International Journal of Global Energy Issues, Vol. 29, Nos. 1/2, 2008

1 INTRODUCTION

1.1 Precursors of the competitive electricity market

A dozen years ago, virtually all electricity in Australia was generated in government-owned plants, transmitted along government-owned facilities and marketed by government-owned retailers. The electricity industry comprised seven jurisdictionally based integrated utilities, which had total control over generation and sales within their respective states. Competition from other suppliers and retailers were illegal.

As in many countries, the early 1990s saw an increased awareness in Australia of the shortcomings of the integrated electricity industry's efficiency. At the same time, a better appreciation developed on the nature of the industry and that it need not be operated as an integrated unitary monopoly. Formal reports by government and private economic policy institutions (Industry Commission, 1991) lent weight to the evidence of inefficiency in Australia compared to elsewhere.

In addition, a rare level of political consensus was developing in favour of greater competition as a means of improving Australian economic outcomes. A major report (National Competition Policy, 1993) had led to the agreement by the Federal Government to provide additional funding of the state governments on condition that the latter structurally separated the parts of their network industries which were natural monopolies from those where competition was possible. This was to be followed by opening up their local markets to competition.

Electricity was the industry where these conditions were most obviously present and was singled out for particular attention. Unbundling the monopolies meant dividing each of the single state government generation and retail businesses into rival firms. It also meant requiring transmission systems to be opened on the basis of non-discriminatory access and with generators being scheduled on the basis of their bid offers.

An important factor in the evolution of the industry into a competitive market was the parlous nature of state government finances in Victoria and South Australia after a period of barely restrained expenditure increases. In Victoria, the consequent level of debt provided an incoming Liberal (conservative) government with a justification for pursuing privatisation, which is never a politically popular course in Australia. The Victorian Government's most valuable asset capable of being privatised was the electricity industry. In privatising the industry, the UK model provided a guide. In advance of the federal government's requirements to do so, the government first disaggregated the electricity monopoly to bring about structural separation of the generation, transmission and retail/distribution functions and to ensure multiple competitive providers for generation. The natural monopoly poles and wires businesses were regulated under a UK style price setting regime.

1.2 Unbundling and opening the market to competition

The original Victorian formulation was absorbed into a National Electricity Market (NEM) with a code enshrined within a National Electricity Law. Originally, a mix of state and federal law, the market rules are being moved into a unified jurisdiction.

The market itself was originally governed by the National Electricity Code Administrator (NECA) and operated by the National Market Management Company (NEMMCO). Because NECA was subject to the general provisions of the industry regulatory agency, the Australian Competition and Consumer Commission (ACCC), it proved to be rather unwieldy in its decision-making. New arrangements were introduced in the mid-2004, which created two bodies: the Australian Energy Market Commission (AEMC) to handle the ongoing development of the National Electricity Rules (Rules) that superceded the code and the Australian Energy Regulator (AER) to set prices on monopoly assets and to police the rules. State governments and state government agencies retain some (hopefully transitional) controls over retail pricing.

All seven jurisdictions unbundled the integrated supply industry into generation, transmission and retail/distribution. For Western Australia, Tasmania and the Northern Territory, this involved single businesses in the three components.

Most governments were reluctant to allow the free flow of market forces. Not only did they maintain residual controls over household consumer prices, they also insisted on cross-subsidisation of distribution and of some customer groups within their jurisdictions. In addition, in the hope of creating powerful state-based businesses, the state governments often sacrificed a larger number of competitors for a greater concentration of production in fewer suppliers. In pursuing this approach, the state governments often feared that they might otherwise be unable to carry their own political parties with the reform program. Thus NSW split its generation resources into only three entities, whereas it could have created double that. Similarly, Queensland created only two retail/distributors and south Australia only one. Tasmania also decided to maintain its extensive hydro resources under a single business.

Only Victoria went the maximum distance in disaggregating the supply industry to ensure competitive tensions. That said, the interlinked nature of the national market has gradually ensured an acceptable level of rivalry, which has driven efficiency gains across all interconnected states. (2),

1.3 Prices, producer efficiency and reliability

The Australian market-based system has been highly successful. Prices have been reduced in real terms; reliability is improved; new capacity has been brought on stream when needed; and the industry at all levels has demonstrated a very substantial improvement in productivity levels.

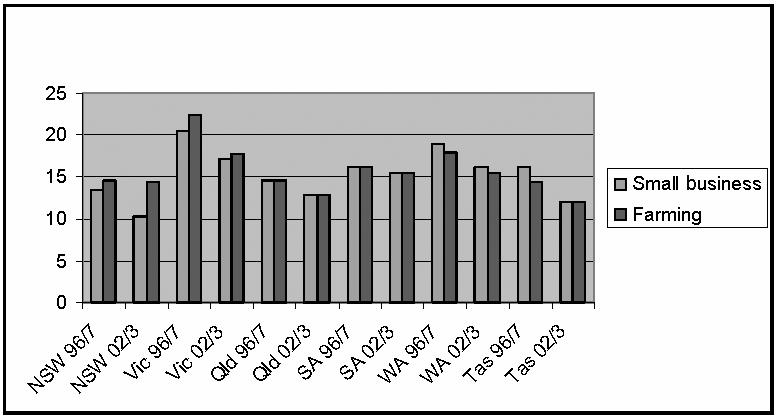

At the consumer level real prices have declined. Some controls remain on household prices in 2006, and price outcomes for this sector are therefore less meaningful. Larger customers, especially those with a relatively flat load profile, have reportedly received very substantial price reductions as a result of competition. Because discounts are now common, price data on this are not accurate. As far as rural and smaller business customers are concerned, Figure 1 illustrative of the generally downward trends.

Figure 1 Real electricity prices Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Source: Electricity Supply Association of Australia, Electricity Australia 2006.

The reliability of the system has been more mixed and is highly variable as a result of weather patterns. On average it has changed little.

