Address to National Summit on Power Generation,

Gold Coast, 25 February 1999

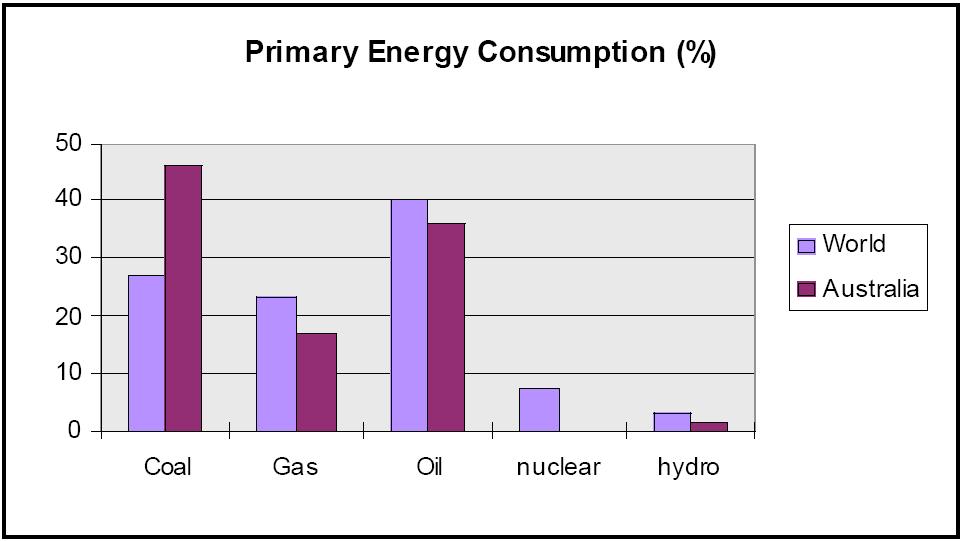

WORLD ENERGY CONSUMPTION

Coal supplies over one quarter of the world's primary energy, and over 46 per cent of that of Australia. Although oil is a more significant energy source worldwide, consumption of it and gas are less important to Australia.

The following chart sets out the details.

CHART 1

Source: BP

While hydro appears to be showing some growth worldwide, this is unlikely to persist. Lack of suitable sites is a major reason. Moreover, the forces which, rightly or wrongly, aborted the Franklin Dam have not lost sufficient clout in Australia to allow any real growth in hydro.

As for nuclear, over the past decade world output has grown 38 per cent and the fuel now accounts for 7 per cent of world energy consumption. It now dominates electricity supply in several European countries and is a fast growing source in several Asian countries.

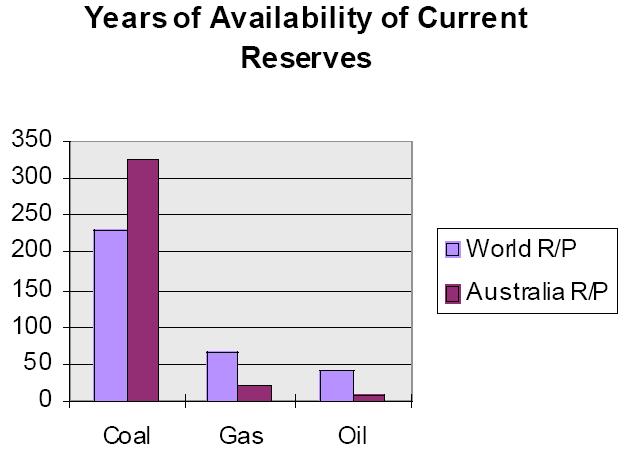

WORLD ENERGY AVAILABILITIES

In spite of most of us having been subjected to the Club of Rome nonsense forecasting an imminent run down in resources, the truth is that we face no shortages of the energy products on which we place greatest value. Even oil, the product with the most likely shelf date has shown a stubborn trend to maintenance of reserves. Oil and gas reserves at 41 and 64 years respectively are pretty much the same level as they were 20 years ago -- this is in spite of the fact that we have used up almost half the known oil reserves of 1977.

