Backgrounder

Summary

A fundamental objective of measuring corporate reputation is to regulate corporate behaviour. Faced with vocal constituencies who want to divert the corporation from its commercial objectives, the corporation can choose one of two strategies: to play the reputation measurement game, or not. The danger in playing the game is to be ensnared by new regulation. In its 2002 questionnaire to Australia's top 100 corporations, the Australian Conservation Foundation asked for assurance that, "the company's environmental performance is beyond the minimal standards set by environmental legislation and other forms of regulation". (1) The ACF and other NGOs who participated in the same exercise would prefer a far more extensive level of corporate regulation across the entire spectrum of corporate activity than is currently expressed in Australian law.

In the debate about the proper relationship between corporations and society, often coined "corporate social responsibility", NGOs are non-state or civil society regulators. (2) This Backgrounder reviews the Fairfax-published Good Reputation Index, and argues that the Index should be construed in terms of a competition between the state as the regulator of "acceptable" corporate behaviour, and advocacy NGOs and the media as regulators of "good" corporate behaviour. It concludes that corporations who played the game were rewarded with a good label, those who refused were labelled as bad.

The Index is poorly administered, lacks objectivity and confuses reputation with performance. The Index is a tool in a campaign against the corporation and its freedom to promote its commercial objectives, consistent with the rule of law and the objectives of its owners and other significant contracted parties. Fairfax and participating corporations should abandon the Index forthwith.

INTRODUCTION

Corporate reputations are a serious business; corporations strive hard to ensure that their reputation is maintained in the best condition at all times. Presumably they do so because it is a component of business success. Which component is difficult to ascertain. Indeed an entire academic journal, the Corporate Reputation Review, is devoted to that question. The rationale for the interest in reputation measurement is, it appears, because reputation "is a growing factor in maintaining corporate competitive advantage". Apparently, because factors such as "media congestion" and "fragmentation" and "the appearance of ever more vocal constituencies" (3) make it so. These factors place pressure on corporations to differentiate themselves from their competitors and to examine their actions and "stakeholder perceptions" of them. If one accepts such reasons, then it follows that, "[t]o be managed, corporate reputations must be measured". (4)

There is little doubt that corporations use non-commercial dimensions of performance to gain a commercially competitive advantage. Corporate philanthropy is an early example of this proposition. The corporation will want to compete in dimensions that have widespread acceptance, low compliance costs, and provide maximum benefit. If the dimensions expand to a point where they interfere with the commercial purpose of the corporation, however, and grant new players the power to direct the corporation, corporate involvement in such ventures must be seriously questioned.

The Good Reputation Index was published by The Age and The Sydney Morning Herald newspapers in 2000, 2001 and 2002. The Index purported to examine, "through the perceptions of community stakeholders and experts", the ability of the top 100 corporations operating in Australia, (5) to manage those activities "which directly contribute to their reputations as socially responsible organisations". (6) In fact, the Index does no such thing. The Index begins with preferred definitions of goodness and expands these, for example by measuring financial performance, to capture the whole reputation of a corporation and labelling the result "social responsibility".

The Index was based on performance across six major categories -- Management of Employees; Environmental Performance; Social Impact; Ethics and Corporate Governance; Financial Performance and Management and Market Focus. In each of these categories, Reputation Measurement Pty Ltd, a private company, selected a range of "community based experts" and "stakeholders" (called research groups) to provide their opinions on the performance of each company. Each research group was responsible for its own questionnaire, and for the rating of each corporation.

Westpac was ranked number one on the Index in 2002. It rated well in every category. (7) By contrast, Flight Centre was ranked number one on financial performance, but 47 overall. (8) It was in the doldrums in every other category, including being ranked 99 on environment. On the surface this seems very strange, given that Flight Centre manages shopfront travel agencies! At its AGM on 31 October 2002, the managing director announced a 37 per cent increase in profit on the previous year. Was this achieved in some socially unacceptable way? It appears not. Not only was there no suggestion that Flight Centre transgressed any laws, it seems to have satisfied its two principal "stakeholders". Shareholders received increased dividends, "with payments rising from 27.5 cents a share in 2000-2001, (excluding the special dividend), to 37.5 cents in 2001-2002." (9) The rise in profits was achieved on a 20 per cent increase in revenue, and shop and business numbers grew from 778 to 975. No suggestions of mass redundancies. In fact, when the growth of the business placed pressure on the recruitment and training of new staff, the company responded with the acquisition in New Zealand of a training college specializing in travel. Moreover, a share ownership scheme is available to facilitate employee participation, as is a Business Ownership Scheme for managers. In two recent years, Flight Centre was named Australian Employer of the Year by the management consultants Hewitt and Associates of Sydney. That rating was not based on the attitudes of NGOs, but on the responses of employees to a questionnaire.

Toll Holdings, the Melbourne-based logistics and transportation corporation was in the top 10 financially, but ranked 65 overall on the Index. (10) Toll Holdings announced substantial increases in earnings and profits at its AGM on 31 October 2002. (11) Toll has an integrated management system which incorporates Environmental, Workplace Health and Safety, Government and Legislative requirements and the pursuit of continuous improvement. Their Occupational Health & Safety Policy states that, "[i]t is unacceptable for any individual to observe non-compliance with safety standards without immediately addressing and correcting that non-compliance with the personnel concerned." Their Environmental Policy states that,

Legal compliance is regarded as a minimum standard and actions beyond statutory regulations, which conserve or protect the environment and support business goals are encouraged. The company participates in recycling programs, and promotes conservation of natural resources such as, electricity, fuel and gas. On all company premises, particular attention will be given to the storage and transport of Dangerous Goods, containment of run off from workshops and washdown areas, and the safety and integrity of underground fuel tanks. (12)

In the face of all this, why is Toll in the bad books?

The answer for Westpac, Flight Centre and Toll lies in one fact. The extent to which each was prepared to accept the agenda of Reputation Measurement. In establishing the Index, Reputation Measurement argued that "there is increasing evidence to suggest that companies seeking to demonstrate their worthiness as socially responsible organizations are most successful when they widen their traditional business stakeholder base to include community stakeholders." Further, "[i]nvestors and consumers are increasingly making decisions based on longer-term issues linked to a company's capacity to contribute to a sustainable future for all." (13) In other words, the Reputation Index is an instrument for advancing a number of political agendas: corporate social responsibility, stakeholder capitalism, and sustainability. Each corporation that participated in the Index needs to be able to justify the three agendas to its shareholders.

SOCIAL RESPONSIBILITY

The key question in the discussion of corporate social responsibility is, "what is good?" Does good mean commercially successful, long-lived, popular among workers or consumers or investors or the community at large? Indeed does any measure of goodness have anything to do with the commercial purpose of the enterprise? This is the first hurdle at which the Index stumbles. It establishes a method which implies that a corporation needs to be something other than a commercial entity in order to be good. It assumes that the corporation needs to be a model citizen. Further, it loads the concept of the good citizen with far higher expectations than it would for individual citizens. Is a good citizen one who earns a lot of money, but then, after paying taxes gives a lot of it away? Does a good citizen account for all of their deeds as they may affect the environment? As parents are they fair to their family, and do they have to account for this? What of citizens' dealings with their neighbours and workmates? The notion of corporate social responsibility suggests a relationship between, for example, a corporation's output and the community's perception of whether a corporation does good work in the community. The suggestion is seductive, it suggests a parallel between corporate reputation and democracy. There are two parts to the seduction.

