Keynote address to

Distribution 2001 Conference on Distribution and Transmission,

held in Brisbane on 12 November 2001

ENTREPRENEURIAL INTERCONNECTS

Views on interconnects range from those who see little in the way of future developments other than entrepreneurial interconnects, to the "planophiles". They range on the one hand from Tony Cook, whose Australian subsidiary has pioneered entrepreneurial interconnects, to Transgrid which sees very little role for them.

At the distribution level, the natural monopoly case is much stronger. In distribution networks, the only live case of duplication and competition is to be found in the Melbourne Docklands. There, two firms decided to build competing lines. Although the ORG placed some conditions on customer contracts that at least one of the competitors considers to be onerous, the outcome has been spirited rivalry and low costs with the two companies splitting the market roughly 50/50.

As far as distribution is concerned it is unlikely that we shall see more than occasional eruptions of head-to-head competition from two facilities. Competition is likely to be for the field itself.

Whereas distribution performs a function with no real alternative, a particular transmission line is an alternative to lines linking different generation sources and, like other forms of trade facilitation, an alternative to producing the energy closer to the market.

With regard to transmission, a recent report for NEMMCO by PriceWaterhouseCoopers and Clayton Utz suggests that we should build more common carriage interconnects with regulated returns.

This is premised on transmission costs being only 5-10% of electricity costs. Hence, the authors argue, the benefits of greater competition and lower prices through generator competition are more than likely to outweigh any inefficiencies.

A major problem with this argument is it fails fully to recognise the scarcity of capital. Moreover, the sort of interconnects we are talking about are longer and more sparsely used than the existing main body of transmission–Latrobe and Hunter Valleys to the respective metropolitan centres–and the 5-10 per cent is not an accurate guide. SNI, for example, would cost $500 per kW in capital for transport, which is similar to the cost of an open cycle gas turbine or half the cost of a combined cycle gas turbine. And that is just for the transport.

When, as part of the process for designing the electricity Code, I raised the possibility of market provided transmission, there was universal scepticism that anything other than a planned wires system would ever work, given free-rider issues, balancing problems and so on. But free markets were the essence of the Code and an obscure clause was introduced. Few, myself included, thought it would have anything other than a marginal application.

Indeed, there is still very little consideration of the notion elsewhere. None in the UK and it is absent from President Bush's 2001 Energy Policy document. Though the Bush policy waxes lyrical about the need to massively reinforce transmission lines, it does not consider anything other than some form of planned system. Eric Hirst's research for Edison Electric is typical of US injunctions when he says, "FERC needs to develop and implement transmission pricing systems that both ensure cost recovery for transmission owners and provide ... nada, nada, nada". The same old anodine strictures favouring sensible planning.

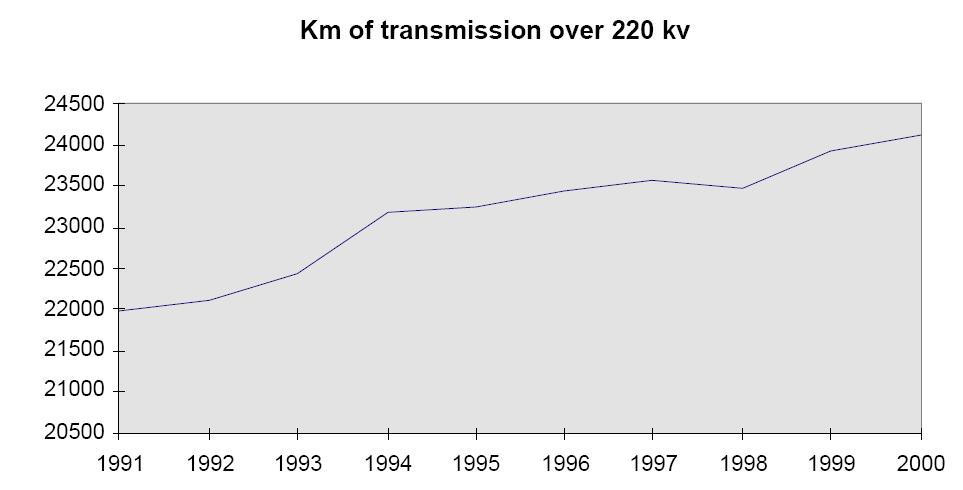

The fact is that transmission businesses have clearly been underwhelmed by the FERC regulated prices they have been offered. Transmission capacity in relation to demand has been steadily falling, a fall that the following chart indicates is increasing

