Backgrounder

EXECUTIVE SUMMARY

The Commonwealth Government expects to spend up to $6 Billion on public research this fiscal year. It is not unreasonable to investigate the return the community will earn on that massive expenditure. Indeed, in March of this year, the Productivity Commission was commissioned to investigate this very point. David Murray, Future Fund Chairman, has argued that no observable link exists between publicly funded research and productivity growth and economic gain. Yet, he has called for a boost in publicly funded research. Economists also argue for increased public funding of research. They imagine massive market failure in research and development. Indeed, standard economic theory predicts that the private sector would undertake no research at all. One is reminded of the old economic saw, "That's all very well in practice, but could never happen in theory". Just because economists can imagine a theoretical market failure that does not imply that real markets actually fail.

This paper investigates the basic economic argument for public investment in research and development. The Allen Consulting Group has argued the return to public research could be as high as 50 percent. If this were true, the government should invest our entire GDP in public research. Of course, it isn't true; the returns to public research are lower, much lower, than generally argued. Due to the deadweight costs of taxation, the costs of public research are much higher than generally believed. In all likelihood, public expenditure on research would crowd-out private expenditure. Using the work of three Nobel Prize winning economists, I show the standard economic analysis supporting public expenditure on research is fundamentally and methodologically flawed.

Each of the stepping-stones in the case for publicly funded science is flawed:

- R&D is not a public good.

- The cost of public funds is not lower than the cost of private funds.

- The returns to public science are low.

- Governments have a poor track record of picking "winners".

- Publicly funded R&D has a negative impact on economic growth.

- Economists are unable to explain how spillovers occur, or how valuable these spillovers are.

The notion that throwing an infinite amount of money at public research will somehow, at some time, automatically lead to some benefit is a myth. The government spends a substantial amount on public science and innovation. It is not clear that any substantial benefit is derived from that expenditure.

INTRODUCTION (1)

James M Buchanan has posed the question, "What goods and services should a community supply publicly through political-government processes rather than privately through market processes?" (2) The Australian government provides many goods and services to the community -- it expends up to 31 per cent of GDP. This paper investigates whether government should fund science. Funding in this sense could be direct, or indirect (using subsidy). An apparently strong economic argument exists to support the public funding of science. Science, the argument goes, has public good characteristics and would be under-provided by the market. Anyone can use knowledge, once created; consequently the producers of science cannot earn a return for their efforts and would do less science than is socially optimal. Economists generally agree: market failure exists and government can easily correct that failure and increase the amount of science. Because economists can imagine a theoretical market failure that does not imply that real markets actually fail.

On close inspection the economic argument for public science is not strong. The standard analysis rests on a series of unexamined assumptions. Each of these assumptions will be considered and each shown to be defective. First, this paper shall discuss the notion that science is a "public good". Second, we discuss the question of when government should finance science, or any other activity for that matter. Third, the paper examines the standard "spillover" argument used to justify government funding of science. In each instance we shall see that the arguments for government funding are either over-sold, or simply false. In many instances effective government funding of science would require the government to have information or foresight that others do not, and cannot have. Therefore, the government should do less rather than more.

INSTITUTIONAL BACKGROUND

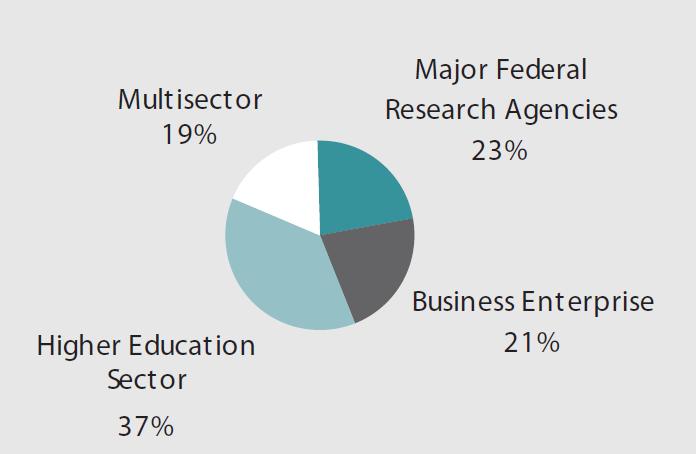

The Commonwealth expects to spend 2.78 per cent of its budget on science and innovation in 2006-07. This constitutes nearly six billion dollars. Figure 1 shows the relative allocation of funds for 2006-07. Approximately, $2.2 billion will be expended on the higher education sector, while $1.4 billion will be spent on the CSIRO, defence, and other federal R&D agencies.

Figure 1: Commonwealth Expenditure on Science and Innovation 2006-2007 Source: Adapted from Budget Papers

Source: Adapted from Budget Papers

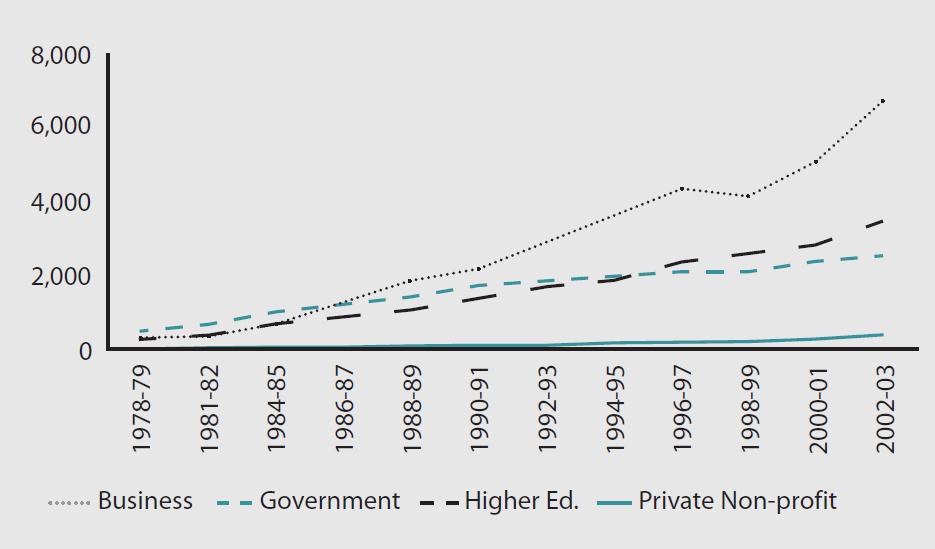

Public expenditure on R&D constitutes almost half of Australian gross expenditure on R&D. Figure 2 shows a time series of R&D expenditure since the late 1970s. Private R&D has grown substantially since that time, from less than what the government spends to double that amount. This is not entirely due to R&D tax concessions introduced in the mid-1980s. The Productivity Commission has investigated the growth in private R&D and argues that the acceleration in business R&D preceded the introduction of tax concessions by two years. (3)

Figure 2: Gross domestic expenditure on R&D ($millions) Source: Adapted from Australian Science and Technology at a glance 2005, pg. 17.

Source: Adapted from Australian Science and Technology at a glance 2005, pg. 17.

The question, of course, is to what extent this money is well spent? Should government be spending anything on R&D? What basis is there to believe that public money should be expended on R&D?

RESEARCH AND DEVELOPMENT AS A PUBLIC GOOD

In a famous 1962 paper, Kenneth Arrow argues that markets will fail in the face of three factors; indivisibility, inappropriability, and uncertainty. (4) He then argues that "invention", which he defines as the "production of knowledge", suffers from all three conditions, and therefore the market will underinvest in basic R&D. (5) The first point to note is that Arrow is very specific: the market will underinvest in basic R&D, not all R&D. The second issue relates to what exactly constitutes an "underinvestment"? This question is quite important. How much more should be invested in R&D? In this regard Richard Romano (6) is worth quoting in full: "In the frictionless perfectly competitive market, with no barriers to the use of information, the market will provide no R&D investment" (emphasis added). The third point, of course, is to ask whether Arrow is correct in his classification of R&D? We defer discussion of the second point.