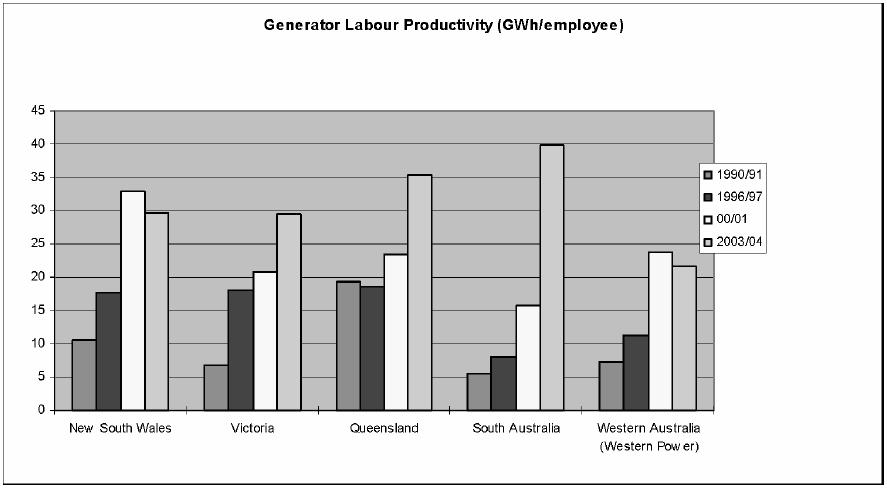

Generation facilities also showed considerable improvements in productivity. Over the dozen years to 2002/2003, the average level of labour productivity in Victoria increased sixfold. The privatised parts performed best, though all state systems improved markedly. Figure 2 illustrates this. (The data collection seeks to ensure consistency by standardising for contract workers and outsourcing, but to the extent that it fails to do so some part of the improvement may be exaggerated.)

Figure 2 Generator labour productivity (GWh per employee) Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Source: Electricity Supply Association of Australia, Electricity Australia 2006.

The stations also improved their readiness to run. This means a higher utilisation of capital and a de facto increase in capacity as well as in productivity.

2 THE WHOLESALE MARKET

2.1 Market operations

The wholesale market itself is based on a "gross pool" into which all but some small generators must bid (and into which loads can also bid, though few do). Though often raised, Australia has to date rejected the notion of capacity payments, preferring to ensure that each generator incorporates its full costs within its bids.

The pool operates on the basis of electricity being bid and prices being set on a 5 minute interval (prices, as paid, are averaged over a half hour period). Bids are submitted and the prices cannot be changed for the day ahead, but since up to ten price bands may be offered and quantities can be shifted within these right up to dispatch, suppliers actually have considerable flexibility.

Pool prices are capped at $10,000 MWh in any 5 min period, and to an aggregate $75,000 MWh per week. Prior to 2002, the cap was $5,000 MWh. The pool, in practice, however, largely works as a means of settling "overs and unders". The vast bulk of sales and purchases are by contract, usually, with a provision for payment by one party or the other of the difference between the pool and contract prices.

2.2 Market intervention

As well as spot markets, the pre-NETA UK system and most North American markets also provided for capacity payments. Capacity market payments mean a regulator determining the appropriate capacity, who has it and how much they should be paid for it. It is only conceivably useful if it provides an investment signal some years out rather than in near time periods. Creating a design for this is especially difficult.

A capacity market approach overrides commercial parties' decision frameworks. Among the deficiencies of this is a muting of the market for reliability -- for example in the demand side bidding. It also leads to pressures to cap energy bids in ways that prevent prices from providing commercial returns. Those markets that have had a separate capacity payment have often found its outcome to be unsatisfactory. Payments reached almost one quarter of returns in the England and Wales market. In the New England market, it has often become the main focus of competition and the capacity price has mainly been close to zero.

The NEM is designed as an energy-only market. (3), The primary mechanism to underpin new generator investment is the forward contract price. That in turn is driven largely by the retailer's fear of extreme payments, should they be inadequately hedged during high prices associated with tight supply/demand? While this is unquestionably a more efficient and competitive mechanism for delivering new investment, it does require a degree of courage. It needs to have potentially very high commercial risks and needs to be unfettered by expectations of intervention that may interfere with those risks.

Australia has a Reserve Trader scheme, which is an alternative measure to address perceived inadequate new investment levels. This is a form of insurance against the market not performing appropriately. When the System Operator (NEMMCO) predicts a shortfall some months ahead, it tenders for suppliers or demand side interruption that was not intending to participate in the energy market to provide reserve capacity over the forecast shortfall period. This capacity is then offered into the energy market at the price cap, thereby averting load curtailment without suppressing price. The supplier is paid a fixed tendered fee levied from all customers.

While the mechanism itself should not depress prices, it can distort the energy market by providing a form of subsidised new entry -- when the contract concludes, the supplier may then join the market. It can also provide a more attractive alternative to incumbent suppliers than the energy market. This appears to have been the case in the 1998 summer when a peaking plant, Ecogen's Newport Power Station, was mothballed due to weak market conditions. However, it then won a reserve trader contract whose necessity was provoked by its withdrawal. This would appear to be a clear case of market design failure. Since that time, however, the doubling of the price cap and imposition of less conservative reserve standards appear to have averted a repetition of a plant being enticed back into supply after having previously declared itself unavailable.

Suppliers are not able to opt for spot market unavailability, bid for reserve availability and, should they not be contracted, then decide to become available. Hence there is little scope for abuse. Even so, the Reserve Trader provisions have continued to be used signifying greater risk aversion on the part of the market manager and with prices that are as a result higher than they otherwise would be.

2.3 Market manipulation: issues in principle

A great deal of time and analytical resources have been spent on the issue of "ethical" bidding by generators. Businesses in North America have been accused of wrongdoing by bidding in excess of marginal costs and withholding supply. In Australia, exploiting a monopoly power in this way is referred to as "gaming" the market.

