Address to APEC Conference on Managing Climate Change --

Practicalities and Realities in a Post Kyoto Future

AUSTRALIAN EMISSION ABATEMENT MEASURES

Although having decided not to ratify Kyoto, Australian Governments have undertaken a range of measures that in effect accede to its obligations. Ministers are fond of saying that we will be only some three or four percentage points above our target of 8 per cent above 1990 levels during the 2008-12 reference period. This is, of course, pure propaganda and results from us having redefined forest clearing so that we obtain credits that previously were not envisaged. The real picture is that we are likely to be at some 25 per cent above the 1990 reference point.

This is in spite of some costly abatement schemes Australia already has in place both in the form of the taxes and command and control. These measures are:

- the Federal Government's Mandatory Renewable Energy Target (MRET),

- the Queensland's 13 per cent gas target,

- the NSW's Greenhouse Gas Abatement Certificate (NGAC) scheme and

- schemes that mandate minimum energy savings on appliances. First extended to fridges and freezers to save the world from the then voguish fear that the world was running out of energy, these regulatory requirements have been re-badged as greenhouse measures and extended. In Victoria, new home buyers have a choice of installing some very expensive and useless water tank system or solar heating, involving an upfront outlay of $2000. This is for an unreliable energy supply that, once its capital is amortised, is much more expensive even than wind power. Nobody has established reliable values for these rather multitudinous schemes, the cost of which are entirely hidden from the consumer.

The MRET scheme's focus is on renewable energy and requires retailers to acquire and annually surrender a progressively increased number of Renewable Energy Certificates (RECs). The major beneficiary was hydro in 2003, with Snowy having some 490,000 RECs, worth some $16 million to the business. Although accounting for only 10 per cent of the RECs created in 2003, wind is likely to increasingly account for the RECs growth.

The Queensland scheme seeks to substitute gas for coal based electricity inputs, while the NSW scheme seeks to introduce a penalty on CO2 graduated in line with the emissions per unit of energy of each electricity generation source.

The default penalty costs of the three regulatory measures provide a cap on the costs they are likely to entail. These costs entail a premium over the costs of conventional electricity to retailers. By 2010, when the schemes are at full maturity, the fall back penalty rates for the Commonwealth, NSW and Queensland schemes respectively are $40, $14.3 and $13.1 per MWh. These rates provide the (maximum) subsidies to the non-carbon or low-carbon emitting fuels.

The table below summarises the more readily identified costs.

2010 Costs of Greenhouse Gas Support Measures

| MRET | NGAC | Qld 13% Gas | Commonwealth subsidies | State Subsidies | |

| $M | 380 | 222 | 68 | 124 (2006/7) | 32 (2004/5) |

ABATEMENT AND MEASURES TAKEN IN OTHER COUNTRIES

Given the readiness of the international community to accept Australia's version of the truth about our massive reductions in business as usual greenhouse emissions, it is a fair bet that every other country is gilding its lilies and that the outcomes to date are not what they appear to be. All this further degrades the overall effect of the carbon reduction measures that most of the developed economies of the world have agreed to undertake. And you will recall, that even the measures agreed to in Kyoto have a theoretical affect of retarding the forecast warming trend by only six years.

Other countries have also employed a mix of taxes and regulatory requirements in pursuing emission reductions. The carbon trading system is therefore an overlay on top of other regulatory requirements and subsidies.

Even though countries may be exaggerating their achievements, very extensive costs have been incurred in many countries to defray carbon emissions. Denmark is the most publicised for its espousal of wind, which accounts for 15 per cent of its generating capacity. Denmark, largely as a result of the measures it has taken, has the most expensive electricity in the developed world -- three to four times the cost of Australia's.

