall or multiple bottom line reputation as well as their ranking (out of 100) on financial performance. Table 3 lists the top ten firms ranked according to financial performance and contrasts this with their multiple bottom line ranking.

Table 2: Top Ten Companies -- Multiple Bottom Line

| Multiple Bottom Line | Financial Bottom Line |

| Australia Post | 1 | 24 |

| Westpac | 2 | 21 |

| Foster's Corp | 3 | 19 |

| Holden | 4 | 32 |

| Queensland Rail | 5 | 46 |

| Alcoa | 6 | 28 |

| IBM | 7 | 54 |

| Ford | 8 | 54 |

| Telstra | 9 | 39 |

| ING | 10 | 31 |

| Average | | 35 |

Source: Good Reputation Index 2001, Sydney Morning Herald, October 22, 2001.

Table 3: Top Ten Companies -- Financial Bottom Line

| Financial Bottom Line | Multiple Bottom Line |

| Flight Centre | 1 | 66 |

| Westfield | 2 | 71 |

| Woolworths | 3 | 15 |

| NAB | 4 | 12 |

| Leighton | 5 | 11 |

| Telecom NZ | 6 | 52 |

| Suncorp-Metway | 7 | 37 |

| RioTinto | 8 | 28 |

| Qantas | 9 | 49 |

| Wesfarmers | 10 | 20 |

| Average | | 36 |

Source: Good Reputation Index 2001, Sydney Morning Herald, October 22, 2001.

These tables show that, according to the Index and therefore the social responsibility industry:

- Financial performance and social responsibility do not go together. Only one of the top ten most socially responsible firms is ranked among the top 20 firms in terms of financial performance. Moreover, all of the most socially responsible firms performed worst on their financial bottom line. Conversely, just three of the top ten financial performers were ranked in the top 20 in terms of social responsibility and, on average; they ranked a lowly 36 on so-called social responsibility grounds.

- Government protection and direction is good and market competition is bad. Five of the top 10 most socially responsible firms are government-controlled. Two, Australia Post (ranked 1st) and Queensland Rail (ranked 5th), are government-owned monopolies. Telstra is partially government-owned and heavily regulated. Holden and Ford are sustained only by the huge subsidies flowing to them from the taxpayer via Canberra. None of the top ten financial firms are government-owned or subsidised and all face vigorously competitive markets.

- Funding social activists is a key to social responsibility. All the highly ranked socially responsible firms donate heavily to corporate social responsibility groups (including many of the organisations who acted as judges for the Index). Westpac (ranked 2nd), Alcoa (ranked 6th) and ING (ranked 10th) are not simply generous financial contributors, but are also strong promoters of the triple bottom line. Westpac has taken the lead in promoting ethical investment in Australia and helped push the corporate social responsibility amendments to the Act. ING has taken a similar approach around the world. Their high ranking is a reward for their contribution to the cause.

WHY IS THE ACT NEEDED IN AUSTRALIA?

There would be some point in all this activity if there were evidence that Australian business is particularly unethical, either absolutely or relatively. There is no such evidence.

In many developing countries, corruption is routine and permeates all levels of society, including the government. This is not the case in Australia. Although no fair comparison can be made with this category, most major Western corporations do operate in such countries. They daily face the moral dilemmas posed by doing business with actively corrupt officials, suppliers, labour organisations and non government organisations.

It is simple from the comfort of Australia, where the rule of law is the norm, to condemn companies which deal with oppressive and corrupt regimes that are the norm in many other parts of the world. For businesses, there is a conflict between the incentive to invest and the need to act legally. This is shadowed at the national level by the tension between economic development and state control. Sometimes there is little alternative other than to refuse to invest, and in some cases this is what Australian firms have done.

A parallel difficulty for firms is encountered where, in the rush for development, the laws of the developing country actually permit practices that Australian society has now abandoned. In these cases, the anti-globalisers seek to impose current Western standards on developing countries, denying them the stage of development from which the West has benefited in the industrialised world. A recent example is BHP's withdrawal from the Ok Tedi mine, where an Australian court and Australian activists prevented arrangements agreed to by the government of PNG and BHP/OTML. PNG law provided the wherewithal to develop the region and provide compensation to landholders adversely affected by the mine. BHP has now disposed of its holding in the venture (14) despite the plea of the PNG government and most locals to remain. There are, no doubt, complex issues of right and wrong here, but ethical imperatives differ across countries and may be shaped by their most pressing priorities.

