Submission to the Senate Rural and Regional Affairs and Transport Committee Inquiry into the Wheat Export Marketing Bill 2008 and Wheat Export Marketing (Repeal and Consequential Amendments) Bill 2008

1. BACKGROUND TO THIS SUBMISSION

We are pleased to have the opportunity to make a submission to Senate Rural and Regional Affairs and Transport Committee Inquiry into the Wheat Export Marketing Bill 2008 and Wheat Export Marketing (Repeal and Consequential Amendments) Bill 2008, hereafter referred to as "the draft bills".

We are supportive of the deregulation of wheat export marketing. We have been an active participant in the wheat marketing debate for some years, and has consistently argued for the dismantling of the single desk. We therefore supports the intent of the draft bills. However, we are committed to full deregulation of the wheat export industry and note the draft bills fall short of this objective.

The following reports and opinion pieces, amongst others, are available on our website. They provide additional information if required.

- Backgrounder: The politics of wheat, March 2008

- "Wheat change is coming: time to help not hinder", February 2008

- "Cronyism buys into wheat sales", October 2007

- "Time for the single wheat desk to go", August 2007

- "Time for wheat to cut against the grain", May 2007

- "Ingrained prejudice", May 2007

- "The wheat monopoly bred arrogance before kickbacks", October 2006

2. THE DRAFT BILLS

While not the full deregulation found in other grain markets, the government's policy is a significant step towards full liberalisation of wheat export marketing. Potential exporters will apply for a license to export from Wheat Exports Australia (WEA). There will be no single bulk exporter. As a result, there will be no national pool by AWB. Also, there will be no legislated buyer of last resort since all wheat will be sold at a market price. This new legislation will therefore deliver the higher grain prices to growers forecast in many studies over many years.

The draft bills set up a potentially heavy-handed licensing scheme offering little benefit to growers. Additionally, the draft bills mandate infrastructure access undertakings by port facilities owners who apply to export wheat. This provision is likely to cause underinvestment in port facilities leading to increasing inefficiency and lack of international competitiveness over time.

Other features of the draft bills are positive and deserve support.

3. THE NEED FOR REFORM OF AUSTRALIAN WHEAT MARKETING

3.1. WHEAT IS A MAJOR EXPORT EARNER

Wheat is the dominant winter crop grown in Australia, in non-drought years wheat plantings are about 13.4 million hectares compared to 4.5 million hectares for barley and 1.3 million hectares for canola. On average Australia exports 75 percent of the wheat crop. Australia is the world's second largest wheat exporter. Major markets include China, Iraq, Indonesia, Japan, Korea and Egypt. In the last non-drought year, Australian wheat exports earned $3.591 billion.

3.2. GLOBAL DEMAND IS CHANGING

The Grains Research and Development Corporation (GRDC) has repeatedly drawn attention to increasing specialisation in international wheat markets and the need for Australian farmers to move away from producing traditional commodity varieties. Market research has also highlighted the strengthening North American competition in varieties traditionally dominated by Australia such as Udon noodle wheat.

Increasing competition and changes in demand suggest Australian wheat growers will be best served by increased specialisation and the development of new varieties for niche markets. The current national pool system is not conducive to innovation because wheat growers are another step away from their customers. All market signals are filtered through the single desk holder who may, or may not, adequately assess and predict market trends. As a result, the single desk system introduces an unnecessary additional level of risk into wheat marketing.