CHART 2

Source: BP

In fact the reserves listed are, in most cases, simply a stock of known resources which may be brought into production when commercial circumstances are right. This is amply demonstrated in the case of natural gas where Australia, according to the BP data, has only some 18 years supply. In point of fact there is known to be a great deal of gas off the west coast the owners of which have not yet seen a reason to proved it up.

In the case of coal, the world has 233 years of proved resources at present consumption levels. Australia is listed as having 327 years supply, but again that is a conservative number. For Victoria, proven and probable reserves of brown coal amount to over 1,000 years supply of a product with no known uses other than on-the-spot power generation.

AUSTRALIAN ENERGY TRENDS

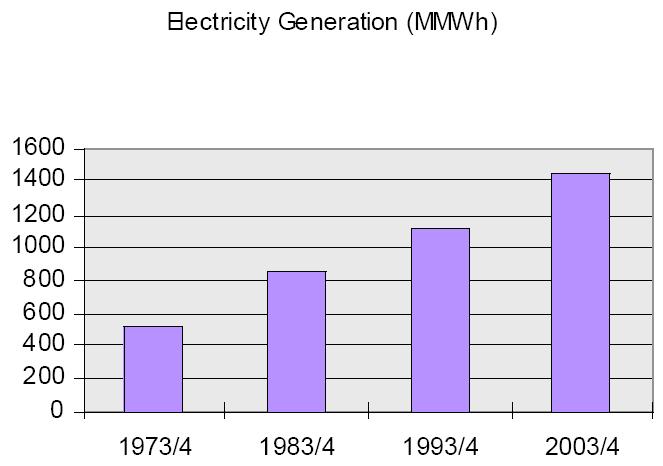

OVERALL TRENDS IN ELECTRICITY DEMAND AND SUPPLY

Australian electricity consumption has more than doubled over the past 20 years. Plant capacity is some 40,000 megawatts (dominated by large thermal units having a capacity between 275 and 500 MW) and output some 179 million gigawatt hours. Although energy demand is slowing, some 30% growth is expected over the next decade. Chart 3 indicates the trends in electricity generation.

Chart 3

Source: ABARE. 1 Pj =278 GWh

AUSTRALIAN PRICE TRENDS FOR GENERATED ELECTRICITY

A feature of the Australian market over recent years has been overcapacity. This has resulted both from over-ambitious plant development and improved plant efficiency, particularly in the light of corporatisation and privatisation in Victoria. In that State, the availability to run of the brown coal fired plants has been lifted from less than 70% to around 95%.

Systems in other States have also improved with the result that a reduced margin of reserve is now required. (The operationalisation of the link between Victoria and NSW and the proposed link between NSW and Queensland also reduces the required reserve plant margin.)

The increased efficiency and the effective increase in available capacity has been readily apparent since electricity has been sold within a market rather than its production administered by integrated State monopolies, a change gradually brought about since late 1994. Whereas the shadow prices of electricity in NSW and Victoria were formerly some $44.5 and $38 per MWh respectively, spot prices in both markets averaged $17 in the period from May 1997 to June 1998, rising to a heady $21 in the second half of the year. In the month of January prices in NSW and Victoria have averaged rather more than this.

Both South Australia and Queensland have seen higher prices than this, though the SA prices have only been made available since the NEM December commencement. Since the market opening, Queensland with its tight supply position has seen prices averaging around $35 while SA has seen average prices some $10 above this.

The low prices in the two largest States stemmed from cut-throat competition as a result of very low marginal costs in Victoria (where the fuel has no alternative uses) and marginal costs that were also low in NSW as a result of coal contracts being set on a take-or-pay basis. Over recent months, as a result of higher cost capacity in NSW being mothballed, prices have tended to increase.