Over the decade to 1999, transmission capacity (miles per GW demand) fell from 280 to 235. Over that period, demand grew 30%, twice as fast as transmission capacity. In real terms, annual US transmission investment halved over the 20 year period to 1999.

More recently, three entrepreneurial interconnects have been approved. The ubiquitous Transenergie owns one in New York. Black & Veatch and Siemens are proposing to build four power plants near coal mines in South Dakota and Wyoming. This will transmit 6,000 MW of power along DC lines at a cost of $11 billion for the plants and $4 billion for the links. Already approved is the Neptune Project with three cables, 3,600 MW in total, linking generation in Maine and Canada to New York and New England.

FERC has put conditions on these developments and it is not yet clear that they will prove successful.

Australian Transmission mileage has also shown less than a 10 per cent increase over the past decade, a trend similar to that of the US but one dictated by politics rather than economics for the period.

THE BENEFITS AND COSTS OF COMPETITION

PARTICULAR ISSUES IN ELECTRICITY

Bob Booth is one critic of market provision of interconnects. He is strongly in favour of regulated links, and has championed the Riverlink proposal in its various guises. Yet in his book, Warring Tribes, he documents the outcomes of government provision of transmission as being one of considerable waste, and in this respect cites the over-building of transmission capacity from the Latrobe Valley to Melbourne.

DC links offer scope for a link to determine whether or not it runs and therefore it becomes akin to a generator. This allows competition in transmission, the lack of which involves several adverse effects:

- gold plating; A notorious issue with government developed facilities is the tendency towards over-engineering. The Victorian transmission system is a case in point. The general consensus is that a private organisation would have been more parsimonious. Government organisations are less disciplined than private organisations to these cost/benefit trade offs because the decision makers have little financial stake in the outcomes. While excessive capitalisation is one result of government ownership, an alternative outcome is a squeeze on new developments where a government general budgetary position is strained. The electricity industry throughout Australia has seen feasts, as governments have climbed on particular rationales for developments, followed by famines as a result of general budget constraints. Such famines are rarer with the private sector since the absence of investment capacity by one firm would not prevent a rival stepping in.

- we also have a political response; Government owned and regulated interconnects allow considerable scope for the pursuit of political goals using ostensibly commercial motives. This obscures the merits of a particular proposal. It leads to misallocation of production, often in the cause of regional development or saving of jobs of those whose votes are particularly valuable.

- finally, there is crowding out; A regulated monopoly transmission is financed by a compulsory charge on consumers. This differs from the alternative means of supplying the capacity: new generation, and entrepreneurial interconnect or demand saving measures. A compulsory charge is likely to crowd out those alternative measures and deny us the most economic industrial blend.

THE FUTURE OF INTERCONNECTS

It may be that the future will see no scope for anything other than a market provided entrepreneurial interconnected system, at least for major augmentations.

At issue, on whether a line should be regulated or entrepreneurial, is whether it is:

- to allow improvements in reliability, spending that would be difficult to cover in fees, and

- expenditure for an augmentation.

Australian debate on these matters has taken place against the backdrop of the ongoing saga of Riverlink/SANI/SNI. The original application for a regulated link argued that only by having the revenues guaranteed could a major augmentation be built. The application got bogged down by definitions of what constitutes the benefits that a planner could count up to decide whether consumers would voluntarily find it in their interests to finance such a facility if they did not have the option of free-riding on it.

Meanwhile Transenergie went ahead and commissioned a significant facility without requiring customers to be press-ganged into paying. A change by the ACCC in the definition of what constitutes benefit has, at least ostensibly, incorporated producer benefits that would not otherwise be counted.