3.3. WHEAT IS INCREASINGLY PRODUCED BY LARGE GROWERS WHO WANT DEREGULATION

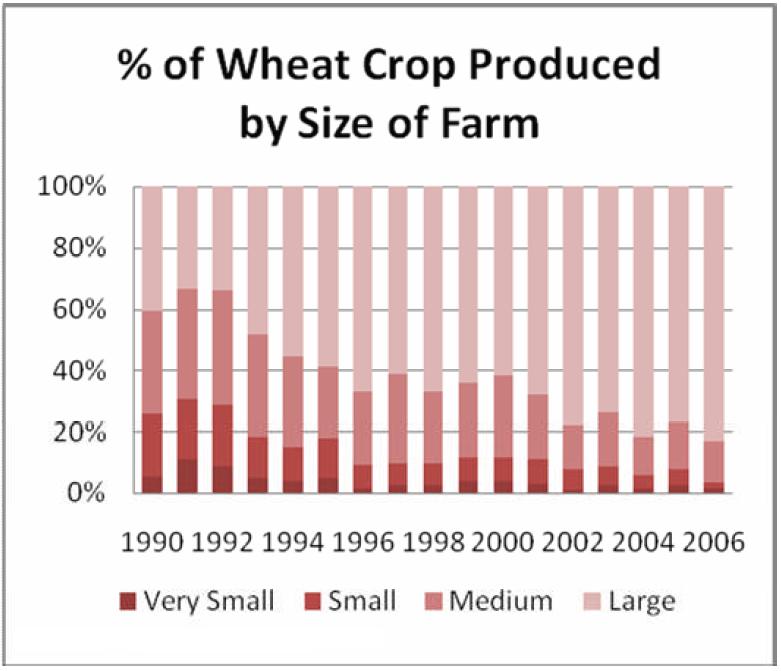

ABARE data shows over 80 percent of the national wheat crop is produced by large wheat growers and the proportion grown by the biggest farmers is continuing to increase (Figure 1 below). The Productivity Commission estimated only "ten percent of Australian farm businesses now produce over 50 percent of output". At the other end of the scale, small-scale wheat growers, who are particularly concentrated in NSW and Queensland, now only produce four percent of the wheat crop despite comprising one third of all wheat growers.

Western Australia is the largest wheat producing state despite having only 18 percent of wheat growers. The WA industry has undergone the largest degree of specialisation and concentration in recent years so that the average wheat-growing farm in WA is now 1½ times larger than in NSW and 2½ times larger than in Victoria.

Larger farmers have greater capacity to manage pricing risk through financial instruments such as forward contracts, futures and swaps. As a result, they are less reliant on pools. Perhaps one indication of the change in pool use is that now over 50 percent of wheat delivered to the national pool is by grain traders not farmers. Farmers are selling their wheat to domestic traders who on-sell it to the pool.

Organisations such as the PGA of WA and the Eastern Wheatgrowers Association who represent larger, specialist growers are pro-deregulation. They can see the benefits from being able to enter into highly vertically integrated contracts with overseas buyers for specialist varieties and from trading their own grain. Similarly, these growers are already experienced users of financial hedging instruments such as futures, options and swaps. The opening of the export grain market will reduce the risk of these instruments because Australian prices will trade more transparently in line with global prices allowing Australian growers to minimise basis (1) risk.

Figure 1 Source: ABARE

Source: ABARE

3.4. SINGLE DESK DELIVERS NO PRICE ADVANTAGE TO FARMERS

Not even the ITS Global study of 2006, funded by AWB, found any evidence of price premia being achieved for growers through the single desk. Estimates of the cost to growers of the current monopoly vary. A recent estimate by Graincorp of the costs to growers is between $9 and $15 per tonne in direct costs from inefficiencies in the entire wheat export chain. Additional costs will come from opportunities foregone by individual growers achieving spikes in spot pricing or better prices for specialist deliveries.

Moreover, there is a strong perception among international grain traders that the AWB has driven down grain prices through its aggressive chasing of market share. It is without dispute that the Cole Commission took as evidence a letter from AWB to the Iraqis selling wheat below international prices.

3.5. THE CURRENT LEGISLATIVE LIMBO IS THE WORST OF ALL WORLDS

Under the current legislative arrangements, the veto over wheat exports will transfer to the WEA on 1 July 2008. In theory, they will be able to issue export permits for specific markets and tonnages as occurs now. However, the WEA will be required to act in accordance with the interests of the national pool. The national pool is run by AWB and the existing legislation will still require this to occur. AWB has made it clear in its evidence to the Senate Standing Committee on Rural and Regional Affairs and Transport enquiry into wheat marketing that it cannot run a national pool without volume certainty.