According to Transparency International (see Table 4 below), an anti-corruption organisation, Australian companies were the least likely to pay bribes in major exporting countries, ahead of Switzerland, Sweden, Austria and Canada. Moreover, our companies' performance had improved absolutely and relatively in the last three years between surveys. This contrasts with British, American, Japanese and French companies, which were significantly more likely to pay bribes. Non-Australian companies in countries such as Russia, China, South Korea and Italy were more than twice as likely to bribe as Australian companies.

Table 4: Transparency International Bribe Payers Index 2002

In the business sectors with which you are most familiar, please indicate how likely

companies from the following countries are to pay or offer bribes to win or retain

business in this country [respondent's country of residence]? (15)

(A score of 10 represents a perfect score.)

| Rank | Country | 2002 | 1999 |

| 1 | Australia | 8.5 | 8.1 |

| 2 | Sweden

Switzerland | 8.4

8.4 | 8.3

7.7 |

| 4 | Austria | 8.2 | 7.8 |

| 5 | Canada | 8.1 | 8.1 |

| 6 | Netherlands

Belgium | 7.8

7.8 | 7.4

6.8 |

| 8 | United Kingdom | 6.9 | 7.2 |

| 9 | Singapore

Germany | 6.3

6.3 | 5.7

6.2 |

| 11 | Spain | 5.8 | 5.3 |

| 12 | France | 5.5 | 5.2 |

| 13 | USA

Japan | 5.3

5.3 | 6.2

5.1 |

| 15 | Malaysia

Hong Kong | 4.3

4.3 | 3.9

n.a. |

| 17 | Italy | 4.1 | 3.7 |

| 18 | South Korea | 3.9 | 3.4 |

| 19 | Taiwan | 3.8 | 3.5 |

| 20 | China (People's Rep.) | 3.5 | 3.1 |

| 21 | Russia | 3.2 | n.a. |

THE INTERNATIONAL DIMENSION

Not unexpectedly, international institutions have enthusiastically taken up the opportunity to involve themselves in the reshaping of capitalism through imposing new obligations on business.

At the instigation of the Secretary-General of the UN, a "Global Compact" has come into being which contains a set of principles to be observed by businesses which cover human rights, labour standards and environmental protection. A Global Compact Office has been set up.

The European Commission has drafted a "Framework for Corporate Responsibility" which incorporates codes of conduct, stakeholder monitoring and community advisory committees.

The International Standards Organisation, which has done much good work on technical standards, has moved into management standards with ISO 14000 -- environmental management.

Pressure has also been exerted by other public and private entities, such as the Ford Foundation, The Prince of Wales Business Leaders Forum and a host of universities, who base part of their raison d'être on advising or hectoring the business sector on how it should conduct its affairs.

A common thread is what has been termed the "new tripartism" -- the involvement of government, the community and business in managing the world economy. What it actually means is the acceptance by business of intervention by government (including international agencies such as the UN and EU) and non-government organisations (NGOs) in their operations, but with no reciprocal obligation.

The intention, and no doubt the result, will be to place greater burdens of consultation on business and further social obligations.

THE DIFFICULTY OF SUPERVISING MORALS

As an attempt to raise the standards of corporate behaviour, the disclosure requirement in the Financial Services Reform Act must be measured against a clear definition and interpretation of the words employed.

LABOUR STANDARDS

Although the criterion has been inserted at the behest of the labour movement, there is considerable disagreement over the best way to improve labour standards. Labour standards are not simply those prescribed in the various manifestoes issued by the ACTU. For example, the ACTU has tended to support a relatively interventionist labour market policy, particularly as wage rates and Australian labour markets are relatively heavily supervised.

It is likely that all Australian businesses would answer affirmatively that they took into account all labour standards prescribed by the domestically applied law to the extent of that prescription. This would not mean the application of uniform standards across Australia because standards do differ from State to State, from region to region and from industry to industry.