ENERGY COMPETITIVENESS OF NON-FOSSIL FUEL PLANT

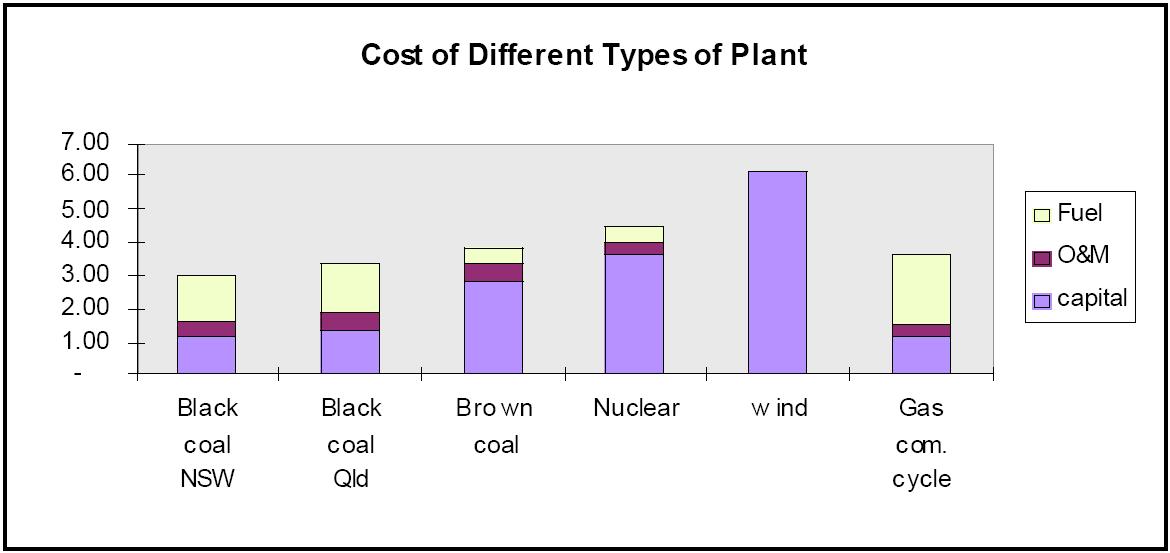

AUSTRALIAN COST ESTIMATES

Prices, at least in NSW and Victoria, are far below those that would justify the construction of new plant. The following chart is updated data derived from information in the main assembled by the Ecological Sustainable Development jamboree that the Hawke/Keating Commonwealth Government unleashed.

CHART 4

At the present time, Australia is more cost effectively served by coal fired generation than any other form. Based on an 8% discount rate and reasonable information about capital, operation and fuel costs, new power stations could be built to produce baseload power at prices that range from just under $35 per MWh for black coal and a little over this for brown coal and for gas (at a gas price of $2.70 per Gj). Coal fired generators may see prices lowered by some 15 per cent with the availability of coal gassification technology. Wind could be produced at under $70 but its value would need to be heavily discounted as it could be neither baseload nor peaking capacity.

Nuclear would cost less than $50 per MWh. Although this makes nuclear uncompetitive with coal, it would be close to competitive with a coal fired South Australian station. The quality of South Australia's coal means a new station is estimated to require a price of $46 per MWh and would also face some additional transmission costs. South Australia imports about one third of its requirements from Victoria.

A further difficulty with nuclear is the considerable size per unit. No nuclear facility of less than 500 MW would be viable and facilities are normally at least 1000 MW. Australia, coming as it has from a centrally planned direction, has a greater proliferation of large plant than would arise in a market founded on competition where plant flexibility commands a greater premium. For this reason, with the exception of Queensland, which is the fastest growing Australian market and where governments have been slow to commission augmentations, most new plant is envisaged to be smaller co-generation facilities or gas turbines which require a lower capital cost and can be built in smaller increments.

In general, abstracting from any greenhouse considerations, Australia's abundant and easily mined coal and especially Victoria's 1000 year supply of non-transportable brown coal, mean coal is likely to remain the preferred source of high capacity baseload plant. In the case of brown coal, research is already advanced on gas turbine technology. This is presently proven as a cost saving source for new black coal stations and represents the next generation of brown coal plants, ensuring the fuel remains highly competitive.