First, in a democracy the electorate votes on the basis of performance and perception of performance. Perception may belie actual performance. Corporations that cannot rely on actual performance alone to make business gains may have to rely on the perception of performance. Unlike the politician, however, the corporation is selling a more well-defined product than the "competence to govern". The political consumer is far less able to make up their mind on whether to purchase, than the corporate consumer who can do so simply on the basis of a product or service. Nor do governments come with a money-back guarantee! Perceptions no doubt play a role in corporate reputations, but they are hard pressed to overcome the more readily measured commercial performance and compliance with legislative and contractual obligations.

Second, the eligibility to vote for corporate performance is far more restricted than universal adult suffrage. And so it should be. Those with a real interest in a corporation are not the community at large but particular individuals who have a specific relationship with the business. Each of these individuals and groups will make their assessment on whether to purchase from the company, work for it, work with it or invest in it. They will do so less on the basis of a broad "competence to govern" than on factors such as price, quality, wages, prompt payment and rates of return on investment.

In a democracy, the rules by which corporations carry out their activities are set by consensus. The consensus determines rules across a very wide spectrum of financial and non-financial criteria, but it determines not so much what is good, but what is and what is not, acceptable behaviour. The law also provides penalties for unacceptable behaviour. The Index, on the other hand, is an exercise among civil society activists who wish to appropriate the resources of corporations for their own purposes. It has little to do with corporate goodness, it has a lot to do with increasing the power of NGOs to impose their agendas, which include the appropriation of property (corporate reputation) and the further regulation of corporations.

The Index is extraordinarily arrogant in its assumptions about knowing what is good. It is possible to measure corporate performance so as to enable those interested to assess whether and how they will deal with a corporation. But "measures" of reputation by groups (some of whom have an adversarial relationship), and others who seek a commercial relationship with the corporations, is at best subjective. To produce a single figure of which corporation is good and by implication, which corporation is bad, is heroic. Although each research group disclosed its direct relationship to a corporation, it was reported that some of the research groups had touted for work by offering their services to corporations in filling out the questionnaire. These approaches were not disclosed. (Incidentally, the Index is published by Fairfax, but the Fairfax reputation is not measured. It may not be in the top 100 corporations, but it should subject itself to the same bias to which others are subjected.)

Goodness, when not defined in a consensual manner, is an act of rent-seeking. No amount of moralizing about goodness has been known to revive a commercially unviable corporation. When a corporation ceases to exist, it does so because it can no longer pursue its intended commercial objectives. Without the commercial objectives -- and these may include profits, growth, market share -- there is no possibility of pursuing good corporate citizenship. Goodness cannot be allowed to threaten the commercial viability of a corporation. On the other hand, "acceptable behaviour", when based on a widespread political consensus is less likely to interfere with the real contribution that corporations make to society.

STAKEHOLDER THEORY

Stakeholder theory suggests a model of the corporation in which all interests in an enterprise compete to obtain benefits from the enterprise, but that none has a priority. This simple proposition is very confronting, because it is in effect posing the question, "in whose interests should the enterprise be run?" (14) It also assumes that society grants an enterprise the right to exist. Those whose business it is to advise corporations on social responsibility are fond of arguing that corporations have a licence to operate in the community. This is accurate at one level only, the community through its law-makers may grant licences and certain privileges in return for the enterprise complying with the law, it does not license the activities of stakeholders at large to impose their views on the corporation.

Nor does the theory satisfactorily answer the question of who, or what, produces economic value. Instead "its focus is on the distribution of outcomes, the harms and benefits, and not on who produced the harms and benefits. It assumes value is produced by the enterprise itself and that stakeholders have a claim on some of this value because the enterprise is a creature of society." (15) It radically overturns the social contract for business which includes obligations to obey the law, honour contracts and agreements and respect the rights of others. It ignores the fact that economic value is produced by owners who make their savings available to other member of society to put them to use in productive ways. The owners have an exclusive moral claim to the benefits produced by their activities, as others have a moral claim for the benefits produced by their labour or other contracted services.

Those with a contractual relationship with the corporation have rights. The breach of contract with a supplier, the dangerous product sold to the consumer, the accident that befalls the worker, the investor who is misled by a prospectus -- each is entitled to pursue the corporation for the recovery of losses. Indeed, the corporation can also pursue any of these individuals for breaches of agreement or misrepresentation and so on. Ultimately, the managers, on behalf of the owners, are responsible for all of these actions. Poor management may result in losses all around -- workers lose jobs, suppliers lose contracts, investors lose money. But only the owners through the managers decide the nature of the enterprise, its purpose and direction. Whom they choose to deal with and how, within the bounds of law and custom, is a matter for them. Which is not to say that "stakeholders" will not have a say, but only in the course of settling matters to the satisfaction of the owners. To assume that everyone starts with an equal say is to assume there is no ownership. There is a suspicion that this is precisely the assumption underlying stakeholder theory, the denial of the rights of ownership.

A second strand of stakeholder theory focuses less on equating the interests of stakeholders with shareholders, and more on their ethical treatment. This means that stakeholders, employees, customers, suppliers, owners, financiers and the community should be treated fairly and justly. (16) This thinking is consistent with those who regard the corporation as no more than a process for grievance settlement in society at large. For example,

One of the most significant things that companies could do to make themselves good "stakeholder corporations" is to ensure they give ... rights to external review, to stakeholders (and stakeholder groups) with legitimate complaints about the company. The right to access justice -- to be able to make claims against individuals and institutions in order to advance shared ideals of social and political life and to rectify relations that have gone wrong -- is an essential part of citizenship in a contemporary democracy. (17)

And further,

We are unnecessarily constrained by the belief that the representative institutions and legal system of the state should be the exclusive or even the primary, home of political deliberation. (18)

Fortunately, stakeholder theory has no basic recognition in Australian Corporations Law. There is no current case law or provision that requires directors to take into account the interests of stakeholders, or the sometimes touted concept of "the interests of the corporation as a whole". (19) While there is no prohibition on directors from considering other interests they can only do so provided there is a prospect of commercial advantage for the company.

One of the principle dangers of stakeholder theory is that it can be invoked by managers who can claim to be serving the general interests of society in the name of the public good. Such claims are not within the powers of managers. Only those with a mandate from the public, like politicians, can make such claims, and they only do so cautiously, in the knowledge that if they do so wrongly, they will be punished.