The trouble with all this, and with welfare economics on which planning rests, is twofold. First the planner does not face the same incentives nor have the same quality of information on costs and risks that is found in the real market; that's why planned economies and electricity systems are inferior to those that are market based.

Secondly, and more fundamentally, the apparent benefits added in the welfare economics case are invariably greater than those in the market case. This is because it is well nigh impossible to restrict all the benefits of a market development to those paying for it. For example, many consumers would be prepared to suffer brownouts and blackouts rather than face the costs of a new power station but once some consumers (those with the higher VoLL!) show a preparation to pay the extra costs the benefits flow to all. Similarly, the welfare economics calculus estimates the value people place on a new development and adds in all the "consumer" and "producer" surpluses. Market outcomes are limited in this by all-comers paying the same price. Much of the value of a welfare justified development should be discounted if its merits are to be compared to a market development. Otherwise it will divert capital to sub-optimal usages.

To reduce over-stating the benefits, in our own central planning we implicitly assume the new link will have no affect on the price. This is the opposite fallacy; it is inconceivable that the private sector would consider building a new facility without half an eye on the implications it would entail for the price of all outputs. Neglecting this tends to increase the relative value of a planned facility compared to that driven by market forces (an outcome that appears to have been overlooked in the PWC/Clayton Utz report which declared the present test to be biased against regulated links!).

GAS INTERCONNECTS

These issues are far less controversial with gas where all suppliers are basically agreed on the entrepreneurial solution.

The main issues in gas are how to prevent the regulators strangling developments by requiring low pipeline charges.

However gas interconnects compete with electricity interconnects and with other solutions to providing energy to the user. If electricity links are paid for by a regulated charge there will be a bias in their favour against gas links which have to find willing buyers. Incentives are created to site prospective power stations close to the source of gas and have the transport costs financed by a hidden levy.

Clearly there are many options for the supply of energy even if this is defined solely as reticulated energy. As well as electricity interlinks versus local generation versus gas links, there is potential competition from demand management. And local generation includes a raft of possibilities including biomass, wind, micro-turbines, co-generation embedded generation as well as power stations delivering on a transmission network.

Biasing regulation for or against any of these will mean we are less well off as a community. It may even undermine investor confidence in the regulatory framework.

THE SCOPE AND APPLICATION OF THE NATIONAL ACCESS REGIME

Access to eligible services may be through the NCC declaration process (1) (after which the ACCC becomes the price regulator) or directly through the ACCC issuing a legally binding and non-appellable undertaking.

Addressing potential distortions was at the heart of the Hilmer Report which was the well-spring of current competition policy and heavily influenced structural change in energy.

Ostensibly, the Hilmer Report did not differentiate between private and publicly provided essential facilities. It was however aware of the harm that could be visited on private property rights generally by regulatory seizure of some of those rights.

In reality the impetus for the Hilmer report was to redress the competition restraining effects of state government owned or controlled monopolies. In Australia in the early 1990s the only "essential facilities" were those businesses which enjoyed government support or protection from competition.

To develop policy in recognition of the twin importance of property rights and competition, there are six important classifications of essential service or bottleneck infrastructure. These can be developed into a taxonomy of regulatory approaches. They are:

- That which has been built without any market protection, especially that built since 1995 which is almost by definition "entrepreneurial" rather than regulated.

In this case the preference should be "no regulation" since the entrepreneur had no privileges in seeking to find the customers and their needs. - That which introduces new competition, even if this is not identical to existing facilities.

There is competition. No regulation should be put in place and regulation on the existing facility should be removed. - Privately built infrastructure built prior to 1995 that enjoyed no government protection.

The onus here should be on the authorities to make a case for regulation - That which is owned by the private sector but was built under a regime that offered protection from competition.

This presents a clear case for regulation but one that needs careful handling to avoid shutting out future competition. - That which was owned by a government but has since been sold under contractual terms to the private sector.