It will be very difficult for financial institutions to affirm that they were able to take into account the standards applied in those companies or projects in which they invested. Not only would it be difficult to assess the degree to which those companies or projects observed the law of the countries in which they operated, but it would be even more problematical to assess the degree to which the behaviour conformed to the equivalent Australian standards. More importantly, it would be impossible to judge whether the application of Australian standards overseas would be to the ultimate benefit of the workers of the countries concerned.

There is a further degree of difficulty in defining those labour standards which go beyond the black letter law. Is it simply more of the same? Does it include the work ethic?

The inclusion of this criterion is all the more curious when we recall that, just last year, Parliament, including the Senate, threw out the Democrat-inspired Corporate Code of Conduct Bill 2001 (which included labour standards), on the grounds of its impracticability. It shows the way in which unsound ideas, persistently held, can prevail unless the Government exerts the utmost vigilance.

The inclusion of labour standards in the Act has particularly serious implications for the millions of people who plan to live off their superannuation in retirement.

The union movement has long threatened to use its leverage over the superannuation industry for industrial purposes. Indeed, it is ACTU policy to do so. However, its efforts to date have been greatly restricted by the requirements, under the law, for trade union trustees to industrial super funds to act in the long-term financial interest of superannuants. The requirement that such funds now report on an undefined set of labour standards not only provides union activists with a new campiagning tool, but gives them the legal justification to pursue their industrial goals at the expense of returns to superannuants. Given that members of industrial funds have no choice and little influence over their participation in such funds, this constitutes a significant threat to the rights and futures of millions of Australians.

ENVIRONMENTAL CONSIDERATIONS

The main challenges an institution will face in reporting environmental considerations will be those of nature and degree. Although there are differences between commentators as to what constitutes an environmental consideration, the debates of recent years have given a very wide definition.

For example, the Australian Bureau of Statistics presented the environment as: "... the standard compartments the average person usually identifies when thinking about the environment -- air, water, land and living things." (16) This suggests that environmental considerations would have a fairly comprehensive application to most business activities.

Bjørn Lomborg, the sceptical environmentalist, canvasses human welfare, resource use, pollution, biodiversity, global warming and many other areas in his recent book, (17) suggesting an equally wide definition of the environment

Areas of doubt will arise generally about what matters to include and in what detail an institution ought to disclose environmental considerations. Every investment will have some environmental impact, however small. Some will be more obvious than others.

One approach available to institutions is for their disclosure document to embody a general policy statement on their environment policy and a list of activities in which it will not directly invest. This would imply that it might invest in any activity not listed. The disadvantage is that there would certainly be pressure to enlarge the list and to include indirect investments through banks etc.

The institution may begin by offering a fairly general definition of what they judge to be environmental considerations. But in reporting the extent of their "taking into account", they will be expected to describe what activities they judge to be beyond the pale.

Rather like the other three criteria, the test may turn out to be largely a negative one. While institutions may state that they are satisfied with the environmental performance of their investments, some investors will want to know whether the institution invested in, say, uranium, mining, forestry or some other sensitive industry.

At what level of detail do the explanations stop? Environmental concerns are notoriously diverse. They range from very general matters such as greenhouse gases and salinity, through industry-specific matters such as nuclear energy and logging, down to local issues such as development planning and effluent discharge.

Individuals may be far more passionate about local than global impacts ("think globally, act locally"). At any level from international to local they may require a great deal of detail to feel satisfied they have, in the words of the Act, "such ... information as a person would reasonably require for the purpose of making a decision, as a retail client, whether to acquire a financial product".

What a person would "reasonably" require is not entirely up to the individual in each case. There must be a general test of reasonableness. But, with the environment, governments have conceded so much ground to interest groups, large and small, that, in effect, what is reasonable can now be determined by a very large number of entities -- official planning and environmental agencies, NGOs, local action groups and individuals.

What this means for the disclosure obligation is either a very long statement, or the risk of exposure to penalties or litigation for failure to be candid on matters that one group or another judges to be reasonably required. In any case, the degree of uncertainty and risk in conducting business is enlarged.