SUSTAINABILITY

Sustainability refers to ecological sustainability, and ecological sustainability is premised on the notion of limits to growth, based on limits to resources. It argues that natural resources are becoming scarcer. It ignores the history of technological innovation, often promoted by competition between corporations, and that such innovation has extended physical resources in ways untold. In fact, judged by price, physical resources are becoming more abundant over time. For example, the environment category of the Index contains questions about the level of corporate electricity and water consumption. It is highly unlikely that conservation and/or recycling will assist in any problems that arise from some future shortage of these resources. Pricing for externalities or to take full account of infrastructure costs is sensible, but pricing for conservation is very unlikely to produce sensible choices among alternatives. The solution to the so-called limits to resources will be found in technological innovation.

One obvious innovation with clear and positive implications for resource use is genetic engineering in food production. Unfortunately, the issue is raised in the questionnaire in such a way that it carries the clear implication that this is environmentally harmful. There are questions as well about greenhouse gas emissions, but elsewhere about nuclear energy production, also with the clear inference that this is forbidden. The environmental agenda is not broadly shared, nor without controversy, it assumes no trade-offs and that abstinence rather than adaptation or innovation is the cure.

The questions in the Index are based on an ahistorical view of sustainability. They represent a very narrow concept of sustainability, an insular and frozen view of human ingenuity. One of the main principles of sustainable development is intergenerational equity, the achievement of which assumes that this generation knows the needs of future generations. Conserving what are considered resources today does not ensure the future is secure, and using them today does not necessarily mean that tomorrow is in jeopardy. Petroleum was not considered a resource 150 years ago, but today it is vital. Consider the following conundrum:

If the choice to draw down resources is held exclusively by future generations, then we, being the future generations of previous generations, have been deprived of that right. Does it make sense for us to condemn our ancestors, who were poorer and much less secure than we are, for using resources to support themselves? Does sustainable development really imply that no generation has the right to use resources, no matter how urgent their needs will be? (20)

The research groups who want to judge the performance of corporations on the environment and other dimensions have a very particular view of what constitutes good. There is no reason why corporations or the rest of the community should share it. It is clear that NGOs are seeking greater regulation by incorporating a wider array of factors. The Australian Conservation Foundation wants to "amend the Corporations Act to ensure that Australian companies report fully on their environmental and social impacts, on material risks (such as greenhouse liabilities) and on breaches of environmental or social standards"; and, "create 'open standing provisions' within the Corporations Act that would permit any person to commence enforcement provisions for breach of the Act". (21)

Those corporations who choose to use the language of sustainability, as well as corporate social responsibility and stakeholder as a way of forestalling tougher regulation may find that their strategy of "ingenuine compliance" simply keeps misleading concepts alive longer than they deserve. Better the regulation debate be placed in a consensual forum such as the Parliament.

THE DATA

The Index is published as a single rank as well as in six categories. This minimizes the criticism that one figure can describe a corporation's performance on so many contradictory dimensions. Who would use the combined figure suggesting one overall rating? Clearly, no-one who has actual business with the corporation. The Index is designed for "society at large", in fact for no-one in particular, so it is really for professional moralists who have no interest, literally or figuratively, in the corporation, or indeed its suppliers, investors or workers.

For specific users, however, the data are available in each category and may conceivably have some utility if the data were relevant. Ideally, it would enable the worker to be informed about wages, training, promotion prospects, safety and other work conditions and so on. It would enable the supplier to know about the record of timely payments, contract conditions, and the investor to know about returns, or perhaps some moral aspects of investments. Further, they may assist a worker to evaluate a trade-off between wages and training, a consumer between price and quality, an investor between returns and investing in desirable industries.

Whether the data are sufficiently informative for each of these users is doubtful, because the Index uses perceptions rather than performance data. Where performance data are available they are useful, but they need to be disentangled from other measures -- for example, shareholder return versus shareholder satisfaction with returns. The over-riding aim seems to be to provide a headline-grabbing list of goodness. This raises the broader issue of whether a corporation can really satisfy all stakeholders equally. It may, in the procedural sense of listening to their demands, and that is useful, but at the end of the day when trade-offs are to be made, can the Index predict which corporation will be the best at adjusting to the external environment, the first to cut its workforce, the most likely to sell a product that is faulty, the most likely to go broke? There is much in the measurement of what corporations do, so much so that measures of perception of vague notions of goodness simply get in the way.

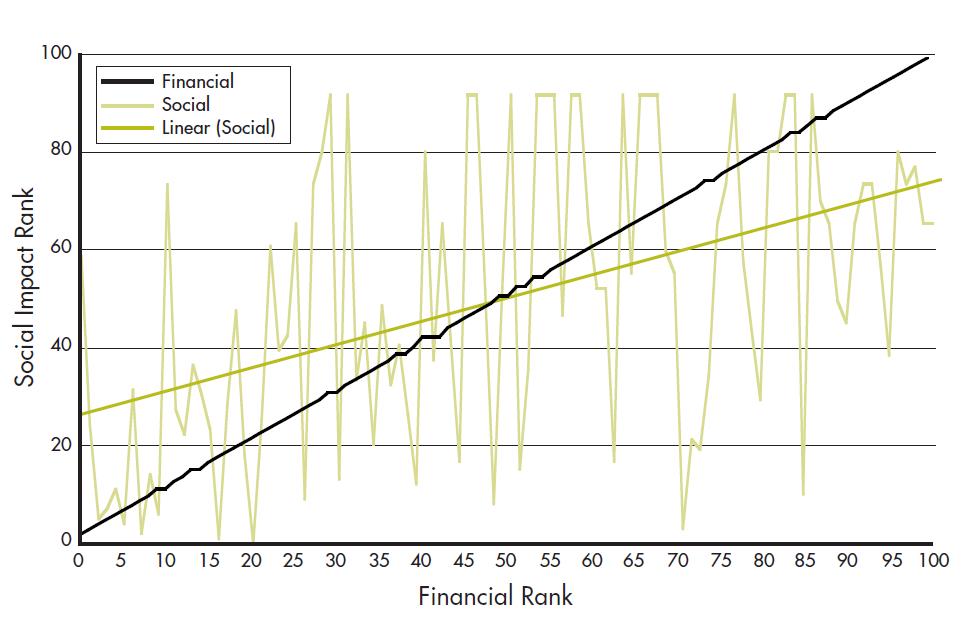

Presumably, the promoters of the Index argue that it is possible to be good in all dimensions, that trade-offs can be made without detriment to anyone's position. Should there be an inverse relationship between environmental performance or any of the five dimensions and financial success, or a positive one? These hard issues of cause and effect, of contribution and trade-offs are all avoided, they are all assumed away. Let this analysis proceed on the assumption that the primary measure of performance of a corporation is its financial success. Each category is compared with the financial rank of the corporation and the results discussed.