GREENHOUSE CONSIDERATIONS

SPECIFIC AUSTRALIAN CONSEQUENCES OF KYOTO

Australia has been allocated an 8% increase in emissions by 2010. Though far in excess of the levels the environmentalist lobby wanted to foist on us, this is not nearly enough to operate on a business-as-usual basis. Energy, and more specifically, electricity is the key to future reductions.

The PM's statement of 20 November 1997 encapsulated the latest estimates of where Australia stands. It also points to various market interventions.

The measures announced are designed to reduce emission growth, excluding land clearance, to 18 per cent by 2010. This leaves a gap of 10 per cent to be filled on the 2010 business-as-usual estimates.

One measure designed to foster reduced emissions is the specialist renewable energy innovation investment fund. This includes loans and grants totalling some $64 million for the subsidy of low greenhouse gas emiting electricity generation. Conspicuously absent from mention were the two most greenhouse free sources of energy production: nuclear and hydro.

Not costed in the P.M.'s November 1997 statement was a requirement that 2% additional energy from electricity is to come from renewable or specified waste-product energy sources by 2010. This means some 20 per cent of new generation is to come from these sources. It may be that such magnitudes of renewable supplies will be forthcoming as a result of improvements in technology by then. But such dividends from technology have long been promised and have failed to materialise.

At present costs, requiring exotic renewable energy sources would more than double the price of the electricity supplied. At two percent of electricity, it would require these doubled costs to be incurred for at least 4,000 GWhs of electricity, and on some interpretations considerably more than this. Four thousand GWhs is about four fifths the size of the Snowy hydro output. If the premium on this output is only 5 cents per KWh, this entails additional costs of some $200 million per annum. However, if the notion of waste-product energy is extended to cogeneration, the cost premium may well be less than 5 cents (may even be zero).

TACKLING FURTHER REDUCTIONS

Further reductions can be forced by use of subsidies, taxes, allocating tradeable rights to emissions or by command-and-control. Any such actions should avoid a focus on particular sources like thermal electricity. There are likely to be many circumstances where increased use of thermal electricity may actually reduce emissions. For example, where electricity replaces household coal or wood burning or where increased Australian electricity usage for transforming Australian raw materials means reduced energy used in transport and in transforming those same materials overseas. While Kyoto may be said to have settled the issue on the latter point, focussing only on electricity is likely to mean some lower costs options are foregone.

Economic instruments, taxes or tradeable rights, generate and harness the information about costs from a vast number of users and producers. They are, therefore, almost certain to bring about a more efficient outcome than if the control decisions were mandated by particular standards. This is due to market instruments making use of the same cost paring and profit searching incentives that have provided the higher living standards evident in market based economies.

Taxes set the price of pollutant emissions; the total amount of permits determine aggregate quantities of emissions, with individual permits being allocated initially on some basis such as current emission levels. Both taxes and permits signal the costs of pollution by putting a price on emissions. Taxes do so directly, by government decision, and permits indirectly, by forcing existing and would-be emitters to compete in the market for a limited supply of permits.

The alternative of using command-and-control regulation is inferior to market solutions for two principle reasons. First, it requires that regulators have intimate knowledge of millions of productive processes and their alternatives so that an optimum regulatory structure can be set. Secondly, it relies on decisions not being clouded by political exigencies.

Normally, the best way to estimate what will be the outcome of a regulatory action is to measure its effects as a tax. With some minor reservations, a tax and conferring tradeable rights have the same economic impact.

THE LEVEL OF TAX REQUIRED

Estimating the effects of tax or equivalent changes on price and then output is difficult enough one year hence and it is well nigh impossible a dozen years into the future. Even so, estimates must be made if we are to see where policy is leading us.

ABARE have estimated the tax required to stabilise Australian emissions at the Kyoto level to be $US34 per tonne of carbon dioxide in 2010. This works out at $A208 per tonne of carbon.