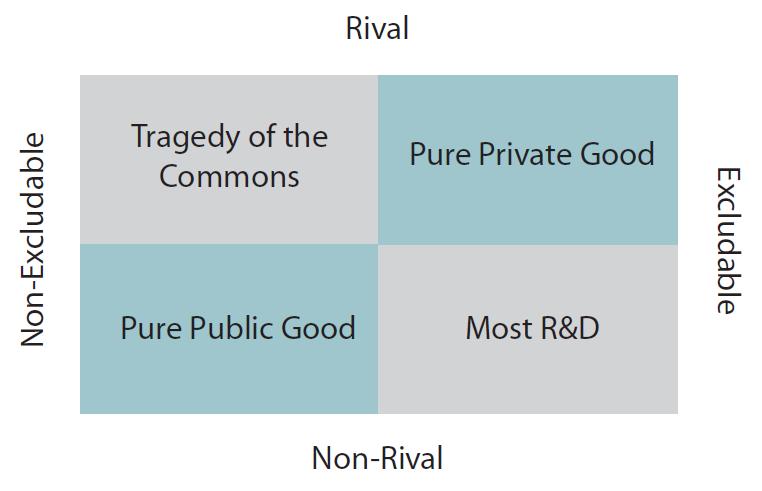

Goods and services with Arrow's characteristics are usually described as "public goods". Public goods have two characteristics: they are non-excludable (indivisible) and non-rival (inappropriable). (7) Geoffrey Brennan argues these two properties are independent of each other. (8) Excludability relates to the ability of person x preventing person y from consuming a good or service. Rivalry relates to person x's consumption reducing person y's ability to consume the same good or service. These two characteristics are plotted in the figure below. Whether a product is rival or non-rival is largely a function of the characteristics of the product and, to a lessor extent, technology. Excludability will depend on property rights, and technology.

Each of the four quadrants in the figure shows different combinations of rivalry and excludability. Pure public goods are both non-rival and non-excludable, while pure private goods are rival and excludable. The tragedy of the commons occurs when goods are rival but non-excludable. This paper shall argue R&D is excludable, but not rival.

Many discussions about R&D activity implicitly assume that R&D is a pure public good, or that the tragedy of the commons prevails. The tragedy of the commons is often described as an "open-access" property rights regime. In this type of arrangement anyone can use a resource, but cannot exclude anyone else using the same resource. Examples of the tragedy of the commons include fishing grounds in international waters and traffic congestion. The argument goes that private firms would not undertake R&D simply because their competitors would immediately copy the output and the originator of the R&D would not earn a return. This argument, however, is not about rivalry, but about excludability. The tragedy of the commons "reflects the unwillingness or inability of the government, society, or current users to introduce and enforce an effective system of control" over access to resources. (9) There is no serious suggestion that R&D activity constitutes a tragedy of the commons. Property rights to intellectual capital exist and are enforced by the courts. For intellectual property there is no tragedy of the commons. (10) Indeed R&D may well have exactly the opposite problem.

Intellectual property, as defined by economists, is not scarce. While creative ability is scarce, intellectual property once created is not scarce. Sir Arnold Plant argues that intellectual property rights (such as copyright and patents) are a "deliberate creation" of statute in order to create scarcity as opposed to alleviate the consequences of scarcity. (11) Without property rights in their creations, creators would be unable to profit from their activity. By providing a monopoly right to their creative endeavour, the legislature provides an incentive for creative activity. Economists tend to be hostile towards monopolies. In the case of intellectual property, however, this situation is said to be desirable as the creation of scarcity (restriction of supply) allows the creator to earn a profit from their creation. John Stuart Mill is clear on this point: "The condemnation of monopolies ought not to extend to patents, by which the originator of an improved process is allowed to enjoy, for a limited period, the exclusive privilege of using his own improvement. This is not making the commodity dear for his benefit, but merely postponing a part of the increased cheapness which the public owe to the inventor, in order to compensate and reward him for the service". (12) Mill, however, also concedes, "that the present Patent Laws need much improvement". (13) One hundred and fifty years later, that comment remains apposite.

Monopoly always causes economic distortion, and patents and copyright are no different. In recent years the demand for intellectual property right protection has increased quite dramatically. Adam Jaffe and Josh Lerner, for example, have written how legislative changes in the US lead "to an alarming growth in legal wrangling over patents. ... [T]he patent system -- intended to foster and protect innovation -- is generating waste and uncertainty that hinders and threatens the innovative process". (14) Following the adoption of the free trade agreement with the US, copyright protection in Australia has increased substantially in line with that in the US and EU, from the life of the author plus 50 years, to the life of the author plus 70 years. (15)

In summary, R&D is non-rival (i.e. it is not a pure private good, nor does the tragedy of the commons occur), but can be excludable. (16) The legal system operates well in this regard -- indeed, the argument is that the legal system is "over-excluding" at present. That may well be the case. For my purposes, however, the argument is simple; most R&D activity does not fall into the definition of being a pure public good. While I do not deny that pure public goods exist, I do believe them to be rare. In other words, the case of R&D is not a good fit to the theoretical literature on market failure. Keith Pavitt argues that the "publicness" of R&D is a mistaken application of theory, and displays an ignorance of empirical evidence. He states, "Risk aversion, low or zero marginal cost of application, and the difficulties in appropriating benefits have become standard explanations for the public subsidy of science. ... Over time progressively fewer references have been made to the empirical evidence, and more to the standard theorems of welfare economics. Whilst it might be advantageous in the economics classroom to assume that basic science is instantly applicable and easily transferable, ... such assumptions are empirically invalid, and have effectively restricted debate." (17)

WHEN SHOULD GOVERNMENT FUND ACTIVITY?

In this section, I will set out the principles as to when the government should fund any activity and will use R&D as an application.

Adam Smith set out the type of activity the government should fund as follows: "... though they may be in the highest degree advantageous to a great society, [they] are, however, of such a nature, that the profit could never repay the expense to any individual or small number of individuals". (18) It is easy to misinterpret this quote. Smith is not saying government should fund any and every loss-making project in society. Publicly funded activities must be "advantageous to a great society", yet be unprofitable to the private sector. The second criterion has already been discussed -- the project must have public good characteristics. In this section, I discuss Smith's first criteria -- the notion that the activity is "advantageous to a great society".

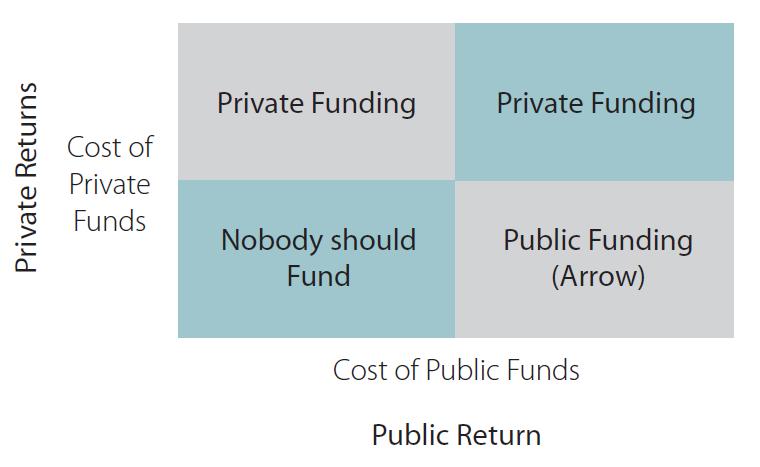

The figure below sets out private and public returns, and also shows the costs of private and public funds. (19) Any private project with an expected return greater than the cost of private funds will be undertaken and financed by the private sector. Similarly, any public project with an expected return greater than the cost of public funds will be undertaken and financed by the public sector. Those projects with expected returns less than the private cost of funds and less than the public cost of funds should not be funded. In order for the public sector to finance a particular project, two conditions must be met. First, the project must provide a public good, and second; the project must provide a return greater than the cost of public funds.