FINANCIAL PERFORMANCE

In the first instance, is the Index's measure of financial success valid? The Financial Performance category consists of eight measures undertaken by three research groups. These measures were combined to create a single rank. The Australian Shareholders Association surveyed its members on satisfaction with shareholder returns, quality of information to shareholders and their assessment of the skills of directors and management. The weakness in this method is that it turns a potentially objective and comparable measure such as shareholder returns into a matter for shareholder perception. Why not just list the returns? An assessment of the quality of information could validly be carried out among shareholders, though there is no detail to suggest that the Shareholders Association did so. An assessment of the skills of directors and management is too broad and unfocused to be credible. Again, there is no detail of the questionnaire, but even a highly-rigorous assessment of the skills and experience of management carried out by means of a study of the actual personnel may have some use (although some would argue that the proof is always in the results they generate). But a survey of shareholders' perceptions of such matters reduces the measure to the level of tea room gossip. Moreover, as the survey involved 1,500 members and comments were asked of 100 companies, it is highly likely that there was little or no information on a number of corporations. In these instances, corporations were given a mean (that is, average) score.

The measures employed by the Institute of Chartered Accountants appeared valid. They consisted of two measures of return on shareholders' equity based on published financial statements. The Securities Institute of Australia ranked corporations on the credibility of financial performance, credibility of senior management and volatility/risk. Survey questions were sent to participants for information on audit committee, risk management and compliance. The problem was that 42 corporations did not respond. The fact that most were ranked at the lower end of financial performance suggests that non-cooperation was a significant factor in the rating. A panel of "professionals" assessed the credibility of senior management, but no detail is provided as to how this was achieved. The volatility/risk scores were based on financial data.

The financial performance rankings have some weaknesses, with a bias on the basis of participation. At least some of the criteria were objective and related to the commercial purpose of the corporation. There are, of course, many acceptable and readily available measures of financial performance of Australia's top corporations. These are available for publicly listed companies at the Australian Stock Exchange and regularly announced at AGMs.

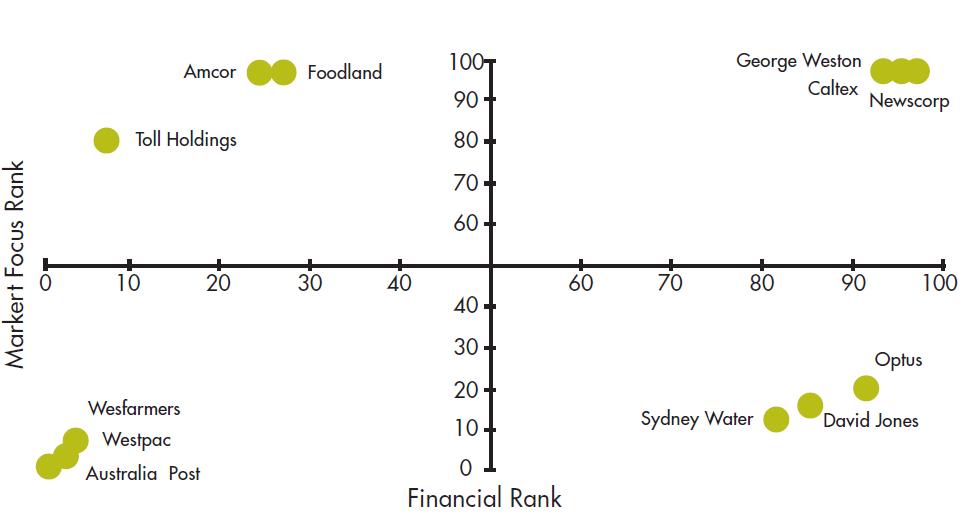

In addition to its relationship to the commercial purpose of the corporation, the Financial Performance category has one strength, it is well differentiated. A few corporations share a rank, but these are spread across the full range of rankings. It therefore provides some basis for comparing the performance of corporations on all other categories. The validity of each measure is discussed below, as is its relation to the financial performance measure. Two charts are presented for each category. The first chart (Chart a) plots on the horizontal axis each corporation's financial rank, starting with the highest at the bottom left corner. On the vertical axis each corporation is ranked on a second category. The second chart (Chart b) plots the performance of a number of corporations that are ranked either very high or very low on the two categories. This creates a typology of corporations characterized as follows.

| "Bad Rich Corporation" Toll Holdings | "Bad Poor Corporation" George Weston Foods |

| Westpac "Good Rich Corporation" | Sydney Water "Good Poor Corporation" |

Using this typology, the Index suggests that Westpac, one of Australia's four major banks is a "good rich" corporation. Toll Holdings, the Melbourne-based logistics and transportation corporation is a "bad rich" corporation. George Weston Foods, one of Australia's largest food manufacturers, is a "bad poor" corporation. Sydney Water, a statutory corporation owned by the NSW Government, is a "good poor" corporation. Why and how they and many other corporations came to be categorized like this is discussed below.

EMPLOYEE MANAGEMENT

The Employee Management criteria consists of 10 measures undertaken by three research groups. These measures were combined to create a single ranking. Employers First is the new name for the NSW Employers' Federation. By way of survey or referring to its "own data base", Employers First sought to rank corporations on their contribution to "substantial levels of direct employment"! To this inane question, all of Australia's largest 100 corporations scored well. Except, that is, for the 43 for which a nil score was awarded because they did not respond (nor apparently did Employers First have anything in their database). The second question was whether the corporation had a fair and reasonable approach to the settlement of industrial disputes. There was no indication of how the judgement about what constituted fair and reasonable could be made. For those who responded or were in the database, all scored top marks. Again, 43 received a zero score. The third question was whether an effective human resources management system was in place. Again no indication as to how such a judgement could be made, again perfect scores for all, except the 43 non-responders who scored zero. In short, the Employers First contribution to the state of knowledge about Australia's top 100 corporations was useless.

Diversity@Work is a Commonwealth Government-funded organization whose job is to assist corporations diversify their workforce. The essence of the four questions it asked was to establish whether corporations recruited people from diverse backgrounds and whether they could substantiate the fact. These questions created considerable differentiation among those who replied, but 42 corporations did not reply and were given a zero rating. The Australian Council of Trade Unions asked three questions on industrial relations. The questions were founded on measurable factors such as the formal recognition of union representatives, whether the corporation responded to awards and had a comprehensive equal employment opportunity policy. The ratings, however, were judged by individual affiliates which may have caused problems in the comparability of the standards measured. In all, 25 corporations were not able to be assessed and were given an average score by the ACTU.

