Address to the Energy Market Regulation Conference

Melbourne, 1 December 1999

PRIVATISATION

With the completion of the Victorian process, the hiatus in privatisation has been filled with events in other States. The blowtorch is on NSW and Queensland with the Financial Review being unkind enough to have assembled a table of losses caused by unwise decisions of bureaucrats and, in Queensland's case, subsidies. The losses run to $1.6 billion, three quarters of which are due to poor contracting by the state authorities.

The other action is in South Australia, where, perhaps partly because of losses by private and public sector businesses alike, the field for ETSA is thinning out faster than a Grand Prix race on a wet afternoon.

But it is the well-publicised losses, especially the Pacific Power/Powercor debacle, that has brought Treasurer Egan gingerly to once again unfurl his banner and re-enter the NSW privatisation debate.

PUBLIC OWNERSHIP AND REGULATORY NEUTRALITY

The Electricity Code, together with the Hilmer competition reforms, was largely written in an era when we kidded ourselves that the ownership structure -- private or public -- was irrelevant. Corporatisation was considered to offer all the advantages of private ownership while retaining the family silver. The adoption of a corporatisation model implied the need for clear commercial objectives, such as the requirement for acceptable rates of return, effective performance monitoring and competitive neutrality in input and product markets.

Part and parcel with this, at the heart of the competition policy reforms has been the requirement for a jurisdictional split between the government as regulator and the government as market operator.

While naked intervention to support a state business against private sector competition is not apparent, the outcome of the corporatisation approach has been mixed. The corporatised entities have certainly showed improved commercial orientation and have downsized and aligned their outputs better to the needs of the customer.

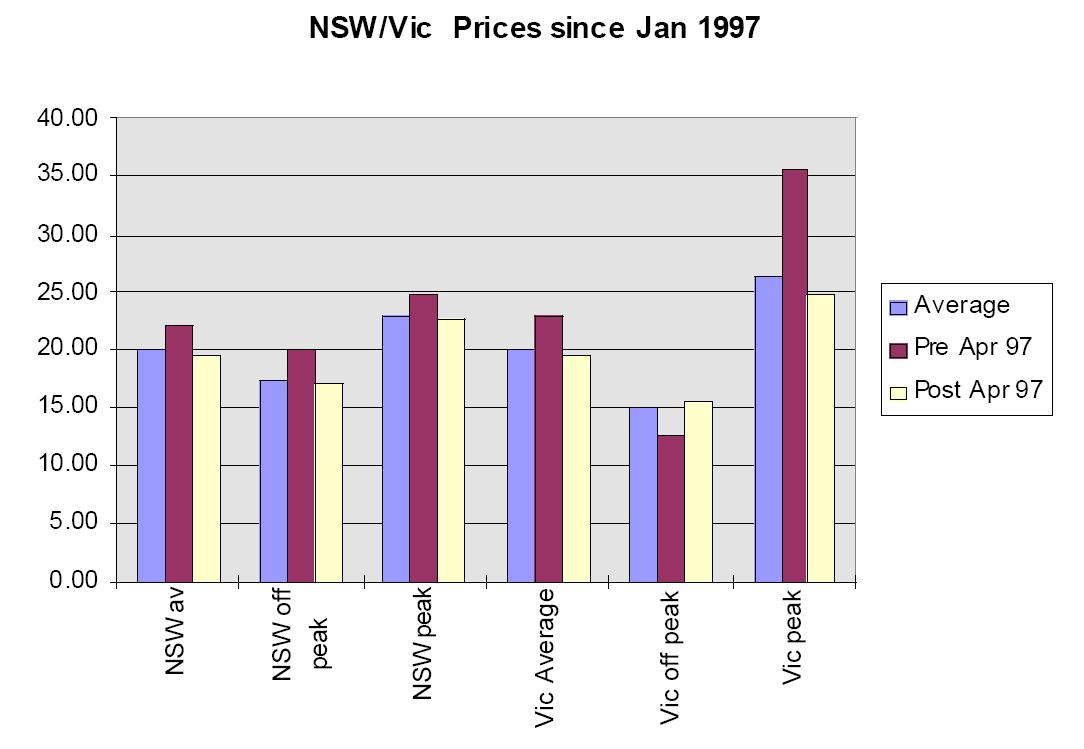

Market prices at some two thirds the new generation price levels have been one frustrating (to the generators) source of stability in the main NSW/Vic market.

The low prices are illustrated in the following chart.

The basic trends in these prices reflects the reality of an over-supplied market. The Victorian generators claim the state owned nature of the NSW generators causes them to bid on a market share rather than profit maximising fashion. There may be something in this but the overwhelming cause of the low prices is excess capacity. Whether that excess capacity would be more readily placed in cold storage by a private sector operator is a difficult question to answer.