Source: Adapted from Kenneth M. Brown (1998, pg. 45)

Source: Adapted from Kenneth M. Brown (1998, pg. 45)

In principle, this may appear to be uncontroversial. Three very important questions arise. To what extent is R&D a public good? I have already suggested that most R&D is unlikely to have pure public good characteristics. What is the cost of public funds? (20) What is the return to publicly funded research?

The Cost of Public Funds. There are, at least, two components to the cost of public funds. First, we must consider the cost of those funds if the project were undertaken by the private sector. Second, we must consider the "deadweight cost" of taxation. In other words, the cost of public funds is equal to the cost of private funds (for a project of similar risk and duration) plus the deadweight cost of taxation. The notion that government funding is "cheaper" than private sector funding is simply wrong. (21) Well-known techniques can be employed to establish the cost of private funds -- indeed, second-year undergraduates are taught these techniques. To establish the costs of public funds, we need to gross-up the private costs for any given public project by the deadweight cost of taxation. Alex Robson surveys the literature on the estimated deadweight costs of taxation. (22) Estimates in the US for the deadweight loss on personal income tax are as high as 200 per cent. Similar estimates for Australia are in the order of 19 to 65 per cent. That means that the public cost of finance is equal to the private cost grossed up by a factor of between 1.19 and 1.65. For example, if the private cost for a particular project were 20 per cent, the public cost would be between 23.8 per cent and 33 per cent.

The Returns to Public Research. In 2003, The Allen Consulting Group undertook an analysis of Australian Research Council funded research. (23) As part of that report, the Allen Consulting Group estimate the return to public science in Australia is 25 per cent, while the return to ARC funded return could be between 39 and 50 per cent. This return is not particularly high -- especially considering that the deadweight cost of taxation may be quite large and the private cost of capital for R&D may be very high. In order to demonstrate the fragility of estimates of the returns to public R&D, I discuss the Allen Report estimates in some detail. (24)

The Allen Report uses two techniques in estimating the ARC return these being a "top-down" approach, and a "bottom-up" approach. The top-down approach results in an estimate of 50 per cent, while the bottom-up approach results in an estimate of 39 per cent. The calculation of these returns are extremely generous, and worthy of some discussion.

The top-down result is based on the following logic: R&D contributes to increases in productivity, which in turn contributes to economic growth. R&D contributed to half of the increase in productivity (which in turn contributed to 40 per cent of economic growth over the nineties). The R&D contribution can be broken up into a foreign, private, and public component. Public R&D makes up 25 per cent of the total R&D contribution, and consequently accounts for 12.5 per cent of the increase in productivity. This implies a social return of about 25 per cent to publicly funded R&D. The Allen Report then assumes ARC funded research to be twice as productive as all other public R&D, increasing the ARC return to 50 per cent. (25) The rationale for doubling the ARC return over the overall public return is highly questionable. The Allen Report indicates that citation studies show higher citations to ARC funded researchers than non-ARC funded research. There is, however, a selection bias in this argument. Academic track record is a highly weighted component (40 per cent -- the single largest component of the selection criteria) of the ARC selection process -- by definition, highly cited academics are more likely to receive funding. In a footnote, we see the following argument: "investigator initiated research such as that funded by the ARC may not be orientated towards generating outcomes ... [but] it must be noted that it is the quality of research, rather that its explicit orientation, that is the key predictor of eventual value and that the ARC produces higher than average outcomes in terms of research quality measures." (26)

The Allen Report, however, provides no evidence to support this claim. This is a common argument, and may well be true. Yet there are, at least, two considerations that mitigate against this view. First, Gordon Tullock demolishes the notion that "pure science is somehow superior to applied science. This feeling, paradoxically, is usually justified by claiming that the long-run results of pure research are apt to be of practical value. ... In fact, the general argument rests on something like an optical illusion". (27) In modern terms, Tullock identifies look-back bias and survivor bias as the sources of the "optical illusion" that pure science is superior to applied science. In other words, we take an existing product and trace its antecedents. Unsurprisingly, modern products are based on a large number of historical discoveries. What we do not know, however, is what proportion of historical discoveries is in use today. (28) It may well be the case that most historical knowledge is in use, however, it is equally likely that little of the historical record is being used.

A second assumption that requires examination is the notion that all R&D drives economic growth. This is a generally accepted approximation. The Allen Report relies on "OECD research" in their analysis. (29) In 2003, the OECD published an official report into "The Sources of Economic Growth in OECD Countries". (30) As part of that analysis the OECD investigates the impact of R&D on economic growth. (31) Specifically, they disaggregate R&D into a private and public component. As expected there is a positive and statistically significant relationship between overall R&D and economic growth, and also between private R&D and economic growth. (32) In contrast to the usual assumption, and in particular the Allen Report argument, there is a statistically significant negative relationship between public R&D and economic growth. The OECD report expresses some surprise at this result, suggesting that more sophisticated estimation techniques or more complicated analysis may reverse the unfavourable result for public R&D. Indeed, that may be the case; conversely until that analysis is actually performed we cannot know what the outcome will be. As the OECD concede, "at face value [the results] suggest publicly-performed R&D crowds out resources that could be alternatively used by the private sector, including private R&D. There is some evidence of this effect in studies that have looked in detail at the role of different forms of R&D and the interaction between them". In contrast to the Allen Report's view that public R&D has a social return of 25 per cent, with the ARC in particular having a 50 per cent return, the OECD reports that publicly funded R&D has a negative return.

The Allen Report also has a "bottom-up" calculation for the benefits of public R&D and the ARC. What they do here is identify the channels whereby publicly funded R&D can positively impact the economy and society at large. The following table sets out a summary of these channels and the "measured" benefits. (33)

| Category of Benefits | Measured Benefits |

| Building the basic knowledge stock | 10.0% |

| Generation of commercialisable intellectual property | 3.0% |

| Improving the skills base | 12.5% |

| Improved access to international research | 7.5% |

| Better informed policy making | 6.0% |

| Health, environmental and cultural benefit | Not Measured |

Source: Adapted from The Allen Consulting Group (2003, pg. 6)

The Allen Report simply adds all these benefits to arrive at a "measured benefit" of 39 per cent. The first caveat they introduce is that these benefits may accrue over time, in particular 4 to 10 years. Thirty-nine per cent return over four years is not impressive (8.58 per cent pa), a similar return over ten years even less impressive (3.34 per cent pa). Even at face value, a 39 per cent return over 4 to 10 years is unimpressive -- especially when compared to 50 per cent (presumably per annum) in the top-down analysis. (34) Bear in mind, the Allen Report indicated that ARC funded research is likely to be more valuable than other publicly funded research.