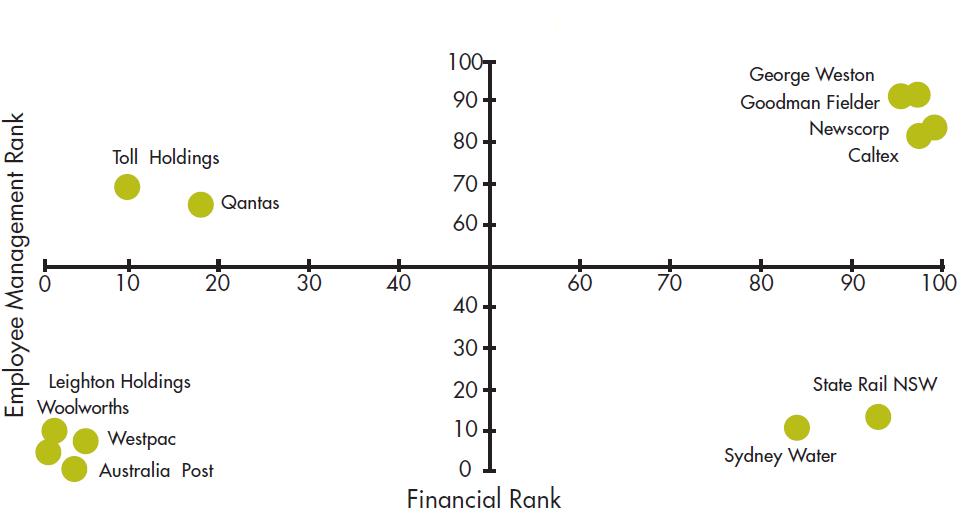

Overall, on the Employee Management measure, 17 corporations had the same rank of 92. These 17 were awarded a medium score by the ACTU and a zero score by the other research groups. In other words, these 17 were awarded this low rank on the basis of no evidence. Further, these occurred in the bottom 30 corporations which suggested that not only was the measure poorly differentiated, but that the same poor rank was awarded to a large number of corporations which adversely affected their overall rank. Chart 1a suggests the paucity of the differentiation, due mainly to a lack of response, reflected in a weak positive relationship between financial performance and employee management.

Chart 1a: Financial Performance and Employee Management

Chart 1b reflects the scores on the two dimensions, finance and employee management. They indicate stark differences in corporation performance, apparently sufficient to suggest that some were good and some were bad. The trouble is that the difference between corporations in this typology is that the "bad capitalists" did not respond to the survey and the "good capitalists" did. In terms of the efficacy of the Index as a research tool, can it be said that poor employee management is the cause of the poor financial performance in some cases, or that good employee management performance is the cause of a good financial performance in others?

Chart 1b: Financial Performance vs Employee Management

SOCIAL IMPACT

The Social Impact category consisted of 16 measures undertaken by four research groups. These criteria were combined to create a single ranking. None of these groups asked questions that involved impact on the local community, nor sought to ascertain whether permission was obtained by shareholders for any philanthropic causes undertaken by a corporation. Amnesty International asked whether the corporation was committed to the Universal Declaration of Human Rights! This is an extraordinarily arrogant question that implies that a corporation that does not run its operations according to this declaration is bad. Moreover, as the only aspect of human rights that corporations control are working conditions and remuneration, and poor practices are proscribed by Australian law, the question, in effect, seeks to invoke a lower standard of human rights than is the experience in Australia. Unless it seeks to further damage its reputation, Amnesty International should not participate in the Index in future. This opinion was in all likelihood shared by 47 corporations who did not respond to its questionnaire.

The Australian Business Arts Foundation sought evidence that corporations gave money to cultural activities. There was no question as to whether the giving bore any relationship to the commercial purpose of the corporation. Forty-seven corporations did not respond to the questionnaire, although AbaF used other sources to give a score to every corporation. As their four questions were of a yes/no type, scores could only be awarded in 25 percentiles. World Vision sought a corporation's impact on global poverty. The assumptions behind the World Vision questions are heroic indeed. Basically, World Vision, and the aid lobby in general, discount the poverty alleviation that corporations make by creating wealth, instead mistaking the corporation for a citizen or a government. In addition, it makes the highly contentious assumption that wealth transfer eliminates poverty. Many corporations agreed that World Vision was asking the wrong questions and 46 did not respond. Of those who did respond or agree with World Vision, there was no evidence presented that the managers obtained permission from their owners for such use of their funds.

The Enterprise and Career Education Foundation was established by the Commonwealth Government in 2001 to enhance the prospects for students to make a successful transition from school to work. The questions were based on measuring a corporation's involvement in such activities. These questions were somewhat related to the commercial purposes of the corporation, but only 56 corporations replied. Of those that did, the scores were well differentiated. Those that did not were given a nil score.

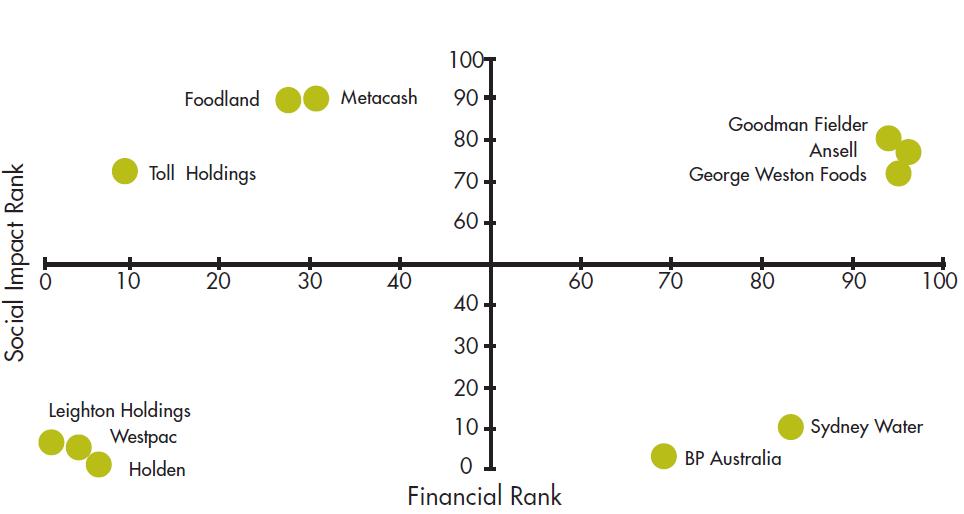

Overall, on Social Impact, 18 corporations had the same rank of 91.5 and 17 of these occurred in the bottom 30, again suggesting poor differentiation and a penalty effect in the overall rank. Chart 2a suggests a weak positive relationship between financial performance and social impact, not a surprising result given the level of non-response and the irrelevance of the agendas attached to many of the questions.

Chart 2a: Financial Performance and Social Impact

Chart 2b reflects the scores on the two dimensions, finance and social impact. They indicate stark differences in corporation performance, apparently sufficient to suggest that some were good and some were bad. Like the previous category, the difference between corporations in this typology is that the "bad capitalists" did not respond to the survey and the "good capitalists" did.

Chart 2b: Financial Performance vs Social Impact

ENVIRONMENTAL PERFORMANCE

The Environmental Performance category consists of 14 measures undertaken by five research groups. These measures were combined to create a single ranking. The Environment Protection Authority Victoria sought answers on three aspects of the corporations' management of environmental impact, including the transparency of corporate activity and whether it complied with all legal requirements. The number of non-responses was not disclosed, those corporations which did not respond were ranked anyway on the basis of publicly available information. The positive aspect of the Authority's survey was that it acknowledged the importance of compliance with the law and therefore the standards set by legislators as being the appropriate standards to determine good behaviour. The same was not true for the three advocacy NGOs who sought to rate the corporations.