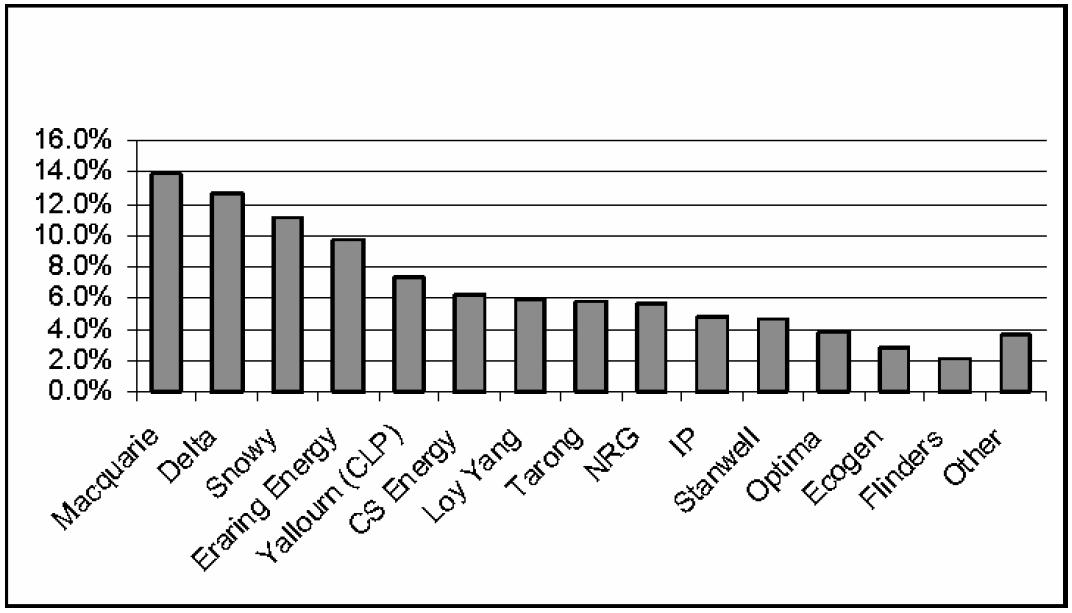

If such activity has to occur frequently, either a monopoly or some sort of cartel is required. In Australia, there is a wide ownership spread of electricity supplies and no supplier has a monopoly. Cartels are illegal and few private or public employees would take the risk of severe penalties by overlooking this. Moreover, it is very difficult to make price boosting cartels stick simply because all parties have different allegiances and will seek to take advantage of the higher prices that have been created. Adam Smiths' oft quoted phrase argued, "People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices". But Smith went on to counsel against intervention by the authorities saying, "In a free trade an effectual combination cannot be established but by the unanimous consent of every single trader, and it cannot last longer than every single trader continues of the same mind". Figure 3 illustrates the extent of competition in Australia.

Figure 3 Major generators' market share Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Source: Electricity Supply Association of Australia, Electricity Australia 2006.

In Australia, proposals to prevent generators exploiting temporary monopoly largely focused on restraints over bid changing or "re-bidding". In the US energy markets, concerns have gone further than this and firms are often regulation constrained from bidding much above their marginal costs.

Price is at the heart of the discipline of economic analysis. It is the ultimate proxy for the value people assign to a purchase, and the cost to producers in its supply. Price is, therefore, the means of signalling new supplies and rationing existing supplies.

However, there is not a great deal of material in the economics literature on the procedures by which the price gets set, especially when the product is subject to rapidly changing demand and supply and when costs have a large fixed cost element.

Marginal costs were long considered to be the means by which markets will offer the optimal balance and operate efficiently. A marginal cost-based explanation is, however, difficult to apply to firms outside the perfect market situation. Pricing at marginal cost generally allows profitable production where costs are rising with additional output. With incremental costs falling because of lumpy capital marginal cost pricing defines the least price at which a seller can supply his product to the market for a certain amount of time. A price below this is not uncommon for short periods -- some goods are given away as a promotional exercise, while electricity commonly is offered at a negative price to ensure a station is operational when a better price is being set.

These and other deviations from charging above marginal cost, on closer scrutiny, are not exceptions to the general rule that requires a firm to profitably cover all its costs if it is to stay in business. Marginal cost-based prices that fail to cover average costs mean, if they are applied, their efficiency in allocating the good itself is offset by the inefficiency in allocating the capital to produce it in the first place. If a firm's capital cost can be covered by a lump sum payment, marginal cost pricing for the units as used is highly efficient. A lump sum payment is easiest to accommodate in government-owned monopoly facilities. But those facilities are notoriously cost padded and often built unwisely. Elsewhere, however, we see it in areas like gas pipelines where customers offer take-or-pay contracts.

For electricity, using marginal costs as a basis for price setting has diverse implications for the different sorts of plant. First, there is the energy-limited plant, usually thought of as hydro-based plant, or sometimes gas-fuelled where there is a daily limit. Second, there is the highly capital-intensive baseload plant, which has a marginal cost in Australia of between $5 and $15 per MWh. Finally, there is the high-cost plant designed to operate only for a few hours per year but requiring very high prices, perhaps in the thousands of dollars, for those few hours if it is to be viable.

Almost everyone is in agreement that the energy-limited plants should bid in a way that ensures they operate at the time when demand provides them the best price. But for the other plants, there is a perception that they ought not to "game" the market by exploiting any temporary monopoly powers they might have. In some markets, the regulator places a plant-by-plant limit on the price that might be bid. Usually, that limit is associated with some capacity mechanism price under which a portion of fixed costs are covered.

It is the basis of much of the analysis of the Californian market collapse that the market in California deviated from the competitive ideal. Although this is uncontroversial, the analysis, for example, of Bushnell and Wolak (2000), is posited on wrongdoing where prices exceed system marginal costs because those bidding into the market were taking advantage of temporary monopoly. The paradigm promoted in their analysis relies on non-energy-limited plant bidding their true marginal costs.

Yet we do not see marginal cost pricing behaviour being routinely followed in other markets. Thus, for example:

- Newspapers have a trivial marginal cost and are clearly operating in oligopolistic markets, still seldom does the price fall to zero even when there is very intensive competitive wars.

- Cable TV once the satellite space is booked, is relatively cheap to bring to additional homes, still seldom does its price fall to near zero levels.

- Airlines seldom sell seats at the bare minimum needed to cover marginal costs (though Ryanair appears to do so) even when planes are far from full.

One reason why marginal cost-based prices cannot occur on a regular basis is that the marginal producer would not recover the cost of its plant and would avoid building it in the first instance. This would unravel the whole supply system. Those who consider, that the situation is saved by having energy-limited plant bid to maximise its revenue need to explain how to treat the plants competing in similar market segments and even if an exception were to be made for energy-limited plant, this clearly would not work in all electricity markets.