These should be regulated according to the contracted terms - That which was built by and remains owned by a government.

This if it is not to be privatised needs to be regulated though in a way that does not pre-empt rival facilities.

So, logically, new unprotected infrastructure built by private enterprise in the "post-Hilmer" era should not be required to grant access or be subjected to price restraints. The builders of such infrastructure are responding to a profitable opportunity that they foresee, one that, by definition, also confers gains on the buyers of the service. The two parties obtain a mutual gain. The sharing of the gain is one for bargaining between the parties but the consumers of the goods that the facility supplies cannot be worse off since without it they would not have that particular access route and perhaps not the product that the access delivers.

For its part, the owner of the new facility in this "post-Hilmer" era, cannot obtain gain from it by virtue of some form of government granted privilege. The owner will, moreover, usually be building a project that carries some economic risk. Such risk may emanate from a failure of the market to develop in the predicted way, new competitors, or the "howling gales of creative destruction" stemming from a technology that renders existing approaches archaic.

Achieving profits by better meeting market needs is at the heart of the private enterprise system. Attempts to "redistribute" such profits can only harm the process. This can be illustrated in the case of a new pipeline. The owner of the pipeline will usually have considered a spectrum of alternative market projections (and perhaps a spectrum of cost projections). There is uncertainty and, implicitly or explicitly, the owner will weight each scenario in making his investment decision. If his threshold is a rate of return of 15% and he is considering scenarios that might yield rates ranging from 25% to 5% but provide a weighted average rate of 15%, cutting off the potential to earn the higher rates will reduce the weighted average to something less than the threshold. The regulatory action would then eliminate the commerciality of the project. In such a case, the sponsor and the customers would both be losers.

Access regulation can have significant disincentive effects on new investments in infrastructure through its impact in reducing expected rates of return.

One of the most contentious issues arose as a result of the EAPL pipeline busting the Moomba-Sydney pipeline monopoly. We sought revocation of the coverage of the Moomba to Sydney EAPL gas transmission pipeline with the building of the rival Duke Energy line from Bass Strait. We also sought that the Duke Energy line not be covered. This provided a test about whether the NCC would "walk the talk".

We argued,

The Eastern Gas Pipeline means we have Coke versus Pepsi in pipelines to Sydney and the case for their regulation has disappeared. With the construction of the Eastern Gas pipeline, the conditions that could warrant either an undertaking or any other form of regulated price and access conditions disappear. The two pipelines themselves have considerable over-capacity and they will be engaged in a price war ... With two pipelines supplying an area, as long as there is no collusion, the case for regulation rests solely on the benefits to the regulators themselves.

The existence of two transmission pipelines serving NSW is the very definition of competition, the absence of which provided the initial rationale for regulation.

The NCC argued that they should regulate both pipelines since they did not traverse parallel routes and that, even if they did, regulation would still be necessary to prevent collusion! It is clear such analytical reasoning by the NCC gives regulatory agencies the opportunity to control virtually every economic activity in the country.

All this said, these notions of allowing freedom for unregulated entrepreneurial links need to be moderated by centuries of application of the common law as outlined by Professor Richard Epstein (2).

Epstein draws on the seventeenth century tract by Lord Matthew Hales de portabis mari ("concerning the gates of the sea"). In that tract, which was not published until the 1780s, Hales argued, that an asset (he was discussing cranes in ports) can be "affected with the public interest" either "because they are the only wharfs (sic) licensed by the queen" or "because there is no other wharf in that port".

This offers strong support for regulation even where the asset has been developed without any government support of protection.

In light of the historical evidence that governments will control essential facilities (and that such control is part of the common law) a workable approach would be that access regulation be reformed to provide explicitly for the use of "access holidays" in relation to new infrastructure projects.

This provides a means, rather like patent protection, of allowing successful entrepreneurial investments to gain the super-profits that motivates them, while not locking in higher prices forever. Equating an access holiday to a patent appears to be useful, insofar as it suggests that the access holiday constitutes an explicit recognition of the right of the facility provider to the return on his investment as the quid pro quo for his creation of new value.