Chart 3a: Financial Performance and Environmental Performance

The Wilderness Society, Greenpeace and the Australian Conservation Foundation each surveyed corporations with a view to finding out if corporations were complying with the NGO campaigns. In this venture, the Wilderness Society acknowledged that it "had a limited understanding of many of the companies environmental strategies and performances". This did not stop them from rating each corporation. Greenpeace was very aggressive in its attitude to corporations, "To enable us to verify your responses, please provide us with further supporting documentation. If this is not provided and we are unable to verify your response, we will default your response answer to a 'don't know' which will be marked and downgraded accordingly". Neither Greenpeace nor The Wilderness Society indicated how many corporations refused to comply with their questionnaire, but the Australian Conservation Foundation indicated that only 50 corporations responded. Non-respondents were nevertheless rated on the basis of publicly available information and other NGO sources. The Monash Centre for Environmental Management sought answers to three sets of questions seeking whether a corporation had identified environmental risks, developed appropriate management tools and was able to measure its performance. These questions were less prescriptive than the NGOs, concentrating on process and self-identification of risk, as opposed to the Greenpeace type of question, "are you a producer of greenhouse gases?" MCEM did not disclose the number of responses to their questionnaire, and used "supplementary sources" to rate each corporation.

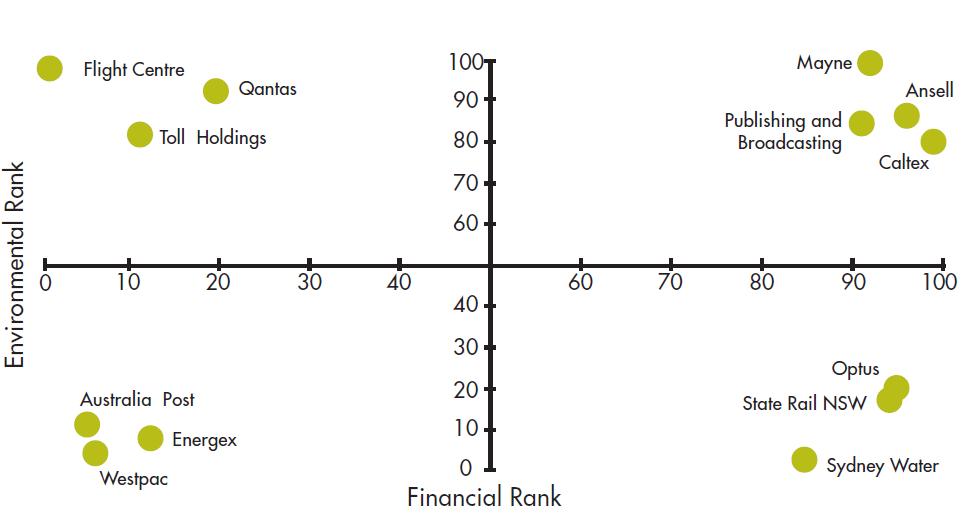

The Environmental Performance measure is well differentiated suggesting no undue influence by non-response -- apart, that is, from the deliberate penalty for non-response awarded by some research groups. This means that the non-responses do not overtly weigh the distribution toward the poor achievers. There is also a verification problem because many of the groups used their own sources to judge performance. The trend line for environmental performance is very flat, which indicates no relationship between financial performance and environmental performance.

Chart 3b reflects the scores on the two dimensions, finance and environmental impact. They indicate stark differences in corporation performance, apparently sufficient to suggest that some were good and some were bad. Like the previous categories, the difference between corporations in this typology is that the "bad capitalists" did not respond to the survey and the "good capitalists" did.

Chart 3b: Financial Performance vs Environmental Performance

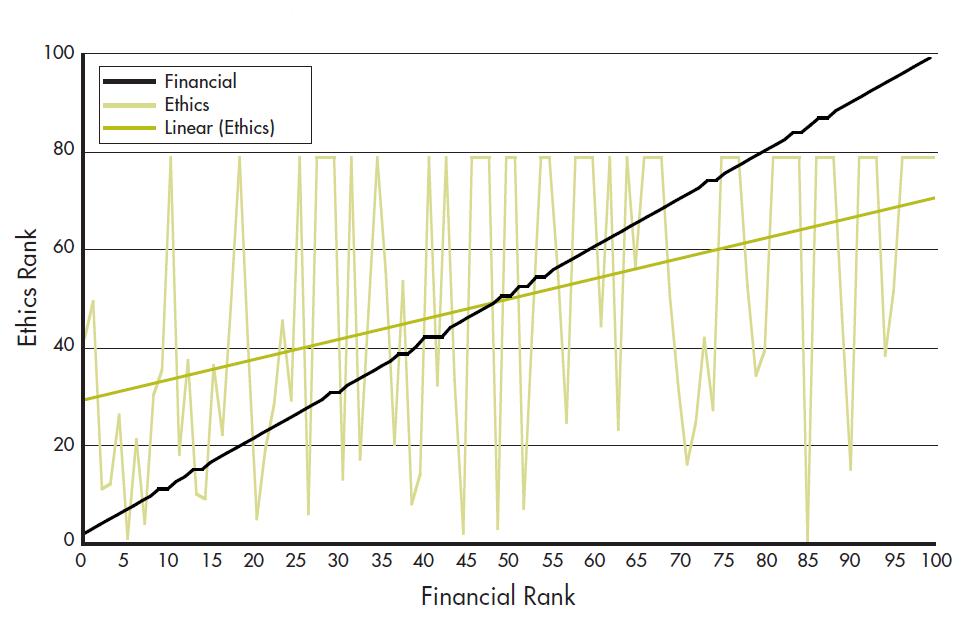

ETHICS AND CORPORATE GOVERNANCE

The Ethics and Corporate Governance category consists of 14 measures undertaken by four research groups. These measures were combined to create a single ranking. The Ethics Network, a private consultancy of business ethics specialists surveyed corporations on a written code of conduct and efforts at meaningful audits. Forty-seven corporations did not respond and these were punished by being awarded zero points. The Brotherhood of St Laurence surveyed internal ethical systems and external relations. Forty-four corporations did not respond and these were rated at zero. The Institute of Corporate Governance and Accountability surveyed the inclusiveness of ethics and governance standards and the integrity of methods. Despite using public sources of information there was no response from 45 corporations, who were rated zero.

Chart 4a: Financial Performance and Ethics & Corporate Governance

Oxfam-Community Aid Abroad sought evidence in these areas: the right to a sustainable livelihood, to basic social services, to life and security, to be heard, and, to an identity. These questions are an embarrassment. They imply a standard of "human rights" far below that experienced by any Australian employed by any of these corporations. For example, the criterion for a "living wage" is positively Third World and ignores the legal and economic reality of Australian working conditions. (22) Questions that ask if the corporation gives to the relief of humanitarian crises elsewhere in the world or contribute to social services in the local area are, as for individuals, a matter of choice, not public policy. Forty-nine corporations seemed to take similar umbrage and did not respond. There is also a clear case of doubling up in the survey, as many of the Oxfam questions were asked under the social and employee management sections.