It is logical that no operator can offer indicative prices for a pool without some idea of the quantity expected. Pool operators hedge the risk that wheat prices may be lower at harvest than quoted for the pool price by using futures and options. It is not possible to do this unless the operator has an idea of what the volume will be.

If the current legislative arrangements are allowed to stand, the WEA can only achieve the legislated objective of supporting the national pool by guaranteeing volume to the pool. The only way to do this is to restrict export permits and force growers to deliver to the pool through lack of alternatives. In practical terms the current legislation will force the WEA to deliver an effective veto back to AWB as the pool manager.

4. A REBUTTAL OF COMMON MISCONCEPTIONS ABOUT GRAIN MARKETING

4.1. THE SILO RECEIVER IS NEVER THE ONLY BUYER

Even for a farmer with no on-farm storage the local silo receivals centre is never the only buyer of wheat.

Furthermore, no farmer is forced to take the daily-posted local silo prices. Farmers can warehouse their wheat and usually have a period of approximately six weeks before they start paying storage fees or they can freight it (at additional cost) to other receivals points offering better prices. As a result, there is no reason for a farmer to receive below the prevailing world price on the day he or she chooses to sell.

If, on the day the wheat comes off the header and into the silo, the offered price is lower than the farmer will accept, he or she has a number of choices. First, the wheat can be warehoused waiting for the price to pick up, second, the wheat could be sold forward by some months or even years with the price received being the futures price that day less warehousing costs. In either case, there is no chance of futures losses or washout costs because the wheat is already in the silo. The decision will come down to whether the individual farmer has a view the price will pick up enough to compensate for the storage costs.

Moreover, the perceived monopoly of Graincorp on the Eastern Seaboard or CBH in the West ignores on-farm storage and domestic user storage such as feedlots. If storage costs at silos are too high, other silos or grain storage bags and bunkers will be built.

Proponents of the view that deregulating export wheat will in some way cause the grain accumulators to force farmers to accept below market prices assume farmers are unable to check the prevailing world price. This information is already delivered to any farmer who requests it from multiple vendors and in a variety of ways, including SMS, email and fax.

4.2. RECEIVER OF LAST RESORT HURTS GROWERS & IS REDUNDANT

Many farmers retain the mistaken impression that the national pool operator (AWB) is required to buy all wheat at pool prices. This is not the case. The national pool operator is required to receive all wheat delivered to it; however, there is no requirement to pay for it. In practice the national pool operator sells the wheat for whatever it can get and eventually (perhaps as long as 2 years later) pays the farmer.

In the past the market for poor quality wheat was very limited. Millers have no use for it and the domestic feedstock market was undeveloped. Changes to domestic demand mean feedlots will buy even shot and sprung wheat now. The farmer will not receive ASW pricing, however he or she would not have got that from AWB either and by selling to a buyer with a use for the wheat rather than delivering to someone who does not want it anyway, the farmer is likely to achieve a better price. The major difference will be growers will need to make a few phone calls rather than one to find a buyer.

In recent years, poor finishes to the season have resulted in large swathes of crops cut for hay. In the past, the traded hay market was localised and relatively limited. However, one of the results of the entry of relatively large, professional operators into the hay market has been the development of new domestic markets for hay. The market for poor quality wheat is similar to hay in that it is unplanned, undesirable and delivered to other farmers. There is no reason why specialist buyers of poor quality wheat will not emerge in the same way they have for hay.

4.3. POOLS WILL STILL EXIST ALONG WITH MANY MORE OPTIONS

ABB estimates over 80 percent of the barley produced in Australia is still delivered to pools despite the total deregulation of the domestic and export barley market. In a similar vein, there are already a number of regional wheat pools, such as that run by Southern Quality Produce in Victoria. AWB and other major grain buyers have indicated they will run regional pools. For farmers who prefer the cash flow structure of a pool many market participants have indicated these products will be available

One concern expressed by some is that regional pools can be closed at any time, leaving those farmers who harvest later or who have not committed at the time of delivery, unable to sell their wheat. These claims are misleading.

