A Speech to the Utilicon TasPower Conference,

9 April 2002

WHAT HAS ENERGY MARKET DEREGULATION DELIVERED

Virtually all jurisdictions everywhere in the world are moving to the competitive energy market model. The realisation that competition, preferably linked with private ownership, pays rich dividends in terms of efficiency has brought institutions like the World Bank to search for opportunities to apply the model even in markets smaller than Tasmania. Fortunately for Tasmania, there is the opportunity of joining the national market which allows the State to take advantage of established means of improving efficiency and lowering electricity costs. Whether Tasmania is positioning itself to allow itself to take full advantage of this is a matter I'll return to later.

The outcomes of deregulation around the world have not been comprehensively documented. This is largely because the key outcome, prices to customers, has been obscured either by a phasing-in process, especially for the smaller customers, or because prices for competitive customers are not collected because they are confidential to the seller. Moreover, prices of electricity, like those of other commodities, tend to be somewhat cyclical.

What we can be fairly certain of is some broad trends. In the UK, NETA, the latest market model, has brought a claimed 15% price reduction (on top of the 30% real reduction 1990-2000). In Australia, we saw prices for larger customers fall 28% 1996-1999 according to a number of surveys. Prices for smaller customers were reduced by regulators.

Underpinning these price falls have been large increases in efficiency. For example, in Victoria the generators since being moved into a more competitive setting (following corporatisation in 1994 and their subsequent privatisation) have seen their workforces shrink from about 11,000 to the equivalent of less than 2,500. At the same time other efficiency measures like availability-to-run have been lifted from the high 70s to the mid 90s. In terms of energy price equivalents this has seen an average spot, albeit in the context of a financially distressed generation industry, down from a level of about 44 cents per kWh to 25 cents.

On top of this we have seen improved efficiency further downstream. Costs and staffing levels have been trimmed in retail activities and in distribution and transmission. The privatised businesses in Victoria moved swiftly to take control of their labour relations, in the context of which workforces had long been padded and work practices ossified by union controls under the old SECV and its local municipal distributors.

In addition, we have seen a steady drop in minutes off line and in other indicators of improved service.

THE ROLE OF THE ELECTRICITY RETAILER

As retail margins are only about 5 per cent, some are perplexed by the prominent role given to the retailer in the judgements about the liberalisation of markets and, implicitly, about how they correspond to consumer benefit.

Under competitive circumstances, the retailer is the de facto agent of the consumer. That role is assumed of necessity–if abandoned or neglected a rival will step in. The retailer's activities, to ensure its on-going success and even its existence, must extend far beyond passively breaking down bulk and ensuring products are delivered at convenient locations. It must extend to assisting in discovering what the consumer wants. Unlike self selected (and often government financed) consumer "representational" bodies the retailer is compelled to be the agent of the consumer, as long as the consumer can move to an alternative agent if the retailer provides unsatisfactory service.

The retailer is an agent in a far more comprehensive sense than any representative body because it has to weigh up the needs against the available product inputs–and to do so correctly or face replacement. The retailer is under great pressure to seek out inputs from all sources.

The homogenous nature of electricity does not negate this. Electricity may be undifferentiable but its supply is from highly variable sources. In terms of assembling inputs, the retailer must decide, based on its customers' and target customers' requirements:

- how much power to contract rather than buy at pool

- how much of different sorts of power (baseload, regular peak, needle peak) to buy

- how much price risk to take for the needle peak.

In addition, this basic product has to be metered correctly, bundled in profitable packages, promoted to consumers who may have little awareness of their needs and options, and priced appropriately. The retailer also needs to examine economies of scope (or synergies) in bundling his goods together with other similar products, sharing services of specialists like meter readers, back office functions etc..

Competition between retailers does tend to ensure that, for a given quality, products are purchased from the cheapest producers and sold on to customers at margins that are not excessive in relation to efficient retailers' costs. Competition is also, and perhaps fundamentally, a discovery process, whereby the competitors set out to ascertain the needs of customers, where those needs are not well defined by the customers themselves.

In this respect, retailer competition has played a vital role in guiding developments. A competitive retail market forcing retailers to act in the interests of their customers, has meant a close focus on costs and product sourcing. Competitive retailers has also meant experimentation with new marketing tools:

- more than one of the Victorian retailers is experimenting with direct debiting of customers' accounts;

- Energy Australia is insisting on interval metering as a condition for the installation of three phase systems for air conditioning.

Generally the greater customer orientation has meant retailers better focussed on needs and, in the current context, being prepared to pay more for peak power or fast start, thereby encouraging the development of such plant.