As already argued, the return for building the stock of basic knowledge is usually over-stated. In other words, the 10 per cent return may not be conservative at all. The Allen Report looks to the link between patents and science to show the value of building the stock of basic knowledge. In my view, this really demonstrates the generation of commercialisable intellectual knowledge -- the next channel they investigate. The Allen Report relies on a 2000 consulting report, commissioned by the ARC and CSIRO, and performed by CHI Research, Inc. (35) This report shows that Australian patents (issued in the US) rely heavily on Australian generated basic knowledge with 95 per cent of the cited papers written by individuals employed at public institutions. Seventy-four per cent of the papers that acknowledge financial support were supported by public agencies. (36) Figures such as these seem to indicate that Australians are making huge, and highly valued, contributions to basic knowledge. The CHI report, however, provides additional information, "Australian patents heavily cite Australian scientific research, the world's patents do not". (37) Australian patents over-cite Australian basic knowledge by a factor of ten, while the rest of the world's patents under-cite Australian basic knowledge by half. In other words, either Australian patent holders are very parochial, or basic knowledge in Australia is Australian specific. Overall, however, the ten per cent return to this channel appears generous.

By only "measuring" a three per cent return to commercialisable intellectual property, The Allen Report admits the ARC does not perform well in this area. Bear in mind, however, that the evidence for the generation of basic knowledge and commercialisable intellectual property is almost identical. The Allen Report in this instance has specific information about successful organisations (although they do not deduct the lost value of unsuccessful organisations) and the inputs the ARC have made. Yet the return from all this success is only 3 per cent. Consider, in that area where specific valuation data exist, the return to public science is shown to be low, but where specific valuation data do not exist, or are vague, the returns are large.

Improving the skill base has the single largest return of 12.5 per cent to the ARC and publicly funded science. To be fair, improving the skills base is likely to be a valuable function -- yet it is not clear whether the argument supports public funded science, publicly funded universities, or publicly funded students. The Australian Bureau of Statistics' Innovation in Australian Business report shows that employing a new graduate is the single largest technique innovating firms use when acquiring knowledge from an Australian university. (38) Yet, again, the 12.5 per cent is likely to be generous. The Allen Report estimates the wage premium to post-graduate studies, and adjusts for the ARC contribution to those studies. Yet, they do not adjust for the difference in premiums to PhD and Masters degrees, or for the difference in premiums in business and science graduates. Nor do they consider the "actual employment history of students", or the potential career paths students may follow. All up, the 12.5 per cent return is likely to be overestimated.

Improved access to international research may well be very important. One of the OECD working papers cited by the Allen Report estimated the impact of foreign R&D to be very high relative to domestic R&D. Australia is a small open economy, and access to international R&D would be very important. But, again, it is not clear whether this is an argument for public funding of science, or public funding for universities, or public funding for students. Indeed, it is not clear that this constitutes an argument for public funding at all. The Allen Report states, "The 'free-rider' strategy is simply not viable in the long term", but does not amplify on this comment. (39) By definition, Australia will always be a "free-rider" on foreign technology and science. On the other hand, Australian patent application over-cite Australian research, in that sense then Australia is not free-riding -- although despite this, the CHI Report indicated Australian performance to be "fair to middling". (40) The Allen Report "measures" a return to international access at 7.5 per cent. This is based on an ARC self-reported multiplier effect of 2.5. A multiplier of this magnitude is huge, so again the 7.5 per cent return is likely to be overstated.

Finally, the Allen Report "measures" a six per cent return to improved policy decision-making. The ARC has funded economic research that has fed into, and potentially improved, political decision making. Perhaps. The Allen Report identifies a number of projects that may well have improved political decision-making, yet even if these projects did yield a 6 per cent return, what of those projects that yielded nothing? Similarly, should we deduct the negative returns from political decision making that have not followed the advice given by the ARC funded research?

Overall, the Allen Report's bottom-up analysis of the returns to ARC funded research is overstated at best, and just wrong at worst. The returns are "guesstimates" and based on conjecture and speculation. In fairness to the Allen Report, many of the arguments they make are part of the mythology that surrounds public research, yet the estimated returns are hugely overstated. It is worth repeating, in that area where the data are hard, the estimated return to commercialisable intellectual property is low. In any event, 39 per cent over 4 to 10 years is not particularly high. Furthermore, the top-down approach is wishful thinking at best, and contradicted by OECD research showing the contribution of publicly funded research to economic growth to be negative. A return of 50 per cent to ARC funded research is not plausible, neither is the notion of a 25 per cent return to all publicly funded research.

Can government pick winners? It is difficult for the private sector to pick winners, let alone the public sector. Edwin Mansfield and others investigated 220 R&D projects in the late 1960s. (41) Forty per cent of these projects were technically incomplete. Of the remaining projects, 45 per cent were never commercialised. Of those that were commercialised, 60 per cent did not earn a positive economic return. In other words, only 13 per cent of R&D projects (in the sample) resulted in a profitable product. In a later study Mansfield and others report the probability of commercial success to be 27 per cent. (42) In a more recent study, Thomas Astebro examined a sample of 1,091 Canadian inventions. (43) Of these inventions, 75 were commercialised and reached the market. The average return was 11.4 per cent, however, the median return was negative seven per cent. In other words, a small proportion of inventions (six) had extremely high returns, while most had low or negative returns. It is difficult to believe that the public sector would be any better in picking winners -- indeed it would be likely that the public sector would be worse.

The ability of the public sector to choose winners relative to the private sector is investigated in a recent paper by Arthur M Diamond Jr. (44) He investigates citations to chemistry papers published in Science in 1985. Presumably enough time has elapsed for the "true worth" of these papers to be established and those that have more citations are likely to be more valuable than those with fewer citations. He pays particular attention to the source of research funding for these papers. His empirical analysis shows that research funded by private donors is more important than that funded by government. Diamond states, "the most straightforward interpretation is that private funders are more successful than the government at identifying important research". (45) The conclusion that we can draw from this research is that it is difficult for anyone to "pick winners", but the private sector is relatively better at doing so than the public sector.

How Much Public Funded Research Should There Be? In this section, I have made two arguments. First, the cost of public funds is higher than many people (including economists) think. The public cost of research funds is equal to the cost of private funds, grossed up by the cost of raising those funds. A lot of public funding is aimed at very risky projects (the Allen Report, for example, states "the ARC tends to fund high-potential research at the early, riskiest stages of the innovation process" (46)), implying that the cost of private equity would be reasonably high. The second argument is that the returns to public science are a lot lower than many people (especially economists) think. In conclusion, many public research projects are likely to be in the "Nobody should fund" quadrant, and fewer projects are likely to be in the "Public Funding" quadrant. There may well be projects that should be publicly funded; however, the burden of proof needs to be greater than at present. Currently, it seems that the only criteria for public funding is that the private sector will not fund the project. Two criteria need be meet for public funding of R&D. First, the project must produce a public good that is both non-rival and non-excludable, and the return must exceed the cost of public funds.

It is important, however, to remember that government may be a consumer of research. The discussion has to a large extent looked at the situation where government funds research for the sake of research. Government may also fund research for the sake of making better public policy decisions. For example, government may have a legitimate interest in understanding the impact of water usage patterns on the environment. In this situation, the government could put a research project out to tender just as any other consumer of research would do. There is, however, a huge difference between government funding research to answer questions it would like answered, and government providing funding for research on the basis that research is under-provided by the market.

SPILLOVER AND MARKET FAILURE: THE STANDARD ECONOMIC ANALYSIS

The standard economic argument for government subsidy is the existence of positive externality, or spillovers. This notion is the appropriability concept discussed earlier. The benefits of R&D are appropriable, but are not entirely appropriable. To the extent that an innovator cannot appropriate 100 per cent of his invention, the argument goes, there will be an underinvestment in R&D. (47) The "solution" to this underinvestment is a government subsidy, or tax concession.