- The current AWB national pool is really a series of pools that open and close now. AWB, as pool manager takes a view as to the likely direction of grain prices and may close a pool if world prices start moving lower. The usual reason given by AWB is to protect the returns of growers who have already delivered to the pool. Therefore it is already the case that a national pool with a high estimated pool price can close at any time and be replaced by a national pool with a lower estimated pool price.

- The issue with pools closing is really one of farmers wanting multiple no-cost options available. Many of the farmers who gave evidence at the Senate Committee hearings on these draft bills said they did not deliver to the national pool last year (or the year before that) because better prices were available for domestic sales. Farmers deliver to the silo at harvest then wait to see whether the pool is a better option than a domestic sale. While there is a national pool this is a low risk option, the worst that can happen is the national pool reopens with a lower estimated return.

- The imminent demise of the national pool has already driven innovation. At least one pool for next harvest is already operating that allows a grower to insure for production risk. The grower can commit to the pool with certainty knowing if the crop fails, the maximum washout cost is $20 a tonne.

4.4. GRAIN TRADERS CANNOT DRIVE PRICES DOWN

A common, but completely erroneous, belief among single desk supporters is that multiple buyers will drive down prices. The logical absurdity of this position requires robust rebuttal.

At the moment, there is the situation of many sellers and a few buyers. The laws of supply and demand dictate that where there are many sellers (too much supply) and few buyers (insufficient demand) the price will be low.

In the future, the number of wheat buyer will increase. Already, even at the local silo level, buyers for the domestic market such as Glencore, Louis Dreyfus, Graincorp and ABB offer daily prices in each port zone to all comers with wheat that meets their specifications. In the future, these buyers for the domestic market may also buy for the export market so they will want higher tonnages and new export-only buyers will enter the market. The greater the number of buyers, the more they have to outbid each other to get the sellers to deal with them. Without collusion, which becomes impossible once there are more than a few participants, it is the buyers who compete to drive the price up not down.

Currently at harvest, supply increases to the point where there are many sellers but only one buyer, AWB. The buyers for the domestic market progressively fill their books and then offer prices below that of the pool. This is not "grain-traders driving down the price" but the simple operation of supply and demand. Once the domestic market is full, the only place grain traders can deliver their excess grain stocks is the pool so the pool price becomes the upper limit for grain prices. Far from claims the pool acts as a floor price, in a normal year the pool price is the ceiling price.

In a deregulated market, there is no limit on how much Australian grain can be exported. Grain traders can sell any grain they buy either domestically or internationally. They no longer have to deliver excess grain to the pool. The pool price acting as a ceiling is removed to the advantage of growers.

4.5. INTERNATIONAL BUYERS WILL PLAY THE GRAIN SELLERS OFF AGAINST EACH OTHER

Related to the wrong idea above that multiple buyers can somehow dampen prices, is the claim once these grain traders become sellers themselves and have to sell the wheat to the major international buyers then the single desk buyers will play the grain traders off against each other so that the wheat sells for a lower price.

Proponents of this view argue in this case there is only one buyer (insufficient demand) and many sellers (too much supply) so the laws of supply and demand will drive the price lower. But this is a misguided analysis that leaves out the total picture. No international buyer is the only buyer. Even the single desks of India, Iraq, and Pakistan etc. compete against each other in the international wheat market. So there is never only one buyer for a load of wheat. If a single buyer will not buy at the world price grain traders will find others who will.

4.6. LIKELIHOOD OF REPAYMENT NOT POOLS DRIVES BANK FINANCE

Many farmers borrow to plant their crop. With escalating fertiliser and chemical prices on the back of some very poor years, an increasing proportion of farmers will need to secure their borrowings against some surety before the banks will lend the money. In the past, some banks have relied on estimated national pool prices as the basis on which they budget projected returns. This has led to some to claim banks lend against the pool return yet this is not correct. Banks may use pool prices in their estimation of returns but the decision whether to advance borrowings is based on the overall financial viability of the farm. After all, even the best-projected prices are insufficient security if there is substantial production risk due to drought.