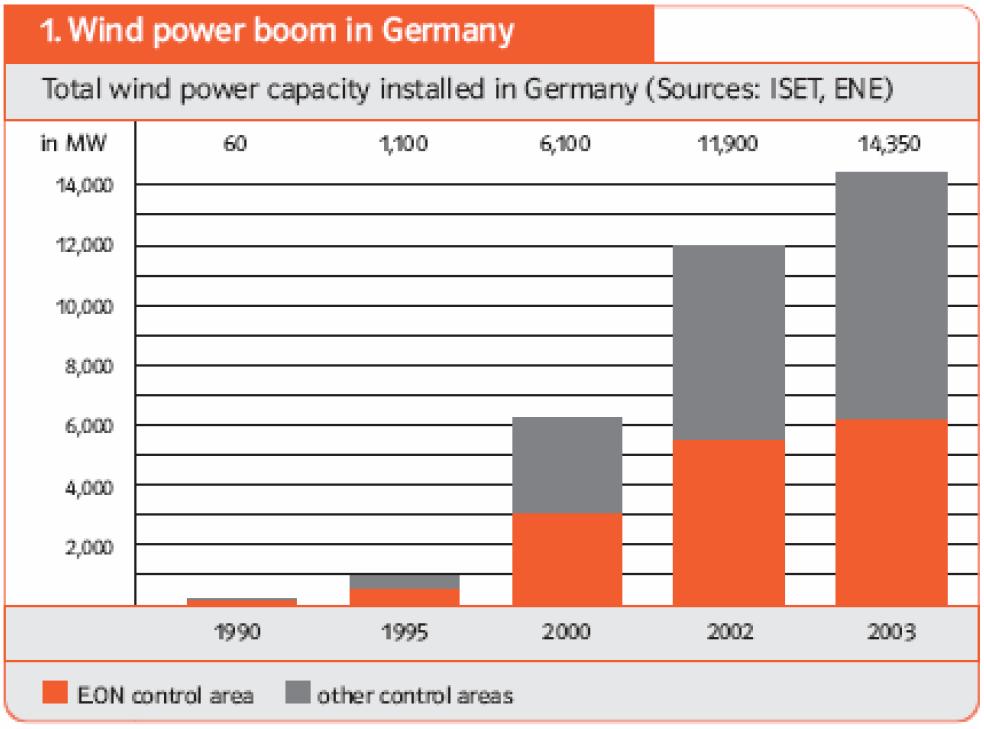

Germany has also made a major effort in installing wind power. The amount of wind power in Germany will be dramatically increased in the coming years through the statutory promotional measures of the Red-Green coalition. From around 23 terawatt-hours (in 2003), the amount of wind power electricity will rapidly increase to more than 77 terawatt-hours by the year 2015. This would represent more than 16 percent of the electricity consumption in Germany

In 2003, Germany's wind installations were rather more than the NSW total installed capacity. Wind actually can only provide an estimated 8 per cent of its capacity as firm even with a great many turbines. Hence e.on maintains the only saving in practice is the pure fuel costs.

CARBON TRADING

The European Union's Greenhouse Gas Emission Trading Scheme started operating in January 2005. It was preceded by a UK trading scheme operating from April 2002. The 25 EU member nations are given carbon-emissions quotas that are assigned among the EU's total of 12,000 power plants and heavy-industry factories. Each of these quotas is then reduced gradually in line with the EU's Kyoto commitment.

Overall this means cutting emissions to 8 percent below 1990 levels by 2012, though the variability is considerable. It ranges from 21 per cent reductions for plucky Denmark and green left Deutschland with its residue of Communist era plants through no change for France and Finland and a permitted increase of 25 per cent and 27 per cent for Greece and Portugal respectively. Companies unable to comply with these cuts must purchase "credits" from companies that have surpluses. And so the tradeable rights process has created a brand new currency and a re-alignment in wealth throughout those nations that have adopted it.

Our own experiences with schemes like MRET illustrate how difficult, once a constituency is formed, it is to abandon the regulatory arrangement. Pressure from the beneficiaries is placed on governments which augments the green left idealistic pressures that are always close to the surface. The Australian Government, having made the mistake of handing a 9,500 MWh per year windfall to the high cost suppliers, thinking that it was merely giving a token 2% additional energy to the exotic renewables is now saddled with about 5 per cent of total energy but has managed to stand firm at this level.

The chart shows where each of the EU countries stands in relation to the overall commitment. Thus Austria in 2002 was 7 per cent above its base year level and has a target to be 13 per cent below; Belgium was 3 per cent above and has a target of 7 per cent below; the UK, largely because it has replaced much of its coal generating capacity with gas, is well ahead of its target.

The following is the picture for the EU 15

| Base year (Mt C02e) | 2002 (Mt C02e) | Change base year to 2002 (Mt C02e) | BSA (%) | BSA target (Mt C02e) | Distance to BSA in 2002 (Mt C02e) | |