The most important discipline on the supplier in electricity markets is that of competitors. All suppliers seek to maximise profits and the economists or regulators who try to prevent this are frustrating the market processes that drive efficiency. There are hardly any real life examples of perfect competition in which the supplier is a pure price taker and if efficiency rested on this premise, market economies would not have prevailed in the way they have.

For the profit-maximising firms that populate the electricity industry in Australia, bidding above marginal cost is actually, and quite properly, inevitable. Cramton (2004) illustrates this. He shows how a 1,000 MW plant will bid the last MW at the price cap if this can be profitable. Thus, simplifying the Australian market, if the last MW of a 1,000 MW plant is bid at $10,000 per MWh and this sets the price for an hour, the plant receives this for all its output, earning revenue of $10,000,000. If it fails to set the price and the marginal bid is $9,900, the firm earns ($9900 �� 999) $9,890,100, losing out only on the last MW and foregoing revenue of $9,900 from the last MWh. If its marginal cost for the last MW is $100, it has foregone $9,800 in the example.

Hence, it is outlaying $9,800 hoping to gain additional revenue for all its output or ($100��1000) $100,000 less than the $100 incremental cost. In the example, if it estimates the chances are better than 10 : 1 of setting the higher price, this is the best option. The constraint on the firm's actions is the existence of other firms all seeking to do the same thing, but losing marginal revenue when their competitor edges them out. The more players, the more potent that constraint until, with the stylised perfect market, comes fully constrained behaviour.

Over time, as firms learn more about their competitors' behaviour, the scope to gain diminishes. This tends to mute the degree to which firms will put some capacity at risk since their competitors' behaviour becomes familiar. But they will commonly leave some supply at high levels because that behaviour is never fully anticipated and because the circumstances of competitors are likely to change as a result of outages, etc. Prices are, therefore, not closely related to fixed costs but reflect marginal costs and the levels of competition.

The other major factor in quelling the firms' proclivity to take advantage of their demand curves is forward contracting. Once a firm has a contract, it has no incentive to bid at greater than marginal costs for the contracted part of its output. And suppliers are as keen to forward contract as are the retailers, since this means risks are hedged. The forward contracts normally have a premium over marginal costs reflecting greater upside price risks.

Contracting is also the means by which high-cost marginal plant is produced -- its effect is, therefore, an insurance contract rather like the supply side contracts that retailers have to enable back-offs at needle peaks.

Hence, the willingness of firms to bid some capacity above marginal cost and to seek to raise prices is crucial to the incentive for additional investment. If marginal costs are all that can be won, this would mean very discontinuous investment decisions driven by sudden soaring prices which, unless locked in, would collapse as soon as new capacity was brought onstream. Indeed, it is hard to see how any investment in high fixed cost assets would take place.

2.4 Market manipulation: evidence from among Australian suppliers

The following charts, derived from the data published by the consultancy service, Intelligent Energy Systems, examine some station bids on a hot day in summer to explore business strategies and as a means of assessing whether monopolistic outcomes emerge.

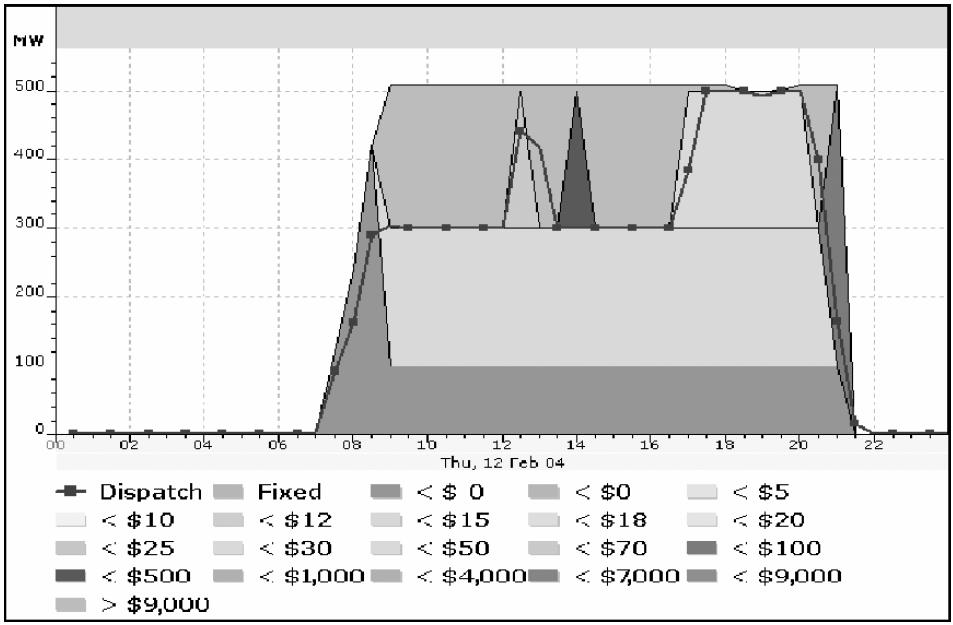

The first, the privately owned Loy Yang A, is offering power at the limit of its capacity at a relatively high price but it is also raising its supply price at the peak hour to the $9,000 per MWh level (Figure 4).

Figure 4 Seventeen station bidstack (Loy Yang A)

The intermediate Newport station bids in an apparently erratic fashion. Again, however, this reflects contracts (especially with TXU) and its marginal costs. If the firm can push the price up for the odd short period, they will take it (Figure 5).

The same pattern is seen with the government-owned stations. Here is Bayswater seeking to gain increased spot revenue where it has an absence of contractual cover (Figure 6).

Figure 5 Seventeen station bidstack (Newport)

Figure 6 Seventeen station bidstack (Bayswater)

Bidding strategies reflect a constellation of marketing behaviour with businesses seeking to maximise their profits and, without jeopardising longer term relationships, take advantage of any window of market power that might fleetingly open. Analogous marketing behaviour can be observed in similar markets with spot and contract elements like hotel rooms and hire cars. The diverse marketing strategies stemming from different contractual and cost positions as well as different analytical frameworks, far from detracting from market efficiency, contributes to it. Seeking out premium price opportunities delivers signals to the supply side to be ready to meet these.