It bears repeating that retailers are not the agents of the consumer out of any sense of benignity but because they must act in such a role if they are to keep the business. Their essential pre-occupation with profitability means they will raise prices to either discourage customers who impose to high a cost on the services they can offer or to better align the costs those customers entail with the prices they charge.

FRC EXPERIENCES

The foregoing indicates the dangers of simply treating electricity retailing as an automatic function that can be easily replicated by a smart regulator. Joskow, Hogan and others (1) have suggested that we can make do with a simple pass through tariff from wholesale and line charges to the customer. This proposition has drawn a sharp response from Littlechild. (2)

The pass through tariff is essentially what NSW's ETEF brings. By fixing NSW wholesale prices, it stultifies competitive provision, while also imposing a risk, low but still palpable, of a colossal loss by government should pool prices zoom up for a lengthy period. Over the longer term it will bring mismatches in energy requirements and availabilities as retailers have a much reduced incentive to signal needs by contracting forward for new supplies.

The ability of NSW consumers with annual loads of less than 160 MWh to take the fixed price means that the controls will continue to hamper market development in NSW for some time to come. The most direct evidence of this is the tiny amount of retail churning we have seen in the State since the theoretical implementation of FRC. Similarly, we have seen the growth of financial products being reversed.

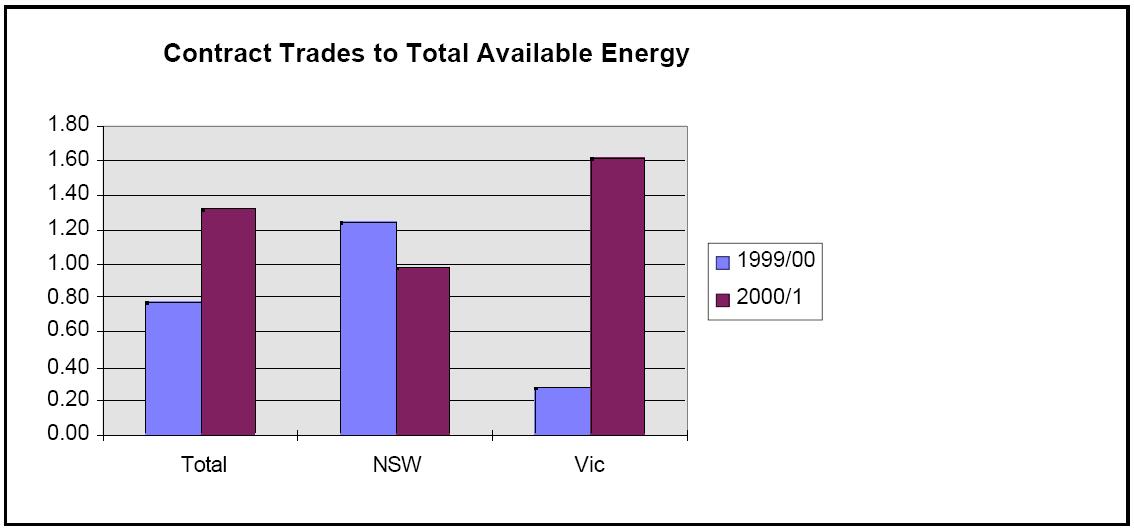

In relation to the energy market, the turnover of contracts in NSW declined last year while that of Victoria increased fivefold. Victorian retailers and generators were seeking out ways of defraying their risks but in NSW there was far less need to do so because the Government has mandated a form of insurance through ETEF. The following chart is based on AFMA data, which is far from comprehensive but does depict an accurate contrast between the two major Australian markets.

In this respect the Parer Energy Market Review paper argued, "Government ownership of both electricity generation and retail businesses appears to provide a natural physical hedging opportunity, alleviating the need to maintain substantial financial contract positions to manage risk exposure. This may restrict the volume of trading on financial markets and has the potential to hinder or distort the efficient and timely development of deep and liquid financial markets."

It might be argued, indeed is argued by those like Quiggin, that the market outcomes are entirely possible without retail competition. And so they are. The trouble is that in the absence of competition, those low cost, efficient outcomes never emerge or at least are never sustained. It takes competition to jolt suppliers into undertaking the research and cost saving measures that serve consumer needs.