In the standard economic analysis, an innovator sets the R&D benefit equal to the R&D cost and makes the appropriate investment. The complication comes in when we consider that "spillovers" drive a wedge between the total R&D benefit and the benefit he can appropriate. This wedge can be called the spillover ratio. This ratio reduces the profitability of the investment and so the innovator invests less. (48) Government intervention can increase the profitability of R&D by creating temporary monopoly, or by reducing costs, and so increase R&D investment back to its "optimal level". This standard economic analysis can be found in many first or second year economics texts. William Baumol has estimated the size of the spillover gap to be as high as 80 per cent -- he suggests this figure may be "a very conservative figure". (49) Charles Jones and John Williams calibrate a theoretical growth model and estimate underinvestment to be two to four times current R&D investment. (50) This latter figure implies US gross domestic expenditure on R&D should increase from (about) $291 billion to $1.167 trillion. (51) Similarly Australian gross expenditure would increase from (about) $13 billion to $52 billion. Of course, a suggested increase of this magnitude leads to the question as to whether those funds can be feasibly reallocated from their current usage to R&D projects?

There are, however, conceptual problems associated with the standard economic analysis. Some of these conceptual problems relate to the degree of abstraction in the analysis while other problems are more methodological. The abstraction problems relate to the type of firms under discussion and the institutional environment they operate in. Furthermore, the analysis is silent of the type of investment being undertaken. For example, are the firms under discussion operating under conditions of perfect competition, or do they have some degree of market power? If firms do have market power then there may be an over-investment in R&D. (52) In any event, what type of investment are we talking about? Most R&D projects end in commercial failure. Should we include or exclude investments that fail? The implicit assumption that many economists seem to make is that all R&D activity is valuable even if it is not profitable. As I argued above, this proposition is only true under limited conditions.

The first set of methodological problems relate to the notion of social benefits, and the second set relate to the costs of R&D and the choices made by innovators. The standard economic analysis begins by assuming the innovator knows the total R&D benefit and then deducts that portion that will spillover and cannot be appropriated. Similarly, the government can simply add back the spillover and estimate the totality of the R&D benefit. This notion, however, runs foul of the uncertainty associated with R&D. Arrow wrote that uncertainty is one of the factors that lead markets to fail. While uncertainty does not imply that decisions cannot be made, it does suggest that ex ante it is difficult to specify the benefits of R&D to a particular product let alone society at large. As Richard Nelson indicated, "External economies result from [the fact] that research results often are of little value to the firm that sponsors the research, though of great value to another firm ..." (53) Yet, we are invited to believe the innovator is able to correctly identify all the benefits from R&D. As Gordon Tullock has indicated, "Any decision on how much should be invested ... necessarily depends on a guess as to what now-unknown information will be discovered by the investigation. Such guesses are hard to make, and we certainly do not put much dependence on them". (54) In describing the benefits to R&D, both private and public, we encounter Hayek's information problem, "how to secure the best use of resources known to any of the members of society, for ends whose relative importance only these individuals know". (55) As argued earlier, it is possible to establish the benefits of R&D after the fact, but this type of analysis relies on look-back bias and data snooping. It is difficult for an innovator to estimate their own return to R&D in advance, let alone that for society at large. Furthermore, as Hayek indicates, it is impossible for government to estimate the societal benefits from R&D in advance. All that economists can say is that an innovator, in the hope of earning a given return, undertakes a research project. At the time of making the decision, the expected return is, at least, as great as the expected costs.

James M Buchanan has emphasised a distinction in those costs that can be objectively measured and those costs that impact upon choice. (56) Choice-influencing cost is subjective, and is described as being "that which the decision-maker sacrifices or gives up when he makes a choice". (57) Objective cost, however, is different and does not imply choice. Cost in this context relates to "the market value of the alternative product that might be produced ... cost is measured directly by prospective money outlays". (58) Objective cost is the ex post cost of undertaking a particular activity, not the ex ante cost. This tells us the cost of achieving a particular outcome once a choice has already been made, but nothing of the choice itself. This is an important distinction. The objective cost, the cost that can be subsidised, is only a portion of the subjective cost that an innovator might consider. Yet, economists treat it as the total cost. As Buchanan indicates, "That which happens after choice is made is what economists seem to be talking about when they draw their cost curves on the blackboards and what accountants seem to be concerning themselves with". (59) In other words, economists have little to say about the costs that can influence decisions; economists have much to say about costs after the decision-making process.

The standard economic analysis of underinvestment in R&D amounts to an exercise in "blackboard economics". Ronald Coase has expressed this notion well in two quotes. "The majority of economists ... paint a picture of an ideal economic system, and then, comparing it with what they observe (or think they observe), they prescribe what is necessary to reach this ideal state without much consideration for how this could be done. The analysis is carried out with great ingenuity but it floats in the air". (60) "This is, of course, blackboard economics, in which with full knowledge of the curves (which no participant in the actual economic process possesses), we move factors around (on the blackboard) so as to produce an optimal situation. This may well be a good way of teaching the tools of economic analysis but it gives students a very poor idea of what is normally involved in deciding on economic policy." (61)

CONCLUSION

The government spends a substantial amount of money on public research. The economic theory that provides the intellectual basis for public funding is flawed. In principle it implies that no private sector R&D would ever occur. One is reminded of the old economic saw, "That's all very well in practice, but could never happen in theory". In practice, the benefits to successful R&D are very high, and there is no reason to believe that the private sector would not undertake the necessary effort to secure those benefits.

Each of the stepping-stones in the case for publicly funded science is flawed. R&D is not a public good. The cost of public funds is not lower than the cost of private funds. The returns to public science are low, and not high as is commonly argued. Governments have a poor track record of picking "winners". Publicly funded R&D has a negative impact on economic growth, not a positive impact. Economists are unable to explain how spillovers occur, or how valuable these spillovers are. The whole argument simply "floats in the air".

The whole notion that public R&D is necessary is based on myth. Daniel Sarewitz has discussed a series of myths that surround public R&D. (62) The notion that throwing an infinite amount of money at public research will somehow, at some time, automatically lead to some benefit is a wonderful -- yet false -- myth. It underpins much of the hysterical commentary coming out of universities and other beneficiaries of public largesse. The government spends a substantial amount on public science and innovation. It is not clear that any substantial benefit is derived from that expenditure.