Insert 4: "Workers will use super muscle for green ends" by Paul Robinson The ACTU has warned business that unions would use their clout to force superannuation funds to invest workers' money in more environmentally friendly and socially responsible industries. ACTU president Sharan Burrow told the Sydney Institute last night that employee members sat on half the boards of funds that controlled almost 50 per cent of total superannuation assets -- about $200 billion. Ms Burrow said board members would face increasing pressure to invest in line with the interests and values of fund members as well as providing sound returns. "What all this adds up to is that unions, along with everyone else involved in the superannuation industry, have a responsibility toward ensuring that workers' retirement savings are managed in their long-term economic and social interests," she said. Ms Burrow said business was keenly aware that institutional investors, such as big superannuation funds, controlled most public company share registers. Funds were predicted to make up more than 30 per cent of the capitalisation of the Australian sharemarket within two years. Ms Burrow told the institute that unions were concerned about the independence of boards, transparency of decision making and executive remuneration. Unions were also keenly interested in how companies treated their customers, suppliers, employees and the community. "Are they good corporate citizens?" she asked. Quoting a study by accountants KPMG, Ms Burrow said 80 per cent of working people aged between 25 and 39 wanted to invest their superannuation in socially responsible ways. "There is growing evidence to show that socially responsible investments, such as those based on the Dow Jones Sustainability Index, do not sacrifice good returns," she said. The warning to business follows a powerful message delivered to unionists at the ACTU's June Biennial Congress in Wollongong by Richard Trumka, secretary of the leading United States labour council, the AFL-CIO. Mr Trumka stressed the financial power of workers and said US investment in socially responsible funds exceeded $US2 trillion. Ms Burrow said profits were essential to business, but excessive profits "at the expense of community services and dignified salaries and conditions for staff must be judged through the lens of a fair share for all involved -- employees, communities and shareholders". She said the ACTU had begun its corporate campaign earlier this year against Rio Tinto at the company's annual meetings in Brisbane and London. Unions sought resolutions to obtain a majority of independent directors on Rio Tinto's board and company commitments to abide by international labor standards. While Rio Tinto opposed the moves, more than one in five shares were voted in favor of better corporate governance and 17 per cent of shares urged the company to abide by ILO core labor standards. "Support for greater shareholder activism cannot be dismissed as a radical frolic," Ms Burrow said. "The ACTU unashamedly stands for democratic practices and transparency in our political system, in our workplaces, in communities -- and in the boardroom. "We believe that the workers who are the beneficial owners of billions of dollars worth of shares should have those shares voted in ways which will maximise their long-term earning potential and their broader interests as members of the community The Age, 30 August 2000 |

SOCIAL CONSIDERATIONS

It is likely that the word "social" is meant to connote considerations relating to voluntary, non-profit promotion of social betterment through charitable donations, sponsorship of local community organisations, support for staff community work and similar activities.

Some institutions -- indeed any reasonable individual -- might regard it as a sufficient social contribution to observe all the laws and regulations imposed on them by society and payment of all taxes and fees to support the public welfare bill ($80 billion at last count). It is likely, however, that a disclosure statement along these lines, although legally acceptable, is not what is intended by the drafters of the Act and would be regarded by them as inadequate.

Equally, the expression of some generalised statement of "social concern" on the part of the management and/or staff of companies attracting investment from the relevant institutions would be unlikely to be accepted as sufficiently taking into account social considerations.

So what is the point of including "social considerations"? It must remain something of a mystery until some "reasonable" persons define their social criteria, bearing in mind that reasonable people in our society have dramatically different opinions on how to improve society. Indeed, our political system is built on that disagreement. With better definition, we will have some concrete expression of the reporting task and the hurdle for those companies seeking to attract funds via the institutions concerned.

What would be retrograde would be pressure for institutions to conform to some state-sponsored social contract. Such an attempt to shackle the ever-diminishing, creative, freewheeling element of our society would not be to our social or economic betterment.

ETHICAL CONSIDERATIONS

Ethical matters, such as a CEO failing to report important details of the company's operations to the board, are well canvassed in current legislation. Ethical investment, on the other hand, is a misnomer. It most often refers to activities which some regard as immoral, but are often nevertheless legal.