The case for reduced regulatory oversight has received a chilling response from the ACCC. The Productivity Commission report on the matter is with the Government.

THE INTERFACE OF REGULATION AND FREE MARKETS

The importance of all these matters boils down to the pricing regime. The past few years have seen bruising disputes between the regulators and the regulated businesses over the appropriate rate of return for monopoly assets. Philosophically, the ACCC has a strong focus on the price gouging potential of monopoly in setting the synthetic market prices it aims at. This may be manifest in terms of the rate of return set, in the valuation of the assets themselves, or in excluding some assets from the total.

The tendency to bear down on price that the incumbent may charge also makes it difficult for rivals to enter the market. Ironically, regulators' decisions therefore tend to prevent competition, the very process they were created to enhance.

Naturally the regulators concoct material to persuade others that they are being generous in their decisions. Whether it concerns Telstra, GPU GasLink (now seeking to float itself at a 20% discount from its purchase price) or TXU networks (also apparently willing to take a capital hit), the outcome of Australian regulatory decisions has tended to reduce the values of the network businesses from those originally set by the market.

Many will argue that the original values were excessive, the fault of over-optimistic buyers, though this can hardly be said to be the case with Telstra where the Government set the price.

Although there may be a windfall to customers if the regulatory authorities set prices too low, the beneficial effects of this are highly transitory. The adverse impact of setting prices too low has several dimensions.

If an asset is valued incorrectly by the regulator, market forces will tend to self-correct this. But they will do so in ways that have damaging effects.

The effect of setting a transmission price that is excessive is likely to encourage new generation or some new rival transmission. These developments are likely to motivate the owner itself to set a lower price and the damage will probably be slight.

Setting the regulated price too low has consequences that are rather more severe. An asset that is priced artificially low will attract excessive demand and will "crowd-out" other, lower cost means of meeting the demand. It will tend to:

- encourage generation to site itself more remotely from markets;

- encourage excessive demand; and

- reduce demand for alternative fuel sources.

In addition to this, setting prices too low will lead to a reduction in its capacity and premature scrapping of the asset. Operators, faced with a return that is too low will not be successful in obtaining adequate funding for maintenance. The proposals will simply fail to make the hurdle rates and the owners will prefer to invest in assets where a better return is available. Lower expenditure on maintenance will bring a deterioration in the productivity of the capital and a consequent waste of resources.

Finally, prices set at lower levels than the market expects, whatever they are, will deter new investment.

CONCLUDING COMMENTS

Competition is the means of promoting efficiency. But its role is far more important than preventing sellers deliberately withholding supplies in order to allow higher prices and higher profits.

Competition is best regarded as having two functions, one generating "dynamic" gains and the other "static" gains.

The "dynamic" gains from competition stem from constant vigilance of many suppliers who need to cut costs and meet shifting market demands.

Commercial rivalry is superior to other arrangements in driving costs down. Competitive firms must constantly seek cost savings, and other ways of maintaining or improving their profits; these cost savings are largely converted into consumer benefits as rival suppliers adopt similar techniques.

The dangers are that, in seeking to redistribute the "static" gains, regulators and policy makers will close off opportunities for the more radical "dynamic" gains. For the latter gains to be achieved, the innovator must be confident that government action will not deprive him of the profits of success. This means having secure property rights. If policy and regulation results in property rights being impaired, this compromises a fundamental plank on which competitive efficiency is generated. For this reason, one of Government's most important role is ensuring the certainty that property will not be taken from individuals.

Requiring a low price for supplying a service where the supplier has previously sunk its main costs can be, in US terminology, a regulatory "taking". It markedly reduces the value and security of property rights. The initial adverse effects of this are felt on the firm whose value is partly expropriated but wider effects follow in deterring other firms contemplating similar activities.

ENDNOTES

1. or its related State certification process.

2. Richard A. Epstein Principles for a Free Society, Perseus Books, Reading Mass, 1998.

No comments:

Post a Comment