TECHNICAL APPENDIX

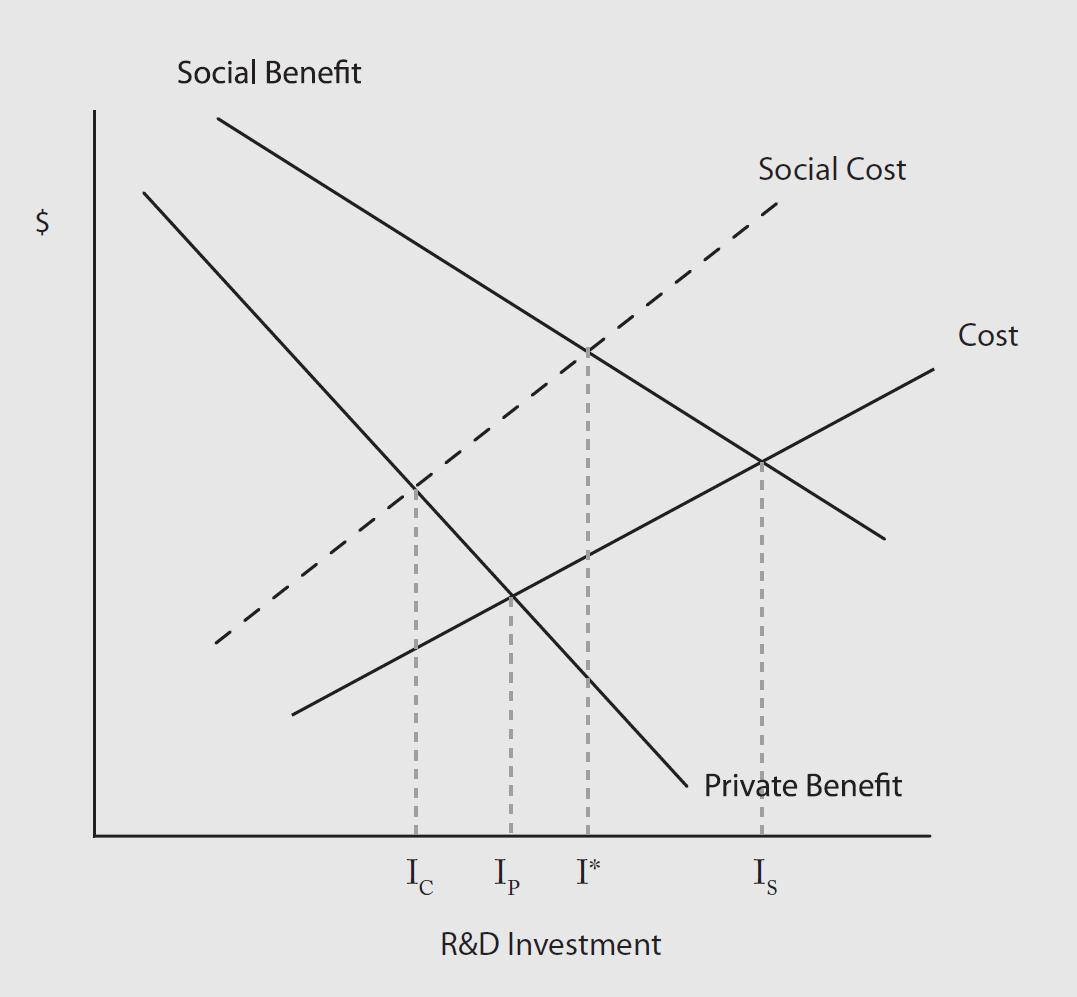

The diagram below shows the usual economic analysis that underpins the argument for public subsidy of science.

The "Private Benefit" curve shows the private benefits of undertaking R&D investment while the "Cost" curve shows the (private) costs of undertaking R&D investment. Due to the existence of spillovers, the "Social Benefit" of R&D is greater than the private benefit. The innovator would set their private benefit equal to their private costs and invest IP in R&D. If the innovator took social benefits into account, however, they would set social benefits equal to cost and invest IS in R&D. The difference (IS - IP) constitutes underinvestment in R&D and provides a basis for public intervention. Charles Jones and John Williams calibrate a theoretical growth model and estimate underinvestment to be two to four times current R&D investment. (63) This latter figure implies US gross domestic expenditure on R&D should increase from (about) $291 billion to $1.167 trillion. (64)

There are, however, some difficulties that the standard analysis glosses over. There are costs associated with public intervention. The total (social) costs are shown in the diagram as the "Social Cost" curve. If we were to set the social costs equal to the social benefits, then an amount I* should be invested in R&D. It is not clear, however, that I* falls to the right of IP. The figure is drawn showing that it does, but the social costs of intervening in the market may be far higher than expected, and the equilibrium point may be to the left of the private equilibrium. There is a further complication. If social benefits of R&D spill out of the firm into society, the costs of intervention may spill into the firm. For example, public science may increase the wages of scientists but not necessarily increase either the quantity or quality of scientists. (65) If the innovator set his private benefit of R&D equal to the social costs then the equilibrium R&D level (IC) will always be to the left of the private equilibrium (IP). To what extent does public subsidy to R&D "crowd out" private R&D?

There are two strands to the literature addressing this question. Three studies (including two literature reviews) published in 2000 shed some light on the issue from a micro-economic perspective. In short, it is unclear whether public support for R&D crowds out private R&D. Paul David and Bronwyn Hall find that the supply of trained scientists is very important in determining this question. If public intervention simply increases the wages of scientists and engineers then crowding out can occur. (67) In a review of econometric evidence, Paul David, Bronwyn Hall and Andrew Toole conclude, "the overall findings are ambivalent". (68) Finally, Bronwyn Hall and John van Reenen argue that $1 of tax subsidy generates $1 of additional R&D. (69) This implies no crowding out. It is premature, however, to draw that conclusion. Hall and van Reenen include the administrative costs of raising tax revenue, but do not take account of the deadweight cost of taxation. The social costs of government providing $1 of R&D tax subsidy are far higher than Hall and van Reenen estimate. In other words, their result is consistent with equilibrium being at IC.

The second literature that provides insight into "crowding out" is endogenous growth theory. Technology and technical progress plays an important role in driving economic growth in these models. An important assumption that requires examination is the notion that all R&D drives economic growth. This is a generally accepted approximation. As part of their 2003 analysis, the OECD disaggregate R&D into a private and public component. (70) As expected there is a positive and statistically significant relationship between overall R&D and economic growth, and also between private R&D and economic growth. There is a statistically significant negative relationship between public R&D and economic growth. (71) The OECD report concedes, "at face value [the results] suggest publicly-performed R&D crowds out resources that could be alternatively used by the private sector, including private R&D. There is some evidence of this effect in studies that have looked in detail at the role of different forms of R&D and the interaction between them." (72)

Clearly, those studies that show a positive relationship between all R&D, and private R&D, and economic growth are incomplete. In order to justify public expenditure on R&D, a positive relationship between public R&D and economic growth must be found.

In describing the benefits to R&D, both private and public, we encounter Hayek's information problem, "how to secure the best use of resources known to any of the members of society, for ends whose relative importance only these individuals know". (73) The information problem implies that only the innovator can know what the private benefits of R&D might be. It is possible to establish the social benefits of R&D after the fact, but this type of analysis relies on look-back bias and data snooping. The extent of future use of current knowledge can only be known when future entrepreneurs apply that knowledge. In other words, the social benefit curve can only be determined after the fact.

James Buchanan has emphasised a distinction in those costs that can be objectively measured, and those costs that impact upon choice. (74) Choice-influencing cost is subjective, and is described as being "that which the decision-maker sacrifices or gives up when he makes a choice". (75) Objective cost, however, is different and does not imply choice. Cost in this context relates to "the market value of the alternative product that might be produced ... cost is measured directly by prospective money outlays". (76) Objective cost is the ex post cost of undertaking a particular activity, not the ex ante cost. This tells us the cost of achieving a particular outcome once a choice has already been made, but nothing of the choice itself. This is an important distinction. The objective cost, the cost that can be subsidised, is only a portion of the subjective cost that an innovator might consider. Yet, economists treat it as the total cost. As Buchanan indicates, "That which happens after choice is made is what economists seem to be talking about when they draw their cost curves on the blackboards and what accountants seem to be concerning themselves with". (77) In other words, the "Cost" curve is an objective ex post type cost.

The argument has emphasised that the standard analysis has conceptual difficulties. There are also a number of industrial organisation issues that the literature never addresses. For example, are the firms under discussion operating under conditions of perfect competition, or do they have some degree of market power? If firms do have market power then there may be an over-investment in R&D. (78) In any event, what type of investment are we talking about? Many R&D projects end in commercial failure. Should we include or exclude investments that fail? The implicit assumption that many economists seem to make is that all R&D activity is valuable even if it is not profitable.