An environmentalist might not think it unethical to put dangerous metal spikes in trees where a trade unionist would think it highly unethical (quite aside from its legal status). The same environmentalist might regard the felling of certain trees as unethical where a forester might see it as essential to the health of the forest (and legal).

Similarly, a social welfare organisation may regard the distribution of free syringes on the city streets as highly ethical (and legal), where the local community, on the basis of the predictable discarding of used needles in streets and children's play areas, might regard the practice as unethical and very dangerous.

Some practices of the Moslem community with regard to the treatment of women have been condemned by feminists as demeaning, discriminatory and, presumably, unethical. Amana Mutual Funds -- a leading Islamic ethical fund -- refuses to invest in banks and other companies that earn interest, while most other "ethical" funds are overweight in banks.

Arab leaders argue -- indeed they lobby investment funds -- strongly against investing in Israel, while many US foundations are overweight in Israeli stocks and investments.

There are many who might regard donations to a political party which favoured a strict refugee policy as unethical.

These are not extreme examples of inconsistency and they could be multiplied a thousandfold. They serve to illustrate that ethics, even in stable societies, are very selective, personalised and subject to change over time. But the clashes of ethical systems can be explosive. This is one reason why governments have tended to regard ethics as a private matter for which wide tolerance should be observed, and have restricted their supervision of society to a more limited body of laws which have some general assent and some chance of being enforced.

When we begin to think how to describe ethical considerations in the selection, retention or disposal of investments, the choice seems to be between meaningless generalised statements of goodwill towards all men or equally meaningless highly detailed listings of conduct or occupations judged to be unethical or ethical. Attempting on either basis to measure the degree to which the institution has taken those considerations into account verges on the impossible and/or the ludicrous.

It should be noted that virtually all economic and social activities would raise ethical questions for one group or another in our society. The essence of our society is tolerance for a diversity of behaviour, so long as it does not cause harm to others. It comprises that large segment of our national life and individual behaviour that is not supervised by government or any special interest group.