The basic tax at $34 per tonne of carbon dioxide is likely to understate the real effect because it is based on an international trading regime whereby the abatement is undertaken by those who can achieve it most cheaply. Although trade in carbon emissions, as with other goods, brings the most efficient outcomes, international trade has definitional and verificational difficulties. Thus, if tradeable rights are conferred on the avoidance of a supposedly intended facility overseas, especially in a country which is not bound by the emission limitation regime, there is likely to be trades in phantom emissions. These would amount to a business claiming to have installed more energy efficient plant in a particular country than had previously been intended.

EFFECT OF A CARBON TAX

The tax imposts required to abate Australian carbon dioxide outputs transform the economics of electricity generation. More than doubling the cost of generation will lead to an increase in costs to customers of some 70%. Electricity prices would still be low compared to those in many other countries but Australia would cease to be the low cost energy supplier that has attracted many processing industries. Our disadvantage would be compounded to the degree that the developing countries were exempt from the controls.

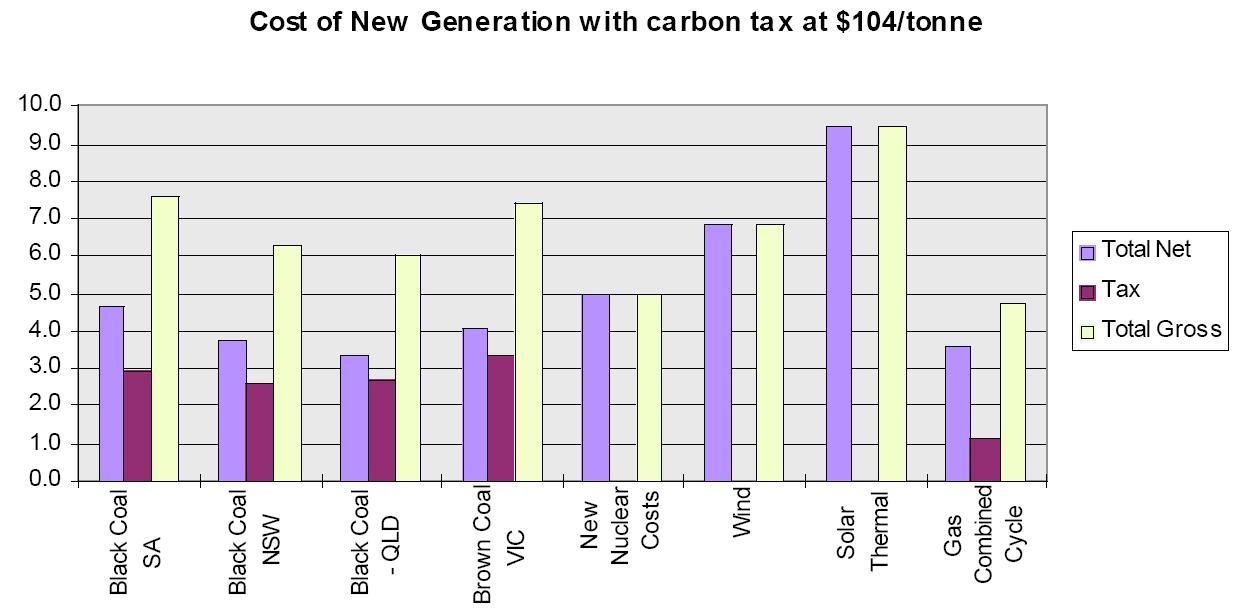

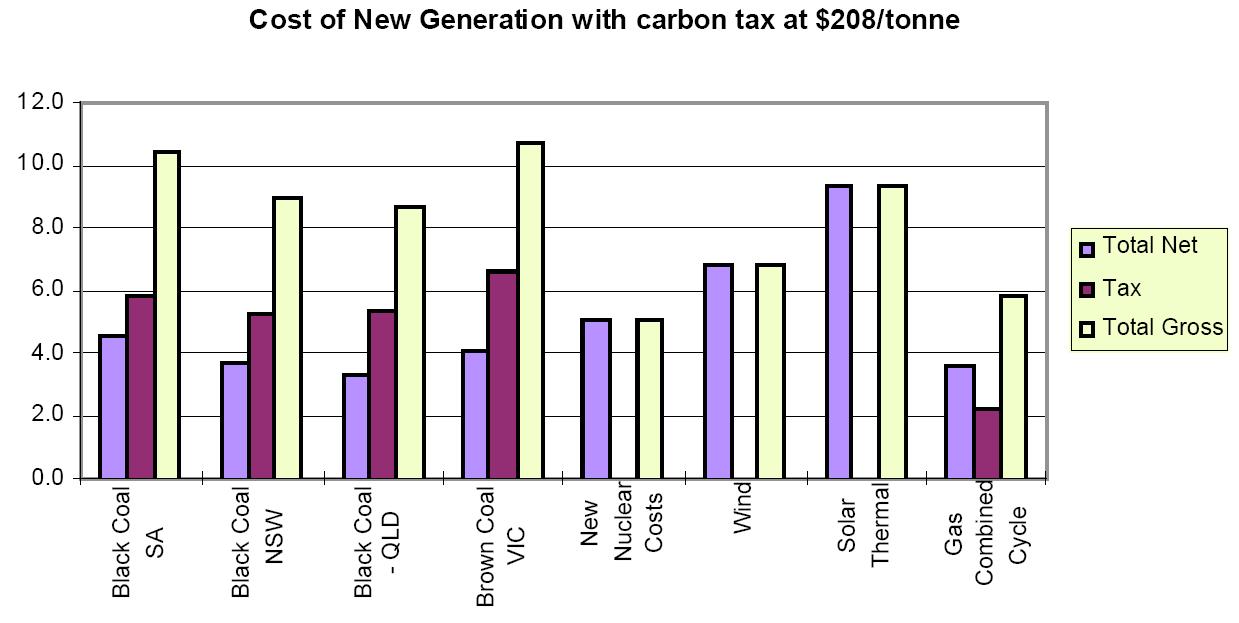

The following two tables measure the cost of electricity generation with a taxes set at $A208 and $A104 per tonne of carbon.

Chart 5

Tax set at $104 per tonne of carbon

Chart 6

Tax set at $208 per tonne of carbon

At a tax of $104 per tonne of carbon, coal is totally displaced and gas becomes the preferred source of new power. It is however likely that the price of gas would be pushed upwards by a rush of demand for it. Nuclear would then become competitive. Nuclear is clearly ahead at the tax rate of $208 per tonne of carbon. Although wind appears in principle to be more cost competitive than coal, especially with a carbon tax at $208 per tonne, its episodic operational characteristics make it unlikely to prove capable of supplying more than a very small fraction of demand.