The Victorian private sector generators have maintained that their publicly owned competitors in NSW are behaving uncommercially as a result of their ownership structure. They have also maintained that the NSW Government is recouped from the vesting contracts and the retail and distribution sector, and from the 0.55c/kwh levy on contestable customers. Even though the ACCC has now forced some reduction in NSW vesting prices, the reduction was rather less than expected and takes place with a delay that is a handy bonus to two year's profits.

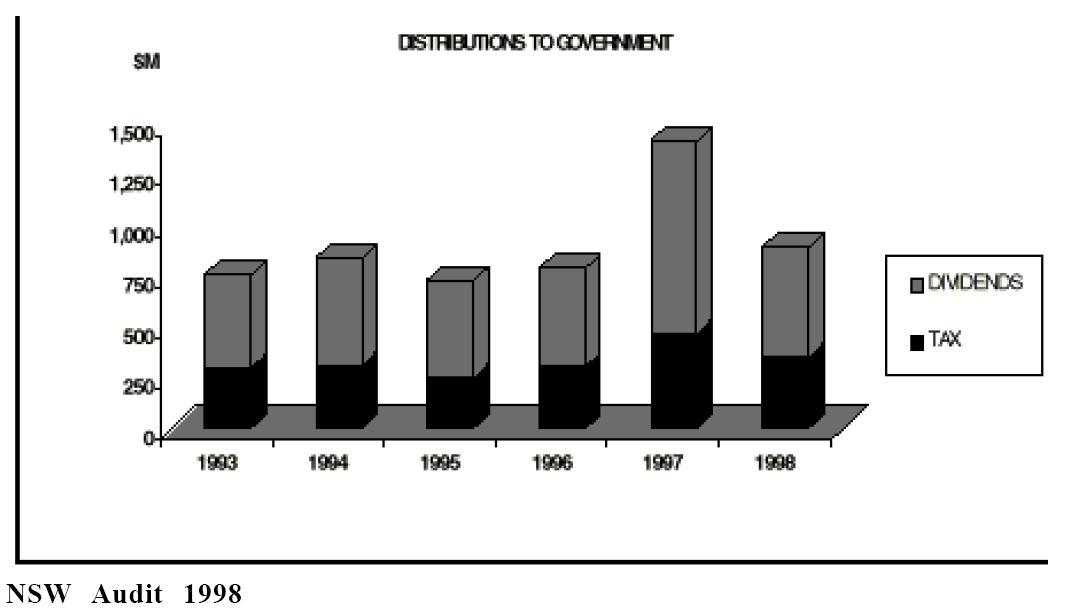

Overall payments of the NSW electricity industry to the Government have been maintained.

Distributors in Victoria, NSW and South Australia have produced solid profit performances on the basis of their regulated prices. Victorian generators have found themselves losing money as the price war has impacted on their heavy levels of debt. The NSW generators have been cushioned by being somewhat undercapitalised but nonetheless have found themselves in distress is evident from the Auditor's 1998 report.

The NSW Auditor in last year's report noted that the generators had shown a steady declining return on average equity from 15% to 10% to 3% in the three years to July 1998. In 1998, Macquarie and Delta had gross profits of around $55 million and Pacific Power about $44 million.

The 1999 results are not yet fully published -- only those of Delta were available at the time of writing. Delta's results, are quite outstanding. The business has increased its profits by almost 10%. This stands in contrast to its expectations of a profit decline from $55 million to less than $20 million. Macquarie also appears to have bettered last year's profits. Nonetheless, the NSW generators remain in trouble -- the settlement against Pacific Power is equivalent to $200-$300 million on most estimates, which would account for 5-6 years of profits!

In one important sense, the NSW Government has had some success in shielding itself from the adverse effects of the price war on its own revenues. But it has done so by grabbing back from the NSW consumer some of the benefits of that price war. And it remains the case that the dividends it receives from its investment are far less than those it would obtain from retiring debt. And, as the Pacific Power/Powecor result shows, existing dividend stream is far from secure.