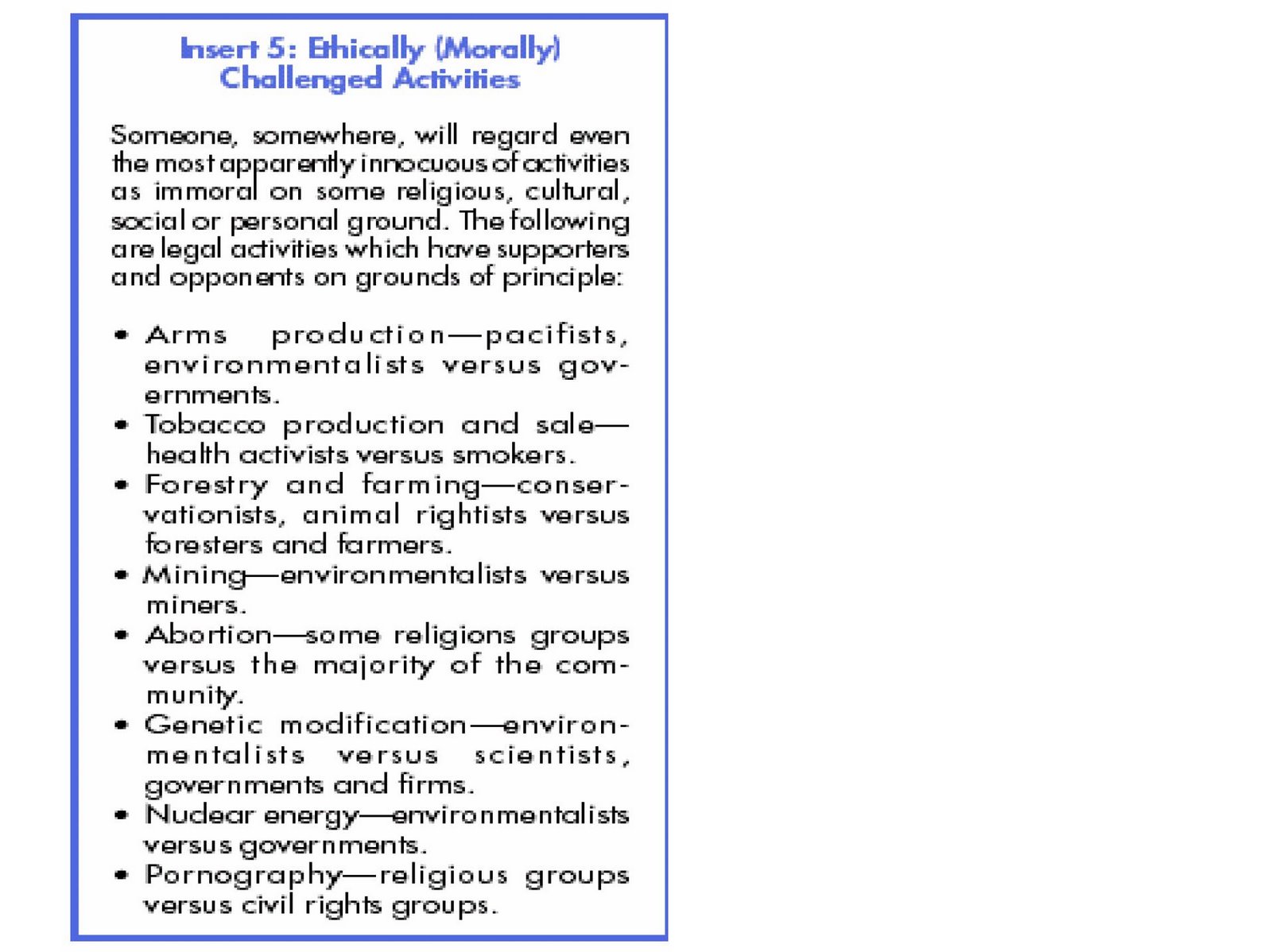

Consider the investments that might be regarded by individuals as raising ethical considerations. Insert 5 contains a list that reflects a variety of viewpoints. What we can see is that, although a case for each could be argued with passion and principle, there are very few which even 75 per cent of the population would support and, in many cases, less than 50 per cent would do so.

Is a firm which believes that one or more of these activities are not only legal but ethical, obliged to disclose that it invests in them -- in other words, is it obliged to question the ethics of an activity about which it has no doubts?

Or is it obliged to disclose that it invests in an activity that some (perhaps a minority) of the population thinks unethical and thus effectively be forced to accept others' ethical norms? If so, there will be no end to disclosure.

If a company consults its own conscience and believes that it conducts morally sound activities in an ethical manner, then it will have virtually nothing to disclose even if it invests in, say, arms production.

The practical difficulties for financial institutions are manifest.

What ethical considerations will be included? It is not feasible to include all possible considerations. The list would be never-ending. Prioritising cannot easily be done objectively. The task, if not impossible, exposes the institution to invidious choice and grievous moral hazard.

And who is to make the choice on what should be included? Is it the directors, the managers, the staff, the shareholders, an outside ethical committee or authority? Apart from the difficulty of making this choice, who is then to synthesise the views and who will have the final say?

The Act and regulations require the institution to report the extent to which the chosen ethical considerations are taken into account. It is open to an institution to state anything between "not very much" and "to a very great extent". Those tending towards the first formulation will suffer public obloquy and the latter will be asked for proof. In any case, the institution will be obliged to defend its disclosure through a description of the processes by which it will achieve the standard of performance which it has identified for the selection of ethics which it has also identified.

In the recent tradition of openness and respect for the numberless "stakeholders" who will want a seat at the table, the institutions will be under pressure to defend their disclosure report publicly and in detail. The "stakeholders" will demand not only to be informed in detail, but possibly to be participants in a more formal monitoring and auditing process with the right of producing their own reports. This opens up the institution to criticism of its definition of ethics, its ethical standards and its performance against those standards.

It all involves much more than a simple disclosure and it was always intended by its proponents that it should.

Insert 5: Ethically (Morally) Challenged Activities Someone, somewhere, will regard even the most apparently innocuous of activities as immoral on some religious, cultural, social or personal ground. The following are legal activities which have supporters and opponents on grounds of principle: - Arms production -- pacifists, environmentalists versus governments.