In the UK there has been much debate on the merits of full retail competition. Although by no means opponents of competition, NERA have suggested that full retail competition in the UK has not been worth the price. They argue that the associated IT costs of customer transfer and lack of metering at the small customer level requiring deemed load profiles means we cannot have true competition. It is true that the arbitrary designation of load profiles severely detracts from the benefits of competition at the small customer end. In fact it has a perverse effect in highly peaked markets like Victoria where retailers have an incentive to chase the high-usage domestic loads. As this generally means those with air conditioning, it exacerbates the peak problem. (3)

But to rule out competition for half of the load would mean jettisoning a vital entrepreneurial dimension to energy efficiency on a sustained basis. This means the on-going role for regulatory oversight. Our experiences with this have not been satisfactory. It generally leads to institutions holding down retail prices.

Holding down retail prices

- reduces incentive and wherewithal of new players to emerge

- reduces the incentive of players to contract for new supplies

- at same time boosts demand

California here we come

The Victorian Government's decision on standing prices for below 160 MWh customers has produced levels of competitive activity below that expected in a full retail competition environment. In aggregate, retail prices have been held down to levels much lower than those sought be the retailers who have faced a steep rise in wholesale prices. And while price controls have their justification for monopoly services like distribution lines, they are not justified for those open to competition.

The upshot in Victoria has been only about 4,000 households have switched retailer over a three month period and the marketing activity of host retailers has been subdued. This compares with a net 50,000 per week changing retailer in the UK. And while churn is not the goal per se, it is an indicator of an active market. More pointedly, the decision prompted the owner of one retailer (CitiPower) to announce that it is seeking a buyer, while it was doubtless a consideration in the decision of Pulse's owners to sell.

Unless prices are allowed to adjust to the underlying cost shifts, retailing will be seriously harmed and the consumer is the eventual loser.

In this respect, Victoria's recent decision also placed a 3% upper limit on the deviation from the average price allowed of the maximum price for individual customer classes This cements-in distortions, making it easier for new retailers to avoid those customer classes whose tariffs have become highly unprofitable. Preserving cross subsidies is the outcome and intent of such glue being placed in the machinery. The Victorian Government also gave a subsidy to rural consumers which is well and good as long as it comes from general revenue and is not a hidden charge on other consumers. Unwinding of these cross subsidies is precisely the sort of outcome expected of markets and stymieing this blunts an important aspect of the efficiency promoting features of competition. A further danger is that the host retailers will gradually be left servicing the highest cost customers.

All this said one might ask what is the relevance of the schedules to FRC such as the following?

| Jurisdiction | Electricity | Gas |

| NSW | 1 Jan 2002 | 1 Jan 2002 |

| Victoria | 13 Jan 2002 | 1 Oct 2002 |

| ACT | Under review to be announced March 2002 | 1 Jan 2002 |

| SA | 1 Jan 2003 | 1 Sep 2002 |

| WA | 2005 | 1 July 2002 |

| NT | 2005 (subject to public benefit test) | n/a |

| Tasmania | 2007 | 2007 |

| QLD | No plans at this stage | Jan 2003 (subject to cost/benefit study) |

At this point of time the NEM jurisdictions already have half of their load free to competition and ostensibly NSW and Vic are fully freed up. But this is clearly of limited real value if there are measures in place like price caps or compulsory insurance that depress prices and undermine the creation of financial instruments on which competitive markets can prevail.

TASMANIAN IMPLICATIONS

Retail Contestability

Tasmania's proposed market opening was as follows (it was amended somewhat by the ACCC).

Table 3.1 The Tasmanian Retail Contestability Timetable

| Commencement (from Basslink start) | Expected Date | Contestability Limit | Approximate No. of additional uncontracted customers | |

| Tranche 1 | 6 months | 1 October 2003 | 20 GWh/yr | 10 |

| Tranche 2 | 18 months | 1 October 2004 | 4 GWh/yr | 54 |

| Tranche 3 | 30 months | 1 October 2005 | 0.75 GWh/yr | 295 |

| Tranche 4 | 42 months | 1 October 2006 | 0.15 GWh/yr | 1,030 |

| Full contestability | 54 months | 1 October 2007 | Under 0.15 GWh/yr | 230,000 |

Source: Meeting Tasmania's Energy Needs for the 21st Century: A Competitive Future, Tasmanian Treasury. November 2000, p41.

This probably puts inadequate pressure on Aurora but the nature of the State's contracts would arguably dictate such a timetable.

GENERATION

More important is the wholesale market and generation. It is not possible to have retail competition operating effectively if there is no generation competition. I want to go back to the words I used in preparing the part of the Nixon report that covered electricity.

"In any type of market, there is always a danger of one or two, usually large, generators exercising market domination. Tasmania has 27 hydro electric power stations plus the irregularly used Bell Bay thermal station and power from Mt. Lyell. But in terms of major storage, Great Lake and Lake Gordon accounted for over three quarters of the stored energy in 1996. This raises the issue of controlling potential market power."