As long as there is adequate competition, and the number of players in the Australian National Market clearly meets this criteria, economic rents cannot be earned on anything other than a transitory basis. Efforts to prevent these transitory rents will bring supply inflexibilities and higher prices in the long run.

In Australia, the overall prices remain low (Figure 7). On both the spot and contract markets, they have remained below the $40 per MWh level that was widely regarded back in 1995 to be the new baseload investment level. In today's money, this would equate to about $50 per MWh. Average pool prices in the most recent period, June 2005 to March 2006, ranged from $29 in Queensland to $39 in NSW (Table 1).

Figure 7 (a) Regional quarterly volume weighted average spot prices since market start;

(b) d-Cypha Trade regional quarterly base future prices Source: Australian Energy Regulator.

Source: Australian Energy Regulator.

Table 1 Average Prices $/MWh

| Qld | NSW | SNOWY | VIC | SA | Tas | |

| 2005–2006 | 31 | 43 | 29 | 36 | 44 | 59 |

| 2004–2005 | 31 | 46 | 26 | 29 | 39 | |

| 2003–2004 | 31 | 37 | 22 | 27 | 39 | |

| 2002–2003 | 41 | 37 | 27 | 30 | 33 | |

| 2001–2002 | 38 | 38 | 27 | 33 | 34 | |

| 2000–2001 | 45 | 41 | 35 | 49 | 67 | |

| 1999–2000 | 49 | 30 | 24 | 28 | 69 | |

| 1998–1999* | 60 | 25 | 19 | 27 | 54 |

*The AER analysis of flat contracts shows no general upward movement.

The point about all this is that with almost total freedom of electricity firms to seek the best possible price for their product, they, like other such suppliers in the economy, are only achieving a modest level of profit. Yet, we have seen windows opening where firms have spotted (or thought they spotted) opportunities to expand. Though, the presence of government-owned facilities may well be distorting new provision -- a point that is addressed in the concluding comments -- the market has, to date, not only produced lower prices but also resulted in capacity increases in line with demand. This is illustrated in Figure 8 and Table 2.

Figure 8 Peak demand and capacity in the NEM Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Table 2 New capacity 2000–2006

| State | Capacity (MW) | Type | Ownership | |

| Redbank | NSW | 150 | Coal | Private |

| Bairnsdale | Vic | 92 | Gas | Private |

| ValleyPower | Vic | 300 | Gas | Private |

| Somerton | Vic | 160 | Gas | Private |

| Laverton | Vic | 312 | Gas | Government |

| Loy Yang | Vic | 236 | Coal | Private |

| Oakey | Qld | 282 | Gas | Private |

| Millmerran | Qld | 852 | Coal | Private |

| Swanbank E | Qld | 360 | Gas | Government |

| Tarong N | Qld | 450 | Coal | |

| Kogan Creek | Qld | 750 | Coal | Government |

| Braemar | Qld | 450 | Gas | Private |

| Hallett | SA | 220 | Gas | Private |

| Pelican Point | SA | 500 | Gas | Private |

| Ladbroke | SA | 80 | Gas | Private |

| Quarantine | SA | 100 | Gas | Private |

Source: Electricity Supply Association of Australia, Electricity Australia 2006.

3 TRANSMISSION ISSUES

3.1 Distances between loads

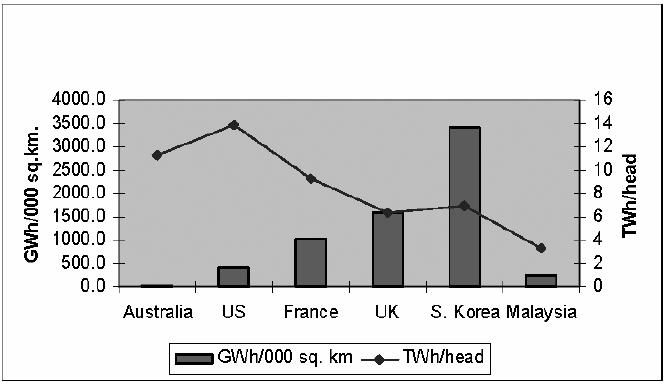

Australia's size, the geographic dispersion of its loads and the associated low population density brings a unique dimension of issues for power generation and transmission. Australia's electricity usage approaches 12 terawatt hours per capita, somewhat higher than most European countries and not much less than the USA, but in terms of usage by area, Australia is dwarfed by all other developed countries. Australia uses less than 30 gigawatt hours per thousand square kilometers, which is only one % that of Korea, and 3% that of France and 7% that of the USA. This is illustrated in Figure 9.

Figure 9 Density of electricity coverage Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Source: Electricity Supply Association of Australia, Electricity Australia 2006.

Even discounting for the fact that 60% of the continent is very lightly populated semi-desert, its marked geographic dissimilarity with other countries requires considerable adaptation of the practices that operate successfully elsewhere. In particular, incremental transmission costs can be similar to building new generation. Hence there is considerable potential for distortion as a result of the operations of different cost recovery arrangements based on the industry norm of a regulated transmission system and a market-based generation.

Pre-1995, the only links between different jurisdictions were those between NSW and Victoria and between Victoria and South Australia. The Victoria–NSW link was a by-product of the Snowy Hydro, a 4,000 MW development that uses water from and provides power to both states. The Snowy system's transmission offered a bridge to the two states, though transfers were limited to modest interchange on the basis of sharing saved fuel costs.

The link between South Australia and Victoria was developed to allow South Australia to take advantage of cheaper Victorian supplies rather than developing local new generation sources. The flows were contracted by the South Australian monopoly utility, ETSA, and activated to take advantage of the lowest marginal cost source of electricity. Some 30% of South Australian electricity was derived from Victoria.

3.2 The interface between regulated transmission and generation

Reviews of the industry, including the 2002 Council of Australian Governments' (CoAG) Energy Market Review (2002) (the Parer Report), have found aspects of the market that can be improved though it is electricity transmission that has been of greatest concern. Under the present policy framework, generation and retailing are treated as market-driven contestable sub-industries and transmission and retailing as natural monopolies that require some regulatory control. The regulatory/competitive dichotomy is, of course, not hard and fast. Some -- primarily small isolated -- regions may find it difficult to ensure sufficient competition in generation or retailing. And there are developments, especially in transmission, which may be eroding the supply monopoly.