IMPLICATIONS OF GOVERNMENT OWNERSHIP

Although corporatisation has proven to be an improvement on the structures presceding it, some of the deficiencies of the model are illustrated by the NSW performance. The deficiencies are:

- the temptation of the government to use the boards to reward faithful retainers. The worst example of this over the years has been the ABC. But in the electricity industry we saw some of the outcomes of this in NSW. The initial board of energyAustralia received a management endorsed consultancy study reportedly recommended a cut its workforce to 1,800 from 3,800 (which is already a reduction from 4,500). The response of the board of energyAustralia in rejecting the report and dismissing the CEO does not appear consistent with the hard-nosed commercial framework within which businesses should operate. Eventually, the NSW Treasurer replaced the energyAustralia board for this and other shortcomings

- The conflicts of interest the minister/shareholder has with the different competitive responses of the companies under his ultimate control and his duty to ensure the best possible return for his shareholders. Rob Lucas, the SA Treasurer relates the difficulties he faced as a shareholder to be told the plans of one of his generating businesses and subsequently to learn of similar plans by another and other action to mitigate the same problem by ETSA. Aside from the difficulty of confusing oneself with who had what plans and inadvertently revealing the commercial secrets of a competitor, the shareholder is in a dilemma: if he tries to prevent expenditure that would be unwise in view of the competitive environment he destroys the vertical and horizontal disaggregation on which the efficiency promoting competitive tensions are based.

- The minister as shareholder will often have a temptation to exercise influence on the business to promote a particular political line. I recall myself as a senior official in Victoria fronting one of the then corporatised businesses to persuade the CEO to allocate funds to burying some power lines. As an emissary of a shareholder minister, my remonstrations would clearly carry much more weight than those of a normal lobbyist. This is even more likely where, as in Queensland and, at least arguably in Western Australia, the Minister/shareholder is also the regulator.

- The attitude to risk will tend to schizophrenia. On the one hand the lack of a genuine shareholder and credit watchers may induce some adventurism on the part of the firms.

- There are criticisms that the NSW generators are less cautious about insuring against major risk events than private Victorian generators. Thus, if a VoLL of $25,000 were to occur, the loss of Macquarie assuming its 4640MW is 75% contracted at $30 is $521 million.

- Great Southern Energy is reputed to have paid nearly twice as much for Wagga gas offered by either AGL or other bidders.

- And it appears the government owned retailers and generators in NSW and Queensland have been unfortunate in their contracting.

On the other hand, Treasury owned firms are likely to have considerable oversight by Treasury officials of their strategic plans. Almost by definition this means excessive caution since the rewards for risk taking are not present.

BENEFITS OF PRIVATE OWNERSHIP

GENERAL ISSUES

All the evidence is that the provision of goods and services is more efficiently undertaken by privately owned businesses.

There are many reasons why this should be so. Not the least of these is the intrinsically greater flexibility of private sector bodies, motivated by the goal of maximising shareholder wealth, to adapt their products to shifting consumer needs and to pare unnecessary costs.

In competitive markets, commercial rivalry will force lower costs to be passed on in lower prices. Private firms that forego opportunities to reduce costs puts at risk their viability.

By contrast, Government owned businesses are able to survive without such a heavy focus on these costs because they do not face the threat of takeover by others able to spot and implement the opportunities for profit by making savings.

In addition, private ownership markedly reduces the risk of government interference in the terms and conditions under which goods and services are provided. This better allows the operation of the competitive market conditions that all states and territories have agreed to under CoAG.

Hence, while in principle there is no reason why private rather than public ownership should offer better outcomes to the consumer, the former is spurred more forcefully by profit considerations that require a very close customer focus. Private businesses flourish when they can establish and hold customer loyalty and avoid poor reputations. Indeed, the reform process in the Australian electricity industry was stimulated by observations of increased efficiency and lower costs observed in the mainly privately owned US industry and by the gains that were rapidly being seen in the newly privatised UK industry.

Measures that result in excessive costs being carried will fall on the customer.

The initial means of eliminating these excessive costs have been to transform the previous engineering based dispatch to one which embraces the total operations in a market and to require lower prices and efficiency gains by price regulation.

SPECIFIC IMPROVEMENTS ATTRIBUTABLE TO PRIVATE OWNERSHIP

In Victoria, prior to privatisation, resolute government action from 1990 resulted in considerable savings in costs and improvements in efficiency. Yet, in the period post privatisation of most of the businesses, further substantial improvements were brought about as a result of the focus on increasing shareholder value. As illustrated below, this cost reduction process had not been at the expense of customer service.

Distribution Service

In the case of distribution, outage time is a useful measure and the outcome has been mixed, depending on whether minutes off supply or number of outage occurrences are counted. On the ESAA data, using minutes off supply, outage time in Victoria has shown the most marked improvement and stands well below that of the other states.

Generation Service

Privatisation generally brings about a more coordinated meeting of demand at affordable costs. Generally speaking, the Australian ESI -- public and private -- has shown a marked improvement in recent years.