I went on to suggest that Tasmania could explore unitization of these dominant reservoirs, a procedure followed in oil. And while arguing for privatisation of the HEC, I also argued that the generation business should be split into five different entities which roughly correspond to the catchment areas.

Those separate entities were as follows.

| Catchment | Storage GWh | 1996 energy GWh | Number of Power Stations | Capacity (MW) |

| Gordon-Pedder | 4724 | 812 | 1 | 432 |

| Derwent | 1989 | 2726 | 10 | 514 |

| South West | 7299 | 1008 | 3 | 380 |

| West Coast | 340 | 2896 | 6 | 626 |

| Northern | 116 | 1687 | 7 | 308 |

Now there may be better ideas on how the HEC should be split up but it is clear that Tasmania will have inadequate competitive pressures if the one dominant firm is ensconced as a supplier. And the control by that firm of Basslink prevents any competition other than that of Duke. In the future we might see more robust competition with Bell Bay mark II at 234 MW on top of the repowered government owned facility. But all this seems a long way off.

In the meantime the ability of the Hydro to constrain Basslink would not allow any mainland generator the ability to risk offering contracts in Tasmania. That ability can mean driving up prices in the Tasmanian wholesale market in either the peak or off-peak by conserving water. Nobody would enter into contracts in Tasmania without assurances about the hedge price and, especially where a competitor controls the transport medium, without a firm hedge.

On top of this electricity regime, the Government is not being helpful in facilitating competition with gas. As a major competitor, gas can help place market disciplines on electricity supply. But the Government has insisted on franchises for gas rather than letting retailer/distributors negotiate for wholesale supplies and proceed to roll out and sign up customers. This has delayed roll out and might add further delays to the degree to which it requires franchisers to commit to a particular timetable.

Customers in Tasmania, as elsewhere, cannot be well served on an enduring basis if there is a monopoly. And experiences in Australia and elsewhere in the world are that a government owned monopoly is even worse. At least in the case of a private owned monopoly there are built-in pressures pare costs but a government body tends to be run by the employees and be subject to political rather than commercial forces.

It might be said that splitting hydro generation would reduce scale economies, detract from the abilities of the HEC to undertake consultancy services, and might impede the coordinated control of water supplies. I don't believe any of these arguments are persuasive. Splitting the HEC would still leave the component parts larger than many hydro concerns including Southern Hydro and many hydros, including Southern and Snowy, find ways to coordinate water that is jointly used.

The concerns about Tasmania that prompted the Nixon report have not abated since then, indeed the malaise in the State's economy has become even more apparent. Hence, irrespective of National Market issues, Tasmanians should reflect on whether it is in their interest to retain electricity generation under a publicly owned monopoly.

It rarely serves the public interest for governments to be mesmerized by size in attempting to create national champions. Iconic issues aside, preserving and on-selling Tasmania's hydro expertise is probably the most important reason for maintaining generation under a single business. But the consultancy work of the Hydro is a modest contribution to the economy and in any event can travel just as well if it is housed in small units as in one larger firm, especially if the latter is cocooned from competitive pressures.

REFORM RECOMMENDATIONS

In short, Tasmania should break up the Hydro into 3-5 competing units, place Basslink on an independent and commercial footing (and, to the degree that commitments are in place, ensure that government reimbursement is open and clear) and re-examine its timetable for retail contestability.

It should sell off the different generation units as well as Aurora.

Its electricity policy should be supplemented by a hands-off gas policy. No exclusive franchises should be given and no price assurances and roll out conditions should be put in place. Gas is going to be a predator fuel for some time and the retailers will need to and be willing to give assurances to customers that locking in capital to use gas will not result in future squeezes. Such assurances will emerge from market forces and need not require government.

ENDNOTES

1. For example, Paul L Joskow, "Why do we need electricity retailers? Or, can you get it cheaper wholesale?" Center for Energy and Environmental Policy Research, Massachusetts Institute of Technology, revised discussion draft, 13 January 2000

2. Littlechild, S.C., Why we need electricity retailers:A reply to Joskow on wholesale spot price passthrough, The Judge Institute of Management Studies, University of Cambridge, September 2000.

3. In Texas according to a McKinsey article, around 305 reduction took place where metering allowed charges (prices were not specified); see Power by the Minute, February 2002. Faruqui et al report Georgia Power saw similar load reductions for their "most responsive' group with interval meters at prices of about 30 cents per kWh; see Regulation Fall 2001 Getting out of the dark.

No comments:

Post a Comment