Economists also have great difficulty in explaining how these spillovers or positive externalities actually occur. Zvi Griliches provides a specific definition of R&D spillover as the following: "ideas borrowed by research teams of industry i from the research results of industry j". (79) What does it mean to "borrow" an idea? Broadly speaking, it seems that there exists six possibilities of how an asset can be acquired: by purchase, purchase at less than factor cost, theft, gift, acquisition following loss, or acquisition following abandonment. None of these constitute an externality. Ideas can be copied, that appears to be the Griliches view. If they are copied with permission, no externality occurs. If they are copied without permission a theft has occurred. This is a property right problem, not an externality problem. It seems that R&D spillovers, following the Griliches definition, can either be the result of some loss or abandonment. To the extent that externalities are due to a loss, the question arises why the owners of the innovation do not recover their property? Richard Nelson argues, "External economies result from [the fact] that research results often are of little value to the firm that sponsors the research, though of great value to another firm ...". (80) Spillovers occur because ideas are abandoned -- hardly a basis for government intervention.

REFERENCES

1. I would like to thank Jonathan Boymal, Robert Brooks, Heath Spong, Matthew Taylor, and George Tawadros for comments that have improved this paper.

2. James M Buchanan, 1968, The demand and supply of public goods, Volume 5, The Collected Works of James M Buchanan, Liberty Fund: Indianapolis, pg. 162.

3. Sid Shanks and Simon Zheng, 2006, Econometric Modelling of R&D and Australia's Productivity, Productivity Commission Staff Working Paper, Canberra, pg. 211.

4. K J Arrow, 1962, "Economic Welfare and the Allocation of Resources for Invention", In The Rate and Direction of Inventive Activity. Princeton University Press. Reproduced in N. Rosenberg (ed). 1971. The Economics of Technological Change: Selected Readings. Harmondsworth: Penguin Books.

5. Much is made of uncertainty in the economic literature, especially in the innovation and R&D literatures. The impact uncertainty has on the real economy, as opposed to theoretical analyses is oversold. Gordon Tullock has written, "Actually, most economic actions are taken under conditions of imperfect knowledge and under circumstances where the outcome cannot be known with certainty. In this respect applied research does not differ from other forms of economic activity" (emphasis added). Gordon Tullock, 1966, The organization of inquiry, Volume 3, The Selected Works of Gordon Tullock, Liberty Fund: Indianapolis, 2005, pg. 16.

6. Richard Ramano, 1989, "Aspects of R&D subsidization". The Quarterly Journal of Economics. 104: 863–873, pg. 863

7. David Warsh (2006, Knowledge and the wealth of nations: A story of economic discovery, New York: Norton, pg. 151) argues that Arrow implied lumpiness when he used the term "indivisible". This is a slight and subtle distinction, but does not change the general gist of the argument here.

8. Geoffrey Brennan, 1998, Foreword, In Externalities and public expenditure theory, Volume 15, The Collected Works of James M Buchanan, Liberty Fund: Indianapolis, 2001, pg. xii. Richard Nelson and Paul Romer also discuss rivalry and excludability as a two-way classification (Richard R Nelson and Paul M Romer, 1996, "Science, Economic Growth, and Public Policy", in Bruce L R Smith and Claude E Barfield (eds.), Technology, R&D, and the economy, Washington DC: Brookings/AEI, pg. 60–61.

9. Thrainn Eggertsson, 2003, "Open access versus common property", In Terry L. Anderson and Fred S. McChesney (eds), Property rights: Cooperation, conflict, and law, Princeton: Princeton University Press, pg. 85.

10. Dennis S, Karjala, 1997, "The Term of Copyright", in Laura N. Gasaway (ed.), Growing Pains: Adapting Copyright for Education and Society, Fred B. Rothman and Co

11. Sir Arnold Plant, 1934, "The economic theory concerning patents for inventions". Economica. Reproduced in Selected economic essays and addresses by Sir Arnold Plant. London: Routledge & Kegan Paul.

12. John Stuart Mill, 1989 1848, Principles of Political economy. New York: Augustus M. Kelley. p. 932.

13. Mill, ibid. pg. 933.

14. Adam B Jaffe and Josh Lerner, 2004, Innovation and its discontents: How our patent system is endangering innovation and progress, and what to do about it, Princeton: Princeton University Press, pg. 2. See also Carl Shapiro, 2000, "Navigating the patent thicket: Cross licences, patent pools, and standard setting", Innovation policy and the economy, I: 119–150.

15. See Jonathan Boymal and Sinclair Davidson, 2004, "Extending the Copyright Duration in Australia", Agenda: A Journal of Policy Analysis and Reform, 11 (3): 235–246 for a discussion of these issues.

16. Even the non-rival nature of R&D needs to be qualified. Even though knowledge and information is non-rival, it is also not free. As Terence Kealey indicates, "have you cloned an organism recently? Or etched a silicon chip? Nor have I. Even though the relevant papers are freely available, only a handful of specialists have the knowledge required to understand them". Terence Kealey, "Science spending a waste of public money", Financial Times, 13 July 2004, pg. 21.

17. Keith Pavitt, 1993, "What do firms learn from basic research?" In Dominique Foray and Christopher Freeman (Eds) Technology and the wealth of nations. London: Pinter Publishers, pg. 31.

18. Adam Smith, 1776, An inquiry into the nature and causes of the wealth of nations, Chicago: Chicago University Press, 1976, Volume II, pg. 244.

19. Adapted from Kenneth M. Brown, Kenneth, 1998, Downsizing science: Will the United States pay a price? The AEI Press: Washington, D.C., pg. 45.

20. See Richard W. Tresch, (2002, Public finance: A normative theory, Academic Press: San Diego) for a rigorous textbook coverage of this issue.

21. The argument is often made that government can borrow at cheaper rates than the private sector can either borrow, or provide equity finance. At face value, this is correct. Governments, however, have to repay their loans, usually by levying taxes in future. Borrowing simply postpones the deadweight costs of taxation into the future. The opportunity cost of funds is a function of the project being financed and is invariant to the identity of the project originator.

22. Alex Robson, 2006, "How high taxation makes us poorer", In Peter Saunders (ed), Taxploitation: The case for income tax reform, Sydney: The Centre for Independent Studies.

23. The Allen Consulting Group, 2003, A wealth of knowledge: The return on investment from ARC-funded research, Report to the Australian Research Council (hereinafter, the Allen Report).

24. Some of my own research is funded by the Australian Research Council. This section is not a criticism of the Australian Research Council per se. The Australian Research Council has come under criticism by Andrew Bolt (Grants to Grumble, Herald Sun, 19 November 2003, pg. 19 and Paid to be pointless, Herald Sun, 26 November 2004, pg. 23), Greg Melleuish (Secrecy taken for granted, The Australian, 27 July 2005, pg. 39), and P.P. McGuinness (What is wrong with the ARC, Quadrant, March 2006).

25. The actual procedure is slightly more complicated and set out in pages 36–41 of the report. The précis I have provided gives the reader a "taste" of the process.

26. The Allen Consulting Group, ibid. page 39, footnote 37, emphasis added.

27. Tullock, ibid. pg. 10.

28. We can think of this in terms of stocks and flows. The argument is that most of the historical stock of knowledge has flowed into the present. It appears to be the case because of look-back bias, but may not be an accurate understanding of the past.

29. The Allen Report cites these papers as OECD publications. In the bibliography they are identified as being STI Working Papers and Economics Department Working Papers. It is true that the OECD as part of their on-going research releases these papers, however, they do not represent the "official" OECD position. Indeed, they carry the disclaimer, "The opinions expressed in these papers are the sole responsibility of the author(s) and do not necessarily reflect those of the OECD or of the governments of its Member countries."