- Tobacco production and sale -- health activists versus smokers.

- Forestry and farming -- conservationists, animal rightists versus foresters and farmers.

- Mining -- environmentalists versus miners.

- Abortion -- some religions groups versus the majority of the community.

- Genetic modification -- environmentalists versus scientists, governments and firms.

- Nuclear energy -- environmentalists versus governments.

- Pornography -- religious groups versus civil rights groups.

|

ON THE WRONG TRACK

The broad intent of the four disclosure requirements is no doubt to encourage higher ethical and moral standards in the finance industry.

The theoretical and practical difficulties posed by the disclosure requirements have been outlined above. The requirements contrast with the rest of the Act and the generality of legislation. They force institutions to state their interpretation of social, ethical responsibility and rate their performance without giving them any standard of adequacy or any arbiter who can provide one. It is saying, "Prove you are a good citizen" without defining "good" or "citizen", or even what might constitute proof.

Definition, performance and reporting are all impossible tasks.

It also reverses the onus of proof, in that the institution is not assumed to be ethical unless it proves otherwise to the satisfaction of hostile parties. It has to demonstrate that it is ethical or it is assumed not to be.

The reasons why governments generally avoid involvement in general rules of behaviour is not just that they are impracticable in the ways described above. It is not even that the history of governments prescribing such rules has led to extremely oppressive social regimes and deadly enforcement. It is that the imposition of any particular system is itself an unethical act on the part of any government with a belief in individual freedom and human rights. It is a move away from the vital principle of Western societies' toleration of diverse views and diverse forms of living where these do not harm others.

The more intrusive and comprehensive the role of government, the less the freedom of the individual to follow his/her own chosen path.

CONCLUSIONS AND RECOMMENDATIONS

The principal conclusion from a close examination of the FSRA disclosure provisions is that it is ill conceived. More precisely:

- The provision is designed to facilitate detailed intervention in the operations of Australian companies through supervising the morality of their behaviour.

- It was implemented without proper consideration of its full implications.

- There is no role for government in supervising the morals of private individuals and entities beyond the point where a restricted category of activities is proscribed by law, because of harm to others.

- The Act is likely to impose large costs on millions of Australians for little or no gain and without their consent.

- The Act will expose trustees and other fiduciaries to the risk of acting against the financial interests of unit-holders and therefore breaking the prudent investor rule.

- There is no evidence that Australian companies have low ethical standards -- it is rather the reverse.

- It is invidious that the Government effectively delegates the roles of judge and jury in the process to "stakeholders" who frequently have no stake in the corporation and who are often hostile to it.

- The process involves potentially heavy costs to society through additional compliance and information costs, which are concealed from public view.

- It potentially imposes further costs through the effects on corporate operations and derogates the rights of millions of shareholders, superannuants and investors.

The main role for the corporate sector is to create the wealth which makes our society one of the richest and freest on the globe. The wealth-creation process is already heavily regulated, and for most businesses the conduct of operations is not value free. Individuals and branded ethical funds are free to invest using whatever criteria they wish.

It is always difficult for government to retreat from a piece of legislation which they have endorsed, albeit under pressure from their opponents. Furthermore, this tide of opinion has been subject to only a limited critique. There is, however, a strong case for repeal of this disclosure provision.

If the Government is powerless to repeal the provision, we would recommend a series of actions to redress its bias:

- Amend the Act so that the disclosure provisions are applied only to proclaimed ethical funds.

- Ensure that any regulation by Treasury or ASIC require funds to disclose the basis on which they screen or rate the various categories or companies.

- Oblige the professional screeners to do the same.

- Encourage greater transparency from the "stakeholders", particularly NGOs, in particular by the use of a Protocol. (18)

- Prescribe compliance with existing labour regulations as satisfying the labour standards criterion

In any case, the Government should:

- Stop funding the activists. Indeed, governments are one of the main funders of the SRI lobby both in form of grants to SRI promotional activities and grants to the many organisation which are dedicated to promoting it.

- Allow for full consultation with the business sector in changes to the law or subordinate legislation -- including compulsory guidelines.