These issues aside, the interface of a regulated with deregulated parts of the industry poses considerable risks to efficiency and commercial viability. Regulated output prices using inputs with deregulated prices can, as has been seen in California, quickly bring ruinous cost squeezes. More commonly, unless the regulation is highly attuned to the true market position, it can lead to a gradual erosion of the incentives that are essential to drive efficiency in any industry.

The issue of transmission sufficiency has been thrown into relief by two factors. First, demands for greater capacity between the main state systems. And secondly recent strains on the pre-existing transmission system in the light of the gradual build up of supply and demand. Also, as discussed later, there have been issues stemming from the increased supply of subsidised wind power, which is normally remotely located both to take advantage of more commercial wind speeds and to avoid local objections.

Lack of seamless transmission links between the main states leads to the different prices, observed in average terms in Table 2. In order to mitigate risks, NEMMCO auctions "settlement residues", which are the price differences that occur when market prices separate due to transmission congestion. This allows price hedging for trades between regions. But there is no perfect hedge since the lines' capacity is unpredictable and often fails causing congestion and major price divergence. When lines' capacity is reduced, so is the amount of settlement residue. Settlement residues auction returns and residues paid out are shown in Figure 10.

Figure 10 Interconnector settlement residues ($M) Source: NEMMCO.

Source: NEMMCO.

Though the national market basically envisaged a centrally planned transmission, it was also recognised that transmission and new generation are alternative approaches. The trade-off between nearby and remote generation (via transmission) is especially marked in Australia, where distances between load centres are vast and transmission costs can therefore be high.

In principle, new generation is required to pay the costs of augmenting the system. (4), However, this has seldom been the outcome for major new generators, partly because aside from inter-state connects the transmission system was overbuilt and no scarcity was evident in the first few years of operation. State governments were also keen to ensure new generation became available and smearing transmission costs across consumers was a means of encouraging increased generation build.

Transenergie, a subsidiary of Hydro Quebec, built two entrepreneurial links where transmission shortages were evident. Transenergie sought to finance these links by selling generators' access rights to markets and by arbitraging price differentials. These developments gave rise to issues concerning the circumstances under which a regulated augmentation of links should be permitted. (5) In the event, the merchant links in Australia could not compete against the links receiving a regulated return and have applied for and been given regulated status (Cook, 2004).

The danger is that links which are financed by a compulsory charge on the customer might lead to incentives to site generation in places that are distant from major markets. If someone else is paying for transmission, the rational generation business will be indifferent to its costs, thus distorting the efficient trade-off between transmission costs and generation costs.

The case for regulated transmission rests on its indivisibility and consequent externalities, which are too great to allow profitable merchant transmission since the price benefits accrue to all and not only to those paying for the asset. But a new generation facility will also tend to suppress the price of all delivered electricity in its interconnected region in a process similar to that of a transmission link introducing new power. Few would argue that generation should therefore be government-owned or subsidised.

A transmission line offers no more market power than that of a significant generator portfolio. Inter-ties in Australia can account for some 35% of supply (Victoria to South Australia) but normally provide much less than this. Hence even though Direct Current (DC) links (the only practicable means of supplying market-based transmission) are controllable, their market power is confined to influence over those wishing to export. Such firms are capable of writing contracts to cover the vulnerabilities they foresee.

The present position in Australia regarding transmission is that regulated links will be permitted as long as a net market benefit is judged by the regulator to be the outcome and as long as the proposed link is the best of a range of feasible alternatives. This, however, remains dissimilar from the decision-making structure that is seen in the generation sector or in markets more generally, since it may incorporate some to the network benefit externalities which a comparable investment in a new generator would not capture.

Some would argue that there is a difference between augmenting transmission for reliability reasons and augmenting it to facilitate trade. However, the two, under close consideration amount, to the same thing.

Cook (2004) assembled the following estimates of four proposals' regulatory benefits (Table 3).

Table 3 The calculation of the regulatory test benefits

| Benefit ($M) | Riverlink* | QNI† | Murraylink‡ | SNI** |

| Energy | 4 | 90 | 82 | 25 |

| Reliability | - | – | 62 | – |

| Deferred generation | 158 | 571 | 54 | 154 |

| Deferred network | 15 | - | 24 | 18 |

| Total | 177 | 661 | 222 | 197 |

* Report on Technical Issues, Costs and Benefits Associated with the Riverlink interconnection -- Between the Electricity Networks of South Australia and New South Wales, undated, Schedule 2.

** London Economics, 1997.

† Murraylink Transmission Company Application for Conversion and Maximum Allowed Revenue, Decision 1 October 2003, ACCC, page 75.

‡ Economics Evaluation of the Proposed SNI Interconnector, Roam Consulting Pty Ltd, October 2001, Results for Simulation J-S-M.

Note: SNOVIC400 Regulatory Test benefits unavailable.

In the case of the proposed regulated Riverlink line between NSW and South Australia, the estimated value of deferred investment was $158 million. This was largely predicated on reserve capacity estimates being a relatively low 12.5%. However in the 3 years following the proposal over 1,000 MW of new capacity was commissioned on top of the pre-existing South Australia capacity of 2,980 MW, bringing the reserve capacity margin to 32.8%.

Similarly, QNI (between NSW and Queensland) was estimated to bring $571 million of deferred generation benefits included $351 million for Queensland where supplies were tight at that time. In the event, in the subsequent 2 years, Queensland's pre-existing capacity of 8,400 MW was augmented by 2,500 MW of additional capacity.

In these and other cases, the estimates of value of the proposal were based on a static situation in which other suppliers are assumed not to react to the same opportunities. Yet the inclination at the time was to further facilitate the allowance of regulated links by incorporating into the estimates of the value "competition benefits" the they bring. This is a departure from the outcome obtainable by a private entrepreneur. A private entrepreneur would be most unlikely to be able to capture all the value from arbitraging prices between two areas. The entrepreneur could not arrange for the price discrimination necessary to obtain the consumer surplus that is represented. Still less would the entrepreneur be able to capture the consumer surplus value that stems from the price reductions forced on incumbent suppliers. Hence a regulated investment justified on the basis of such benefits is overvalued vis-à-vis a private investment.