The Ethics and Corporate Governance criteria is extraordinarily undifferentiated, with 43 given the same rank of 79, fully 41 of whom are ranked in the bottom 41 overall. In other words, all the research groups have decided to penalize the non-respondents, all of whom are placed at the same poor rank. The result is that there is no credible relationship between financial performance and ethics and corporate governance. It should also be made clear that the questions which implied that giving is good are not a dimension of ethics or of morality. Rather, they are a dimension of values and a particular ideology that affects the aid industry. As with so much of the survey, the answers only serve to expose the agenda of the research groups, the advocacy NGOs and attendant interest groups.

Chart 4b reflects the scores on the two dimensions, finance and Ethics and Corporate Governance. As in earlier charts, they indicate stark differences in corporate performance, apparently sufficient to suggest that some were good and some were bad. The difference between corporations in this typology is that the "bad capitalists" did not respond to the survey and the "good capitalists" did.

Chart 4b: Financial Performance vs Ethics & Corporate Governance

MANAGEMENT AND MARKET FOCUS

The Management and Market Focus category consists of 11 measures undertaken by three research groups. These measures were combined to create a single ranking. Standards Australia sought to establish the level of commitment to formal management systems, continuous improvement and risk management. On all four criteria, scores out of 7 only varied between 3.5 and 7, and 43 corporations did not respond. The non-respondents were awarded zero. The Australian Institute of Management sought information on four criteria: business and employee leadership, employee training, customer satisfaction and commitment to innovation. Corporations were asked to self-assess, though 43 declined to respond. The non-respondents, in contrast to almost all other research groups, were nonetheless awarded a mean (average) score. While this does not punish the non-respondents, it does by default rank the corporations on the basis of questions by other research groups in this category.

Chart 5a: Financial Performance and Management & Market Focus

The Consumers' Federation of Australia sought answers on three criteria based on consumer rights, complaints resolution, and on the needs of customers, suppliers and contractors. The Consumers' Federation questionnaire had a very high response rate, which may indicate that it was asking corporations to report on matters that were germane to their purpose. The scores, however, measured in the range of 1 to 7 did not fall below 4 and a 7 was rare, which allowed for little discrimination between rankings. Eighty corporations received a rank between 67 and 76 on the Federation's score.

The Management and Market Focus measure is poorly differentiated with 27 corporations receiving a score of 80, 26 of whom occur in the bottom 40, and 7 which received a score of 97, also suggesting an undue influence on overall performance by an undifferentiated measure. There is a weak positive relationship between the two measures as indicated by the trend line.

Chart 5b reflects the scores on the two dimensions, finance and Market Focus. As in earlier charts, they indicate stark differences in corporate performance, apparently sufficient to suggest that some were good and some were bad. The difference between corporations in this typology is that the "bad capitalists" did not respond to the survey (except that of the Consumers' Federation) and the "good capitalists" did.

Chart 5b: Financial Performance vs Management & Market Focus

DID THE INDEX INFLUENCE CORPORATE BEHAVIOUR?

The research groups and Reputation Measurement, and indeed The Age and The Sydney Morning Herald have engaged in the exercise of corporate reputation measurement presumably in the hope of changing corporate behaviour. One way of testing such a proposition is to look at the change in the rankings of corporations between 2001 and 2002.

Chart 6, Major Changes in Rank 2001–2002, displays those companies whose rank changed most dramatically from the 2001 survey to the 2002 survey. Five corporations rose between 40 and 60 places in the ranking in this period, and four corporations slid between 40 and 60 places. How did they achieve these feats? Each company was contacted for their answer.

Chart 6: Major Changes in Rank 2001–2002

Western Power Corporation, owned by the Western Australian Government, rated much better on the second occasion because it began participating in the United Nations-inspired Global Reporting Initiative. This meant that the survey was more readily completed, but the rise in the ranks was more a measure of effort in filling out the form than from any change in behaviour.

Sigma rose dramatically between the two surveys, apparently on the basis of a combination of a rise in its share price, which gave it a sharp rise in investor relations, and the fact that it took the time to fill out the questionnaire more thoroughly on the second occasion. Despite this intention, however, the work on filling out the survey on the second occasion was stopped two-thirds of the way through because it was taking up too much time. This was a common complaint among respondents. Apparently, the second survey occurred at a time of cost-cutting and declining staff morale, which did not show up in the survey. In essence, the company was rewarded for participating in the survey, but there was no change in its behaviour in response to the survey. Business proceeded as usual.

Tattersalls rose dramatically in the rankings for the very simple reason that they participated in 2002, but not in 2001. In 2001 they were ranked without their participation. Their reward for playing the game was to receive a good reputation, but their behaviour as a corporation, other than to cooperate with the reputation regulators, did not change.

Mitsubishi increased it rank by 42 places because it filled out the survey on the second occasion. Mitsubishi did not participate in 2001 but were nevertheless ranked on the basis of the opinion of the NGOs and expert groups. Because of their poor performance in 2001, the company decided to participate in 2002. Again, the reason for the steep rise in the rank was the same -- they cooperated. They reported no change in their behaviour between 2001 and 2002.

Boral did not perform well in the first survey, a matter which was raised by a group of shareholders at its 2002 AGM. Boral resolved to put a great deal more effort into responding to the survey in 2002. They did so, and were rewarded with a jump of 56 places. They did not, however, change their business behaviour. Their reputation was enhanced, their business behaviour was unchanged.

The companies that slid down the ranks provided answers just as enlightening.

Telstra participated in the 2001 survey and scored a middle rank. They were not happy with the nature of the survey, however, and declined to participate in 2002. They were punished in 2002 with a drop of over 40 places.

Fosters participated in 2001 and declined in 2002. They seem to have been punished with a series of zero rankings and a drop of nearly 60 places.

Telecom NZ participated in the 2002 survey, but only in the parts where they thought the questions were relevant to their business. They were not confident that some of the research groups were competent to judge their performance, indeed that they understood anything about their business operation.

Goodman Fielder did not participate in any aspect of the survey. Not participating on either occasion raises the question of whether the strategy of Reputation Measurement was to punish the non-respondents. Certainly the decision by most groups was to award a zero, as opposed to a mean rank for a non-response.

It seems clear that participation in the survey did not change corporate behaviour. This means that the survey failed to achieve one of its aims. Perhaps it had an impact on one of the key stakeholders, the shareholders?

DID THE INDEX INFLUENCE STAKEHOLDER BEHAVIOUR?

A further test of the impact of Index and corporate behaviour is to look at the change to the share price of the corporations which were subject to large variations in their rank between 2001 and 2002 (Chart 6 corporations). The Index was published on 28 October 2002, shortly before the AGM season for many corporations listed at the Australian Stock Exchange. It appears that the research groups intended their work to influence shareholders and thus corporate behaviour.

Although it is difficult to suggest any direct relationship between share price changes and the Index, there is undoubtedly a view shared by the non-state regulators that they should use the power of publicity to alert shareholders to change their corporation's behaviour for the better. Indeed, as Boral reported, the shareholders at the 2001 AGM "waved the Index in front of the Board" seeking answers to Boral's poor rating. Were Boral and the others whose reputation rose rewarded by the shareholders? It appears not.