- Compensate business for any additional costs arising from the Act and shareholders and investors for the loss of any property rights and returns.

- Consider requiring ethical fund managers to issue warnings to potential investors that the pursuit of ethical, social, environmental or labour objectives may lead to lower returns and higher costs.

ENDNOTES

1. These provisions include:

- A catch-all provision for regulations to require further detailed information in general or particular situations (Section1013 (4)(c));

- A provision for compulsory ASIC guidelines to reinforce clause 1013D(1)2, of which more below (Section1013DA); and

- A general obligation to disclose "any other information that might reasonably be expected to have a material influence on the decision of a reasonable person ... whether to acquire the product." (Section 1013E). There is an attempt (in Section1013F) to define what is reasonable, which does not, however, seem to reduce the subjectivity and openended nature of the general obligation.

2. "Socially Responsible Investment -- The Response of Investment Fund Managers", Deloitte and Touche, 2000; "Do UK Pension Funds Invest Responsibly?", David Coles and Duncan Green, Justpensions, July 2002.

3. ABS, Finance Australia, 5611.0, 2000-2001.

4. ABS, Australian Economic Indicators, 1350.0, December 2001.

5. For example, S. Hamilton, H. Jo and M. Statman, "Doing Well while Doing Good? The Investment Performance of Socially Responsible Mutual Funds", Financial Analysts Journal, November/December 1993; L. D'Antonio, T. Johnsen and R.B. Hutton, "Expanding Socially Screened Portfolios: An Attribution Analysis of Bond Performance", Journal of Investing, Winter 1997; M.G. Reyes and T. Grieb, "The External Performance of Socially-Responsible Mutual Funds", American Business Review, January 1998; L. Abramson and D. Chung, "Socially Responsible Investing: Viable for Value Investors", Journal of Investing, Fall 2000, cited in Paul Ali and Martin Gold , "An Appraisal of Socially Responsible Investments and the Implications for Trustees and Other Investment Fiduciaries", Centre for Corporate Law and Securities Regulations, The University of Melbourne, 2002.

6. Rob Wherry, "The Clean and the Greens", Forbes, 12 June 2000; "Sinners set to feel the heat", The Guardian, 28 May 2000; "Counting the cost of social responsibility" Mary O'Hara, The Guardian, 7 July 2002.

7. Rob Wherry, "The Clean and the Greens", Forbes, 12 June 2000.

8. The average long-term return of the stock market and therefore of the super funds is 7 per cent per annum. The expense ratio of SRI Funds in the US is, on average, about 1 per cent per annum higher than for non-SRI funds.

9. Paul Ali and Martin Gold, "An Appraisal of Socially Responsible Investments and the Implications for Trustees and Other Investment Fiduciaries", Centre for Corporate Law and Securities Regulations, The University of Melbourne, 2002.

10. Ibid., pages 30-31.

11. Freeman, R.E., Strategic management: A stakeholder approach, Boston: Putnam, 1984, page 46.

12. Sternberg, E., "The stakeholder concept: A mistaken concept", Foundation for Business Responsibility, Issues Paper No. 4 1999, page 21.

13. Greenpeace "Moving Forward: Benchmarking for Corporate Environmental Change" http://www.greenpeace.org.au/corporate/reports/Benchmarking_Report.pdf

14. Ok Tedi Mining, 2001 Annual Review, page 4.

15. The question related to the propensity of companies from leading exporting countries to pay bribes to senior public officials in the surveyed emerging market countries. A perfect score, indicating zero perceived propensity to pay bribes, is 10.0, and thus the ranking starts with companies from countries that are seen to have a low propensity for foreign bribe paying. In the 2002 survey, all the data indicated that domestically owned companies in the 15 countries surveyed have a very high propensity to pay bribes -- higher than that of foreign firms.

16. ABS, Australians and the Environment. 4601.0, 1996.

17. Bjørn Lomborg, The Skeptical Environmentalist -- Measuring the Real State of the World,. 2001.

18. This concept is discussed in Wood, R.J., "Protocols With NGOs: The Need To Know." Backgrounder, November 2001. Vol 13/1.