The AEMC is again reviewing this issue (AMEC, 2006). In a paper issued on March 2006, it canvasses the approach of assigning certain forms of property rights to the transmission systems facing constraints as a means to provide greater incentives for generators for building the transmission required to bring their power to major nodes. It noted that such an approach in essence prevails in the PJM system.

A more comprehensive form of this approach has been advocated previously by the present author (Moran, 1999). Ideally, this would assign a share of the available transmission to incumbent generators (many of which have been sold on the implicit assumption that transmission to the main node they service is fully accessible). Major new generation would then be required to finance any additional transmission capacity that its output required (or buy such capacity from a plant that was contemplating retirement). This would avoid the tortuous public hearings and risks of inappropriate customer funding of new transmission.

4 RETAILING AND DISTRIBUTION

The original market design in Victoria and elsewhere envisaged stand-alone businesses concentrating on generation, retail/distribution or transmission. Retailing and distribution were separated by a required ring-fencing arrangement but stapled together because few saw a significant role or a possibility of substantial value in a stand-alone retail business.

Retailing has in fact proven to be a profitable and highly rivalrous activity. Retail competition was introduced with sequential tranches of decreasing customer size being progressively opened to non-host retailers. The process was completed by 2003 in NSW, Victoria and South Australia and in 2006 in Queensland.

Once they became free to do so, all the larger businesses quickly moved to contracts, mainly with businesses other than their host retailer. The household markets have also seen high churn rates -- over 40% of households have moved from standard contracts in Victoria and South Australia (though only half that level in NSW due to various market interventions including a mandatory insurance scheme, now being removed, which favour the government retailers).

While the joint ownership of retail and distribution was considered to be vulnerable to re-aggregation, the retail/distribution separation has proved to be enduring. The reality of the two functions being different business types with dissimilar customer interfaces forced them apart. Within a few of years of privatisation, one of the five original Victorian distributor/retailers bought a failing rival business, spinning off the joint retail arm into a third party, Origin Energy, which was operating without any distribution activities.

This structure was followed by another of the private businesses and further merger activity in the mid-2006 has meant that none of the private businesses now have both retail and distribution arms. This pattern is being followed by the government-owned businesses with the Queensland Government proceeding to sell its state-owned retail assets.

By the same token, retailing has attracted stand-alone start-ups, which have performed remarkably well. One of the most successful, Power Direct, recently was taken over by a Queensland Government retailer (which is itself now slated for privatisation) at a price of $122 million.

Similarly there has been a totally unexpected move towards retailing acquiring generation assets and generators becoming retail businesses. In 1999, the retailer, TXU, moved upstream by entering a long-term contract with the peaking generator, Ecogen, that gave it a position similar to merchant ownership. In 2000 it directly acquired another, Torrens Island. There were also moves upstream with the foundation by base-load generator Yallourn of a retail arm, Auspower. Treated as something of an aberration initially, it targeted only the largest customers. Other generators have since established retail arms.

Other retail businesses have also moved downstream into generation. In one case, AGL, this has involved the business taking a major stake in a large baseload power station (Loy Yang) and acquiring a significant hydro facility (Southern Hydro). AGL is now in the process of divesting all its distribution assets in an asset swap with Alinta, which is primarily a distribution and pipeline business.

Hence, competition has led to a variety of market participants. We neither have the vertical reaggregation, which some feared may be an outcome, nor do we have stand-alone players operating exclusively in one area of supply. Instead, the outcome appears to be towards specialist network businesses, which face a high degree of regulation, and businesses that straddle both the competitive side of supply, retail and generation.

The tendency for retailing and generation to form corporate links appears to reflect a risk management strategy, whereby a spectrum of forward positions is taken ranging from short-term contracting to asset ownership.

The national regulator initially opposed these reaggregations fearing that the dissolution of the original structural separation would bring about a contamination of the competitive market. This has not occurred. Retailing has established a major position within the industry. No matter what corporate affiliations are in place, no retail arm would agree to leave itself vulnerable to the lack of confidence of non-affiliated suppliers by favouring related parties. No retailer could afford to leave all its business in the hands of a single supplier.

Such outcomes are by no means unique in business. Many motor vehicle assemblers buy components from rivals and would only continue to do so if confidentiality and even-handedness is preserved. Food processors too often contract production with rival firms.

5 ACCOMMODATING WIND AND OTHER GREEN ENERGY

Though not having ratified the Kyoto Convention, Australia has introduced policies designed to reduce greenhouse gas emissions. In June 2006, the Commonwealth Government announced a review of nuclear energy, against which most states currently have specific legislation.

The major greenhouse gas mitigating measures in force as at May 2006 with impacts upon the energy industry were:

- the Federal Government's Mandatory Renewable Energy Target (MRET),

- the Queensland's 13% gas target (a subsidy to increased gas use),

- the NSW's Greenhouse Gas Abatement Certificate (NGAC) scheme.

The MRET scheme's focus is on renewable energy and requires retailers to acquire and annually surrender a progressively increased number of Renewable Energy Certificates (RECs). The scheme requires 9,500 GWh in designated new green energy forms, a level which by 2010 is 4.1% of forecast electricity consumption. Wind is likely to increasingly account for the RECs growth.

The Queensland scheme seeks to substitute gas for coal-based electricity inputs, while the NSW scheme introduces a penalty on CO2 graduated in line with the emissions per unit of energy of each electricity generation source.

The State of Victoria has introduced policies that will require 10% of electricity to be generated by renewable power, the incremental sources of which will largely comprise wind power.

Based on default penalty charges, the costs for the Commonwealth, NSW and Queensland schemes respectively are $40, $14.3 and $13.1 per MWh. The Victorian scheme's default penalty charge is an indexed $43 per MWh. By 2010, when the schemes are at full maturity, based on these premia, the estimated annual costs in today's dollars are:

- MRET $380 million

- NSW NGAC $222 million

- Queensland 13% gas $68 million

- Victoria $146 million

Wind, the lowest cost readily available new source of green energy, at around $75 MWh is roughly twice the cost of conventional coal-based energy. Wind's intermittent nature also requires increased back-up generation and the greater dispersion of wind turbines also entails higher transmission costs (especially since Australia's most prospective areas are remote from major population centres). Some concessions have already been given in allowing wind transmission costs to be smeared across the system.