30. OECD, 2003, The Sources of Economic Growth in OECD Countries, Paris: OECD Publication Service.

31. OECD, ibid, pg. 85.

32. OECD, ibid. pg. 85, emphasis added.

33. The Allen Report, ibid. pg. 6. The "measured benefit" should really be the "estimated benefit".

34. The Allen Report indicates the difference between their top-down and bottom-up techniques is "not surprising" (pg. 7). First, they are unable to identify all channels whereby R&D impacts society and the economy, and they have been conservative in their analysis. These would normally be reasonable arguments. The difference between the two approaches, however, is not 11 per centage points (50–39), rather is the difference between three per cent or nine per cent and 50 per cent. In other words, the difference between 50 per cent per annum and 39 per cent over four to ten years is huge.

35. F. Narin, M. Albert, P. Kroll and D. Hicks, 2000, Inventing our future: The link between Australian patenting and basic science, Commonwealth of Australia.

36. The Allen Report is slightly misleading in this regard. It states, correctly, that 266 Australian papers acknowledge the ARC as a source of funding, while 153 acknowledge a university as a source of funding, and given that the ARC only provides 10 per cent of university research funding the ARC contribution is very valuable relative to the "average for all university conducted research" (pg. 43). These statistics are sourced from table 37 (pg. 104) of the Narin et al. report. That table sets out funding organisations acknowledged in Australian-authored papers cited in US patent applications. In that table 3236 papers acknowledge support from 36 different sources -- the ARC contribution is 266/3236 or 8.2 per cent, not 266/(266+153) or 63.5 per cent as the Allen Report implies. In an additional table (table 43, pg. 108–110) a further 138 organisations produced 1305 papers that contain no financial acknowledgements. Of those 553 were produced by universities -- at the very least, the Allen Report should compare the ARC funded papers (266) to the number produced by universities without any other funding (at least, 153+553).

37. Narin, et al., ibid, pg. 16.

38. Australian Bureau of Statistics, 2005, Innovation in Australian Business 2003, cat. 8158.0, table 6.5 pg. 49. Note, however, that the ABS indicates this statistic should be used with caution.

39. The Allen Report, ibid., pg. 54.

40. Narin, et al. ibid., pg. 11.

41. Edwin Mansfield, J. Rapoport, J. Schnee, S. Wagner, and M. Hamburger. 1971. Research and Innovation in the Modern Corporation. London: MacMillan. Extract published in R. Rothberg (Ed), Corporate Strategy and Product Innovation, Second Edition. New York: The Free Press. Similarly, a study by Booz, Allen and Hamilton, Inc. (1968) reports that it takes 58 ideas to result in one successful new product.

42. Edwin Mansfield, John Rapoport, Anthony Romeo, E. Villani, Samuel Wagner, and F. Husic. 1977. The production and application of new industrial technology. New York: WW Norton.

43. Thomas Astrebro, 2003, "The return to independent invention: evidence of unrealistic optimism, rent-seeking or skewness loving?", The Economic Journal, 113: 226–239.

44. Arthur M Diamond Jr., 2006, "The relative success of private funders and government funders in funding important science", European Journal of Law and Economics, 21: 149–161.

45. Diamond, ibid., pg. 159.

46. The Allen Report, ibid., pg. 39.

47. As William J Baumol indicates, it is not desirable that zero spillover occurs. See William J Baumol, 2002, The free-market innovation machine: Analyzing the growth miracle of capitalism, Princeton: Princeton University Press, especially chapter 8.

48. There is a very important assumption being made here. The notion that the innovator invests less because the social rate of return is higher than the private return is an assumption. This assumption follows from Arthur Cecil Pigou's original discussion of externalities. Edwin Mansfield, John Rapoport, Anthony Romeo, Samuel Wagner and George Beardsley (1977, "Social and private rates of return from industrial innovations", Quarterly Journal of Economics, 91: 221–240) caution against concluding that an underinvestment occurs simply because there exists a wedge between public and private rates of return.

49. William J Baumol, ibid. pg. 135.

50. Charles I Jones and John C Williams, 1998, "Measuring the social return to R&D", Quarterly Journal of Economics, 113: 1119–1135.

51. OECD, 2004, OECD in Figures 2004 Edition, Paris.

52. See George Eads (1974, "US government support for civilian technology: Economic theory versus political practice", Research Policy, 3: 2–16) for an extensive discussion of these issues.

53. Richard R Nelson, 1959, "The simple economics of basic scientific research", The Journal of Political Economy, 67: 297–306. pg. 306.

54. Gordon Tullock, ibid. pg. 164.

55. Friedrich A Hayek, 1945, "The use of knowledge in society", American Economic Review, 35(4): 519–530, pg. 520.

56. James M Buchanan, 1969, Cost and choice: An inquiry in economic theory, Volume 6, The Collected Works of James M Buchanan, Liberty Fund: Indianapolis.

57. Buchanan, ibid. pg. 41.

58. Buchanan, ibid. pg. 40.

59. Buchanan, ibid. pg. 43.

60. Ronald H Coase, 1988, The firm, the market and the law, Chicago: Chicago University Press, pg. 28.

61. Ronald H Coase, 1964, Discussion, American Economic Review, 54(3): 194 - 197, pg. 195.

62. Daniel Sarewitz, 1996, Frontiers of illusion: Science, technology, and the politics of progress, Philadelphia, Temple University Press.

63. Charles I Jones and John C Williams, 1998, "Measuring the social return to R&D", Quarterly Journal of Economics, 113: 1119 - 1135.

64. OECD, 2004, OECD in Figures 2004 Edition, Paris.

65. See Austan Goolsbee, 1998, "Does government R&D policy mainly benefit scientists and engineers?", American Economic Review, 88: 298 - 302, for a discussion of this point. Also, Paul M Romer, 2000, "Should the government subsidize supply or demand for scientists and engineers?" Innovation policy and the economy, I: 221 - 252.

66. Crowding out of private R&D by public R&D is discussed extensively by Terence Kealey in his 1996 book Economic Laws of Scientific Research, London: MacMillans.

67. Paul A David and Bronwyn H Hall, 2000, "Heart of darkness: modeling public–private interactions inside the R&D black box", Research Policy, 29: 1165–1183.

68. Paul A David, Bronwyn H Hall and Andrew A Toole, 2000, "Is public R&D a complement or substitute for private R&D? A review of the econometric evidence", Research Policy, 29: 497–529.

69. Bronwyn Hall and John van Reneen, 2000, "How effective are fiscal incentives for R&D? A review of the evidence", Research Policy, 29: 449–469.

70. OECD, 2003, ibid, pg. 85.

71. OECD, ibid.

72. OECD, ibid. pg. 85, emphasis added.

73. Friedrich A Hayek, 1945, ibid,

74. James M Buchanan, 1969, ibid.

75. Buchanan, ibid. pg. 41.

76. Buchanan, ibid. pg. 40.

77. Buchanan, ibid. pg. 43.

78. See George Eads (1974, "US government support for civilian technology: Economic theory versus political practice", Research Policy, 3: 2–16) for an extensive discussion of these issues.

79. Zvi Griliches, 1992. "The search for R&D spillovers". Scandinavian Journal of Economics. 94: S29–S47. Reproduced in Z. Griliches. 1998. R&D and productivity: The econometric evidence. University of Chicago Press: Chicago.

80. Richard R Nelson, 1959, "The simple economics of basic scientific research", The Journal of Political Economy, 67: 297–306. pg. 306.

No comments:

Post a Comment