The normal measure of service in generation: availability to run, saw a particularly strong improvement in the corporatised Victorian system which has been maintained in the subsequently privatised system

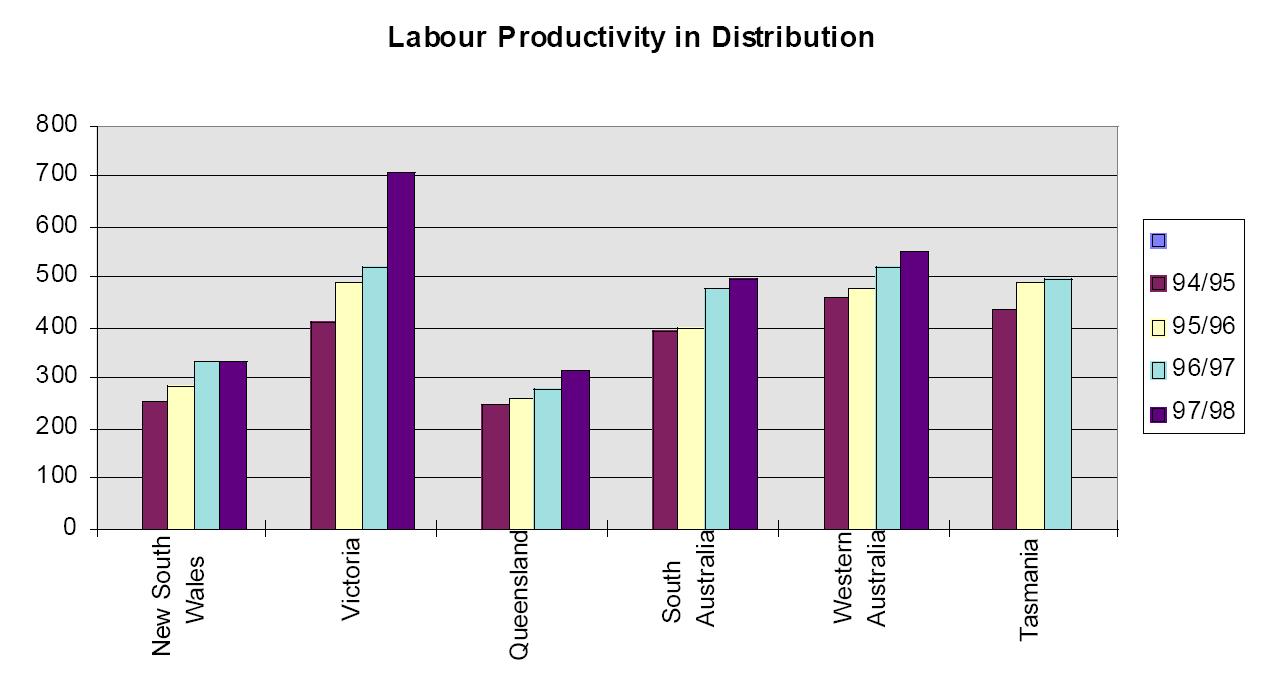

Generation Productivity

Labour productivity has generally improved across all states but the most marked improvements have been in Victoria (Tasmania's improvement on the data is partly due to the completion of the building program). Labour productivity has almost trebled in Victoria, with most of the big gains made prior to privatisation -- most in fact made during that ruthless labour-shedding administration of Joan Kirner!

Distribution Productivity

The really spectacular gains in distribution business productivity have been made under the privatised Victorian system. To some degree these figures are due to outsourcing, which has been more radical in Victoria but there are also businesses that have not markedly reduced their workforce, TUA being one, because they have diversified into synergistic areas (in TUA's case transmission construction).

Even the Kennett Government baulked at tackling the excess labour hoarding in the distribution sector and it was left to the new owners to achieve the rationalisation that the chart demonstrates. But since corporatisation, the NSW electricity businesses have also moved rapidly to reduce their staffing levels. Each of the six retail businesses has reduced its workforce by 10-25 per cent. Even so, it is the privatised Victorian system that has led the pack. Only as recently as 1994, Victorian manning levels were comparable to those of South and Western Australia but now are 20-30% lower.

As in generation, the rationalisation of labour was accompanied by an improvement in the normal measures of meeting consumer requirements. And from the publicly available information, it has also been accompanied by increased profits.

CONCLUDING COMMENTS

All the evidence is that privatisation and competitive markets together bring about major gains for consumers, shareholders and, where assets are sold by governments, the taxpayer.

Private ownership is preferable both because of its more concerted focus on profiting from consumer satisfaction, and because it removes the industry away from political direction. These conceptual advantages have been amply proven by the Victorian experience.

No comments:

Post a Comment