CONCLUDING COMMENTS

Absent any greenhouse gas measures, with Australia's abundance of cheaply mined coal will entail it remains the dominant fuel source for electricity. Gas is likely to increase its share as the industry rebalances towards more flexible plant. Nuclear power is the only serious contender for base load and unlikely to be viable, except perhaps in South Australia. And in South Australia, the Pelican Point decision will have deferred any serious consideration of nuclear even if Australian governments had the stomach to resist the inevitable agitation. With greenhouse gas taxes or its equivalence in tradeable emission rights, nuclear would become the lowest cost option.

Much depends on the merits of the greenhouse fear and, more importantly, the Government's reaction to these. Greenhouse is far from an established phenomenon with severe effects on the planet. Signing an agreement is different from putting it into practice. An Australian Government has previously, with the 1992 Rio Treaty, agreed to reduce emissions of greenhouse gases under certain conditions and failed to do so. Furthermore, the US position is crucial and the Senate has already rejected a treaty that does not incorporate emission reduction targets of developing countries by 95-0.

Serious reductions in greenhouse gas emissions would have a devastating effect on the coal industry including a total eradication of Victoria's brown coal resources (worth at least $12 billion). Its knock-on effects would also require a massive restructuring away from resource processing. Any emission control measures, while presenting opportunities for some generation sources, would be clearly alien to Australia's national interest.

No comments:

Post a Comment