Western Power, Tattersalls and Mitsubishi are not listed on the ASX, but Sigma and Boral are. Sigma's shares rose at the time and immediately following the publication of the Index, but this was very much in line with the All Ordinaries Index. They rose appreciably sharper than the All Ordinaries Index, however, when the Managing Director made a presentation to the Securities Institute, but made no mention of the Index result.

Boral experienced a similar rise in its share price. The Boral AGM took place on 25 October 2002 and the Annual Financial Report had been released on 26 September 2002. There was a rise in share prices following both events. The chairman noted at the AGM, "At the time of the 2000 Annual General Meeting, Boral's share price was $1.94 (30 per cent below net tangible asset backing). At the time of last year's AGM, the share price had increased to $3.51, ... 36 per cent above NTA backing. Since the merger, Boral's share price has increased by 80 per cent. Over the same period, the ASX100 index has decreased by 4 per cent. ... the share price ... is now around $4.10". (23) There was no mention of the Index rating, although the Chairman praised the company's efforts in environmental management and occupational health and safety issues.

What of those who crashed in the Index rankings?

Telstra shares were steady following the release of the Index, although they fell a week or so later in line with the All Ordinaries. The probable cause of the fall was the announcement on 5 November 2002 by Moody's Investor Service of a change for the worse in the rating outlook for Telstra. This disappointing result was not relieved by the Board's report to the AGM on 15 November 2002, after which shares continued to fall. (24)

The Fosters Group's shares changed little at the time of the Index's release. The only large changes to the share price occurred in early September and early October, which were probably caused, as the Fosters Chairman explained in his AGM address on 28 October 2002 by two other factors. "The Dividend Reinvestment Plan, or DRP, was also amended in June 2002. At the AGM last year, shareholders were advised that we would remove the 5 per cent discount that applied to shares purchased under the DRP. This took effect from 5 September 2002." In October 2002, more than 76,000 Foster's shareholders elected to participate in the DRP and as a result 8.7 million ordinary shares were issued. (25)

The shareholders of the Telecom Corporation of New Zealand seemed similarly unaffected by the Index's release. Share prices fell slightly after 28 October, but they fell a great deal after the announcement on 4 November 2002 of a substantial change in shareholdings of the corporation. They had risen a similarly large amount in the months prior to the announcement of the buy-up. (26)

Goodman Fielder shares fell somewhat in the week prior to the Index's release. Interestingly, at the AGM on 8 November 2002, the Chairman remarked, "While I don't normally place too much store on surveys, it's interesting to note that in a recently completed study on corporate governance practices conducted by the University of Newcastle, Goodman Fielder ranked tenth out of 250 Australian companies." No mention of the Index.

In terms of the immediate impact of the Index on shareholder behaviour, it appeared to be ineffective.

CONCLUSIONS

The results of the analysis of the Good Reputation Index are clear and stark.

- The entire exercise was marred by the imposition of a political agenda not widely shared by the community.

- The agenda, if successful in changing corporate behaviour, is probably injurious to the contribution that corporations make to society through their commercial activities.

- Success in the rankings was determined by survey participation, not performance.

- The exercise had no apparent impact on the behaviour of the corporations. In that regard, it failed to achieve its objective.

- The disclosure of interests on the part of research groups was marred by reports that some had touted for business in helping corporations to fill out the questionnaire.

It is important to all those who have an interest in the success of corporations to have access to accurate information about them. The relevance of information will depend, however, on the relationship between the corporation and the enquirer. The investor will want to know about returns and good financial management. The worker will want to know about pay and conditions. The supplier will want to know about contract details and timeliness of payment. The consumer will want to know about products and services, their price, availability and quality, and guarantees sold with the product. The local community will want to know about the impact on their amenity. A myriad of government authorities will want to know about all of these things and more. Governments will establish rules from time to time that will apply to all corporations which will include requirements to disclose certain information. Beyond those requirements and the many that arise from contractual obligations and in the course of building relations with any groups a corporation chooses, there is little point to the Reputation Measurement exercise. No-one changed their behaviour, no-one much took any notice, but those corporations who did choose the method to enhance their competitive edge should ponder the climate of regulation they help encourage.

Reputation Measurement, the NGOs who pose as experts, and The Age and The Sydney Morning Herald who pose as keepers of the truth, should ponder what good they are doing in the exercise. Their agendas are flawed, their techniques are flawed, their answers are preposterous. They should give the game away.

ENDNOTES

1. Australian Conservation Foundation, 2002. "Corporate Australia: Stuck In-Reverse The Environmental Performance of Australia's Top 100 Companies 2002", 14. Accessed 17 February 2003.

2. See Johns, G. 2002. "Corporate Social Responsibility or Civil Society Regulation?" The Harold Clough Lecture, Perth, 19 August 2002.

3. Gardberg, N. and C. Fombrun, 2002. "The Global Reputation Quotient Project: Steps Towards a Cross-Nationally Valid Measure of Corporate Reputation." Corporate Reputation Review 4(4): 303.

4. Loc. cit.

5. As listed by BRW magazine, based on financial indicators.

6. http://www.reputationmeasurement.com.au/2002ReputationIndex.pdf. Accessed 28 January 2003.

7. It had the lowest average deviation across all performance categories.

8. It had one of the highest average deviations across all performance categories.

9. http://www.asx.com.au Accessed 11 February 2003.

10. It appears on every chart in this analysis.

11. http://www.asx.com.au Accessed 11 February 2003.

12. http://www.toll.com.au/index.asp Accessed 13 February 2003.

13. http://www.reputationmeasurement.com.au/2002ReputationIndex.pdf. (Emphasis added) Accessed 28 January 2003.

14. Weiss, A. 2002. "Cracks in the Foundation of Stakeholder Theory", 1. Accessed 27 August 2002.

15. Ibid., 6.

16. Corfield, A. 1998. "The Stakeholder Theory and its Future In Australian Corporate Governance: A Preliminary Analysis." Bond Law Review, 10: 218.

17. Parker, C. 2002. The Open Corporation: Effective Self-Regulation and Democracy. Melbourne: Cambridge University Press, 227. Emphasis added.

18. Ibid., 7.

19. Corfield, op. cit., 221.

20. Mitra, B. and R. Gupta, 2002. "Sustainable Development Versus Sustained Development." In R. Bailey ed. Global Warming and other Eco-Myths. Roseville, California: Forum ,134.

21. Australian Conservation Foundation, 2002. "Corporate Australia Stuck In-Reverse: The Environmental Performance of Australia's Top 100 Companies 2002", 11. Accessed 17 February 2003.

22. See Oxfam/CAA Accessed 17 February 2002.

23. http://www.asx.com.au Accessed 19 February 2003.

24. http://www.asx.com.au Accessed 12 February 2003.

25. http://www.asx.com.au Accessed 13 February 2003.

26. http://www.asx.com.au Accessed 19 February 2003.

No comments:

Post a Comment