The Australian Bankers' Association has recently reiterated, "banks were keen to reassure grain growers that access to finance would not be impaired" by changes to wheat marketing arrangements.

5. SOME CONCERNS WITH THE DRAFT BILLS

5.1. LICENSING NOT TRANSPARENT & DISCOURAGES GROWER EXPORTING

In releasing the draft bills the minister, The Hon. Tony Burke said, "We want to have a regulated but competitive market which gives growers the opportunity to sell to reputable traders. This includes informing wheat farmers about the changes and ensuring appropriate checks and balances are in place to protect growers' interests." (2)

The proposed licensing system is the mechanism to identify reputable traders and protect growers' interests. However, as it now stands the licensing system is unlikely to achieve its objective. There are a number of unintended consequences likely to arise from the draft bills. In addition, the entire licensing system is contrary to the positive deregulation initiatives announced by Finance Minister the Hon. Lindsay Tanner and add needless costs.

5.1.1. Basis of assessment not transparent & discriminates against smaller operators

The most robust and transparent licensing system is one that operates from a publicly available set of criteria. Appropriate criteria may include financial probity and capacity to finance wheat exporting, export experience of agricultural bulk commodities and high standards of corporate governance. The draft bills require the WEA to have regard to these sorts of criteria but does not require the WEA to publish specific measures.

As it now stands, the WEA is required to "have regard to", 17 specified criteria, including the catch-all "such other matters (if any) as WEA considers relevant". There is no indication of whether all 17 criteria must be adhered to or how each criterion should be interpreted. The result of this is to create a large degree of unaccountable bureaucratic decision-making. Moreover, neither potentially accredited accompanies nor wheat growers have any way of assessing for themselves whether they think the interpretation is reasonable.

To take just two criteria as examples, the WEA is required to have regard to "the record in situations requiring trust and candour of each executive officer of the company". How is this provision to be interpreted? Business dealings, particularly at the executive level require high levels of trust and candour on a daily basis. Is the regulator meant to collect evidence, perhaps email traffic or board minutes, to determine the executive's record?

Similarly, the WEA must have regard to "the financial resources available to the company". This is unclear on a number of levels. Does it mean capacity to raise money? If the company is a publicly listed company, the financial resources available to it include the capacity to issue additional stock as well as debt. Or does the provision relate to retained earnings, a traditional definition of resources available to a company? Will the WEA require statements from accountants, bankers or auditors to evaluate this criterion? Clearly, this provision alone has the potential to add significant costs to exporters. It could stop smaller companies from undertaking the accreditation process.

5.1.2. Stops growers exporting their own grain

The accreditation process as it now stands makes it unlikely any single grower or group of growers could get accredited. While a single grower or a few neighbours could easily from an export company, it is difficult to imagine how such a company, with no trading history, could possibly meet the business record requirement. In the same way the financial resources assessment and risk management arrangements are unlikely to pass any meaningful test. Moreover, the point raised above in relation to the large costs the process could place on applicants is likely to preclude any small grower group from applying.

Hence, the draft bills set up a process that enables large companies, even those with no grain trading experience to become accredited but growers are effectively precluded from exporting their own grain. This is anomalous.

5.1.3. The licensing regime does not protect growers' interests

Growers need two things from wheat exporters, a large number of them to compete for the grower's grain and confidence they will receive payment for the grain delivered. The licensing system as it now stands delivers neither. As discussed above, the potential for the WEA to apply expensive and prescriptive licensing requirements will limit the number of accredited exporters hence reduce the pool of exporters buying grain from growers.

This legislation creates moral hazard because it gives the impression to growers that accredited companies are safe; after all the government has assessed them as sound and worthy of accreditation. Yet the legislation offers no guarantees against the possibly catastrophic result of grain markets moving in such a way to drive an exporter bankrupt, potentially overnight. Accredited companies could still fail and leave growers out of pocket but the very existence of the accreditation process gives growers a sense of security without actually providing any real protection. Instead, growers should assess for themselves who they think is a suitable grain buyer to do business with as they do already for other commodities and domestic wheat sales. Growers are not consumers in need of protection from the unscrupulous, but business men and women who can make their own commercial decisions and the draft bills should reflect this.