| Austria | 78 | 85 | 7 | -13.0% | 69.7 | 17.1 |

| Belgium | 146.8 | 150 | 3.2 | -7.5% | 135.8 | 14.2 |

| Denmark | 69 | 68 | -1 | -21.0% | 54.5 | 13.5 |

| Finland | 76.8 | 82 | 5.2 | -0.0% | 76.8 | 5.2 |

| France | 564.7 | 554 | -10.7 | 0.0% | 564.7 | -10.7 |

| Germany | 1253.3 | 1016 | -237.3 | -21.0% | 990.1 | 25.9 |

| Greece | 107 | 135 | 28 | 25.0% | 133.8 | 1.3 |

| Ireland | 53.4 | 69 | 15.6 | 13.0% | 60.3 | 8.7 |

| Italy | 508 | 554 | 46 | -6.5% | 475.0 | 79 |

| Luxembourg | 12.7 | 11 | -1.7 | -28.0% | 9.1 | 1.9 |

| Netherlands | 212.5 | 214 | 1.5 | -6.0% | 199.8 | 14.3 |

| Portugal | 57.9 | 82 | 24.1 | 27.0% | 73.5 | 8.5 |

| Spain | 286.8 | 400 | 113.2 | 15.0% | 329.8 | 70.2 |

| Sweden | 72.3 | 70 | -2.3 | 4.0% | 75.2 | -5.2 |

| UK | 746 | 635 | -111 | -12.5% | 652.8 | -17.8 |

| EU15 | 4245.5 | 4125 | -120 | -8% | 3905.6 | 219.4 |

Sources: Point Carbon and United Nations Framework Convention on Climate Change

EU Ministers are already discussing major further cuts for the post 2012 period. This is in spite of the EU as a whole showing a wide gulf between its 8 per cent reduction commitment and the existing level of about 3 per cent, a level presumably facilitated by the EU's slower than expected economic growth.

In this respect, the accession of Russia to the Kyoto Protocol was welcomed by other ratifiers, not only because it provided the quorum to bring the treaty into force but also because Russia has surplus credits which enable European countries to buy so that they can fulfil their obligations at (they hope) a relatively low cost. For its part Russia clearly hopes to screw a high price out of the Western Europeans and Japanese and Canadians.

But these financial flow speculations obscure the fact that their effect is to further reduce the real reductions in carbon dioxide since the Russians' actions, had they not ratified, would not be affected by shortage of emission rights in the pre-2012 period. Sales therefore represent windfall gain and losses but no real reduction in emission levels. In other words, there is a financial flow and an illusion that more is being done to reduce the emissions than is in fact the case.

TAXES VERSUS TRADEABLE RIGHTS

Assignment of tradable rights and a tax amount to a similar outcome. One establishes the quantity and allows the price to be determined as a result; the other sets the price which it estimates will bring about the desired quantitative effect. Taxes offer certainty about the price of the outcome, tradeable rights offer certainty about the quantity; conversely, taxes may markedly over or undershoot the target, while tradeable rights might prove to have highly uncertain values.

One shortcoming of a tradable rights scheme is that once in place, a property right is created and similar rights based on a scarcity determined by government have proven very difficult to remove. One thinks particularly of taxi plates, which constitute a negative effect on aggregate income but which once in place few jurisdictions have ever removed.

To be of value, the right must be clearly defined, rigorously policed and easily transferable. Rights to emit sulphur and other local emissions have shown the way in the USA. Handling these on an international scale is more difficult, though clearly not insuperable. Their value is a reflection of their scarcity and is diminished to the degree that the rights:

- can be cancelled

- become obsolete as a result of innovations

- become worthless because they are no longer needed e.g. the fear of warming disappears

- existing rights are swamped by newly created or discovered rights.

The importance is the scarcity. This could easily be reduced by having new rights created especially in developing countries and especially if those rights could be in the form of "planned projects that have been modified" so that reduced levels of emissions emanate.

In some respects, therefore a tax is preferable to a tradeable right though the incumbents would clearly favour the latter which would offer them some compensation for plants established before some de facto retrospective legislation reduced their value. In this respect, firms are probably living in a fool's paradise. A recent UK Parliamentary report slammed the likelihood that UK generators would make windfall profits in excess of £500 million from the trading scheme, labelling it unacceptable and ironic in view of the complaints from the power sector regarding the UK national allocation plan.

The advantage of a credible tradeable rights approach is that it recruits the users into discovering the most cost-effective means of achieving the target. Thus, it leaves the various parties to decide whether to change input source, reduce output or arrange to have new forest plantations or other means of meeting the target.

One thing is clear: there can be no target meeting by voluntary means. Indeed the aforementioned UK Parliamentary Committee report said, "In the final analysis emissions trading will only work if it results in an increase in the price of energy for industry, business and even domestic consumers. Only then will the necessary incentives to prompt behavioural change and investment in low carbon technologies arise". Ominously, the report also urged the British government to demand strict targets for developing countries to curb emissions when discussing post-Kyoto targets clearly a forerunner of using trade as a Kyoto policy weapon.

The voluntary take up of green energy is quite small. There are claims that one of the Japanese utilities has taken an option on some forestry reserves in NSW but this placed a very low value on the greenhouse component itself in return for the presumed PR benefit.

There is also some evidence of firms and individuals voluntarily agreeing to pay a premium for green energy over and above that which is non-transparently foisted on them by government in the form of MRET, NGAC, 13 per cent gas and energy efficiency standards on appliances and houses.