Issues brought by green energy include the increased costs that stem from this source of energy (wind's costs at $75 MWh compare to $35–40 MWh for coal-based generation with $60 MWh widely assumed for nuclear). In the case of wind, some additional costs are also incurred to ensure increased stand-by back-up due to wind's intrinsic volatility. Investment uncertainty about future regulatory regimes and, in Australia's case, a series of different regulatory regimes also complicate the picture.

6 CONCLUSIONS AND ISSUES FOR THE FUTURE

The Australian industry's restructuring and partial privatisation commenced in the mid-1990s. The vertically integrated monopolies were disaggregated and all units were reorganised into corporate entities subject to normal company law. Those parts that were not natural monopolies were opened to competition.

In terms of productivity gain, consumer prices and reliably meeting new demand the changes, which were strongly opposed at the outset, have resulted in great success. Privatisation continues to be successfully resisted by unions and other pressure groups and half the industry remains under government ownership.

Most issues for the future of the industry stem from government intervention. These include the endemic issues surrounding transmission build and its pricing. Getting transmission on a market basis has proven to be among the most difficult (some say intractable) issues worldwide.

Likewise, the issue of setting prices for established facilities -- transmission and distribution -- can never be absent from controversy and the intercession of a regulator is always prone to mistakes by under-allowing price increases. A resultant capital constraint was claimed to have been one of the causes of the poor performance of the main Queensland distribution business.

Queensland has the fastest load growth and has seen five major base load power stations built of recent years. The government encouraged private investment to enter the market. A Shell-dominated consortium built one power station in 2002 and took a half share with the government in another. The government, however, has proceeded to build additional power stations. This devalued the investments and Shell gradually sold down its holdings with the final tranche valuing the investments at little more than half of their original cost.

If governments are building generation capacity for returns that are not commercial, this carries risks for the future since it may make it difficult for private capital to become involved in a supply sector that has non-commercial players. With transmission that is built on a cost-regulated basis, such activities can also impact on linked markets.

Similar risks are evident in retail pricing caps, which can result in firms vacating the field of competition unless increasingly onerous requirements are placed upon them. Fortunately, retail pricing restraints are gradually being lifted.

Future concerns largely revolve around government intervention through ownership and environmental matters. Other ongoing threats follow from the necessity of regulatory agencies setting prices and supply standards for "poles and wires" and the possibility of inconsistent treatment that might arise where regulated transmission offers a rival solution to new generation facilities. Also recently there have been issues stemming from the increased supply of subsidised wind power, which is normally remotely located both to take advantage of more commercial wind speeds and to avoid local objections.

REFERENCES

Bushnell, J. and Wolak, F. (2000) "Regulation and the leverage of local market power in the California electricity market", UC Berkeley, Competition Policy Center, No. Cpc00-13 May 2000 (for less interventionary approach see, Frank Wolak, "Sorry, Mr. Falk: it's too late to implement your recommendations now", The Electricity Journal, August/September, pp.50–55).

Cook, A. (2004) "Maintaining the security of supply to south australia through interconnections", Address to South Australian Power Conference.

Cramton, P. (2004) "Competitive bidding behavior in uniform-price markets", Paper presented at the Hawaii International Conference on System Sciences. In proceedings.

Energy Market Review (2002) (the Parer Report) Council of Australian Governments' (COAG).

Industry Commission (1991) Report: Energy Generation and Distribution.

Tasman Institute (1991) A Rebuilding Strategy for Electricity in Victoria.

Moran, A. (1999) "Firm access rights: the key to efficient management of transmission", Submission to The NECA Transmission Pricing Review, Energy Issues Paper no. 12.

National Competition Policy (1993) The Hilmer Report, AGPS.

Smith, A. (1776) An Inquiry into the Nature and Causes of the Wealth of Nations.

NOTES

1. Helpful comments were received in the preparation of this paper from Ben Skinner (TRU energy) and Alex Cruickshank (AGL). Opinions and any errors remain my own.

2. Interconnected states are Queensland, New South Wales, Victoria and South Australia. Tasmania connected via an undersea cable in 2006.

3. Western Australia's market is based on contracts with a day ahead pool market for residual demand. This has price caps of $150–$450 MWh–1. The previously integrated monopoly was converted into a single generator business (Verve) and a single retailer (Synergy), which has monopoly over those customers with an annual bill of less than $8,000. A reserve capacity mechanism is in operation.

4. The Rules specifies at 5.5 (6)(f).The Network Service Provider and the Generator shall negotiate in good faith to reach agreement as appropriate on the:

- amount to be paid by the Generator to the Network Service Provider in relation to the costs reasonably incurred by the Network Service Provider in providing generator access

- compensation to be provided by the Network Service Provider to the Generator in the event that the generating units or group of generating units of the Generator are constrained off or constrained on during a trading interval and

- compensation to be provided by the Generator to the Network Service Provider in the event that dispatch of the Generator's generating units or group of generating units causes another Generator's generating units or group of generating units to be constrained off or constrained on during a trading interval.

5. This brought a voluminous level of studies. Those in Australia include the sceptical like Mountain, B. and Swier, G. Entrepreneurial interconnectors and transmission planning in australia, the electricity Journal, March 2003. London Economics in its work for the ACCC (Review of Australian Transmission Pricing, 1999) also concluded that entrepreneurial links could not cover their fixed costs. This scepticism is also seen in the work of Joskow and Tirole (e.g. Merchant Transmission Investment, CMI Working Paper 24, The Cambridge-MIT Institute, 2003). The Australian 2002 Parer Independent Review of Energy Market Directions (www.energymarket review.org) saw a possible role. Littlechild has been more supportive both in studies in Australia and Argentina (e.g. Littlechild, S. (2004) Regulated and Merchant Interconnectors in Australia: SNI and Murraylink Revisited, Applied Economics Department and The Cambridge-MIT Institute, Cambridge University, Cambridge Working Papers in Economics CWPE No. 0410 and CMI Working Paper 37; and Stephen C. Littlechild and Carlos J. Skerk (2004) Regulation of transmission expansion in Argentina CMI, Working Paper 61, University of Cambridge, Department of Applied Economics, 15 November).

No comments:

Post a Comment