Recommendation: remove the 17 criteria for accreditation and replace with a requirement that the WEA licenses applicants who meet the single criterion of being a corporation under Australian law.

5.2. ACCESS TO PORT FACILITIES

The draft bills mandate an access regime for port infrastructure owners who also want to become accredited wheat exporters. The ostensible reason for this is to prevent port infrastructure owners from acting as monopolists to the disadvantage of potential competing exporters. The apparent fear embodied in the draft bills is that Graincorp, CBH and ABB will deny other exporters equal access to their bulk handling port facilities.

The creation of an access regime is flawed. Optimal infrastructure is provided when firms hold full control over their own investment decisions and can provide access at the most economically advantageous rate. The imposition of an access regime is by definition designed to force infrastructure owners to provide access at lower prices than would occur through voluntary contract. In the short term, this has the effect of lower costs for users and higher demand for services. However, over the longer term the effect is to stymie incentives for additional investment to either expand facilities or to upgrade them to achieve greater efficiencies.

The outcome in coal terminals is instructive where BHP's Hay Point facility is not subject to access undertakings while Dalrymple Bay and Port Waratah are:

Faced with an expansion of demand for coal in 2004 the BHP owned Hay Point facility saw an approval and commissioning of a 25 per cent increase in capacity in a little over 3 years.

By contrast, a comparable multiple-user regulated facility at Dalrymple Bay took an additional year, albeit with a larger planned capacity increase, as a result of argy-bargy and regulatory intercession over price.

Even greater delays are being experienced in expanding the facilities serving Port Waratah, the rail capacity to which has been increased following Commonwealth Government intervention. (3)

The bulk grain export facilities at Australia's ports are claimed by some to hold natural monopolies. Over the expected lifetime of such facilities, this assertion is unsupportable. Firstly, grain exporters always have the option to freight the grain to another port as growers do already. Secondly, as has been shown by the development of additional port capacity for coal and iron ore, new port facilities can always be constructed. In all cases, there is a price where the grain will be processed through a port facility.

Furthermore, it is in the commercial interest of port facility owners to maximise the throughput through their facilities. Port infrastructure is a volume business and port owners will price their facilities to ensure maximum throughput.

One of the more curious aspects of the access provisions in the draft bills is the key beneficiary of any access requirements will be AWB. The reason for this is as the current single desk holder AWB currently has the best-established international networks of buyers for Australian wheat. Until very recently, AWB by definition held a 100 percent share of Australian export wheat sales. Even with the small amount of export permits AWB is still dominant in export sales.

If AWB gets mandated access to port facilities at below commercial prices, it gains an advantage over its new exporting competitors. The port infrastructure owners must continue to bear the full cost of their facilities while the dominant exporter gets cheaper access. Far from encouraging competition, mandating access undertakings inhibits the capacity of port owners to compete.

Lastly, the proposed access provisions ignore current commercial realities. With one small exception, AWB does not control port facilities yet has successfully negotiated port access for decades. Port facility operators make their money from infrastructure utilisation and will continue to do so even if they begin to export wheat. Notably, the new permit export holders under the current export arrangements are not all infrastructure holders and they have been able to successfully negotiate access at mutually agreed prices.

Recommendation: Delete all reference to access requirements in the legislation and rely on the operation of the Trade Practices Act and contract law to regulate commercial disputes in relation to port access.

6. CONCLUSION

We will continue to support full liberalisation of Australia's wheat export marketing as in the clear best interest of both growers and the nation. However, these draft bills are a very positive step along that deregulatory path and the government is to be congratulated for bringing these reforms forward.

ENDNOTES

1. Basis is the difference between wheat prices in Australia and the global price with both prices expressed in the same currency. Basis exists due to supply and demand changes between domestic and international demand.

2. Press release 5 March 2008 "Draft wheat export marketing bill released today".

3. Richard J. Wood, 2007. "Economic regulation of transport facilities". Speech to Lloyd's List Events Conference, Melbourne, 6 June 2007

No comments:

Post a Comment