The annual Green Power sales (above MRET requirements) are 424 GWh/annum. This is an additional 24% on mandatory requirements and represents over 103,000 customers including 6,000 commercial customers.

From 2006 Switzerland will introduce a CO2 tax on fossil fuels of (euro 22.6/t). It is also introducing a so-called voluntary Climate Penny scheme intended to raise 70 Millions Swiss Francs (euro 45m) but if this is not achieved by the end of 2007, a CO2 tax will be introduced for transport fuels as well. The money will be spent on domestic measures, such as the promotion of bio fuels, but the biggest share of it is planned be spent on emission reduction projects abroad.

AFFECT OF CURRENT CARBON PRICES ON AUSTRALIAN

ELECTRICITY GENERATION INDUSTRY

If carbon taxes or tradeable rights become a permanent feature of the electricity supply cost structure, the cost structures of the different fuels is going to change markedly. Those with virtually no carbon per energy output (wind, hydro, nuclear) will be favoured over those with relatively little carbon (gas) and high carbon (coal).

The chart encapsulated the different emission factors for the coal and gas plants and sets their costs at the present level of carbon trades (i.e. about Euro 14 per tonne of CO2).

At that level nuclear in Australia would ostensibly be the most viable source of future energy. For Australia however, nuclear might face more than the usual number of rent-a-crowd activists which would add considerably to the cost, including through delays.

Excluding taxes, nuclear is clearly uneconomic in Australia, especially compared to the low cost coal along the eastern seaboard. In terms of dollars per MWh coal comes in at between the low $30s and $40. Nuclear would probably be in the high $40s. In addition, there is the inflexibility of nuclear -- just as the inflexibility of coal fired stations reduces their value somewhat against combined cycle gas plants, the lesser flexibility of nuclear would call for a significant, though lesser discount against coal power.

These cost augmentations mean a dramatic change in the power industry worldwide and a shift to nuclear. Nobody seriously considers the renewables, mainly wind, can play a major enduring role. Wind is flattered on the chart because its intermittent nature is not factored in. That nature means that reserve power must be made available as an ancillary service and the transmission system, once wind assumes more than a trivial role must be upgraded. Indeed, the only reason Denmark can operate with such a high wind share is that it is part of the Nord grid and the wider German grid and its energy volatility is compensated by Norwegian fast start hydro in particular.

Mr Blair's various utterances are clearly preparing the ground for a momentous change by the political left on the nuclear issue. In Australia Mr Carr has pointedly said that in his various statements that nuclear would be very difficult but is also raising the issue. Contrary to the hype, it is safe, clean and extremely reliable.

The outcome of moving to nuclear would be mixed, depending on the country concerned.

In Japan, and most European countries, nuclear represents the lowest cost option. For Australia, the punitive taxation of coal (and later gas) from greenhouse mitigation measures would means a vast loss of wealth and a rearrangement of industries. Brown coal and progressive slivers of black coal would be rendered valueless. This amounts to tens of billions of dollars of natural wealth. Moreover, the economy is heavily centred on the energy intensive industries -- not only the industries themselves but the tertiary sector infrastructure that advises accounts, markets and otherwise services them. The serious drop in living standards that would stem from their abandonment is difficult to model

THE VALUE OF GLOBAL CARBON TRADING

The value of carbon trading can therefore be considered in two ways. The first is how much are the trades as units and in aggregate likely to be worth. Well the present level of transactions is running at about euros 10 million per day. But if the rather modest reductions from business-as-usual that are presently in place are bringing a price of $22 per tonne of carbon dioxide, once the more serious post 2012 reductions have been agreed and implemented, we must be talking about a level rising up to the hundred dollar plus mark -- implying a threefold increase in the generated price of electricity.

Whether this amounts to real worth, the second means of considering value, depends on your belief systems about the reality, extent and effect of global warming.

Higher priced energy will clearly reduce its usage. But with options to have the same goods produced in countries which have no major obligations to impose the tax effect of the Annex I parties there will clearly be a deal of substitution.

Indeed, it is possible that the net effect could be an increase in emissions for two reasons. First the power plants in the western world are more efficient than is generally the case in countries with no obligations to reduce their emissions. This may change but the initial effect of shifting energy intensive industries to China and India would be a greater use of energy per unit of output.

Secondly, a forced relocation of industries is also likely to mean a greater degree of transport per se. This is in two forms: first a reduction in processing for local needs will mean an export and subsequent import where at present there is neither. In addition there will be a relocation of processing to tax-immune jurisdictions -- to put it most simply, bauxite will replace alumina as the transported product and alumina will replace aluminium. This extra transport will itself increase the amount of energy used.

No comments:

Post a Comment