Address to the Conference

Competition & Regulation in the Energy Industry,

15 March 2002

SUMMARY

- Opening up electricity and gas markets to competition forces retailers to seek better ways of meeting the needs of customers more cheaply and ensures that cross subsidies are made known. The retailer is the agent of the customer and, in a competitive environment, must remain so to stay in business. This means the retailer must constantly research consumer wants and match these with power at the lowest costs and the required availabilities.

- Victoria has moved fastest among the Australian States but progress to a fully competitive market has been marred by Government price fixing.

- Such a fully competitive market is important to ensure costs are kept down in a sustainable way and product offerings are tailored to the needs of customers.

- With electricity, the absence of low cost interval meters is hampering the gains that rivalry for consumer demand could bring.

- Structural separation between retailing and distribution has taken place without distributors favouring their retail affiliates. Most of the private sector suppliers have voluntarily separated retailing and distribution into different corporate structures.

- All in all, comprehensive measures of Australian retail regulation shows it to be as well advanced as that for the leading North American jurisdictions.

MOVEMENTS TOWARDS FULL RETAIL COMPETITION (FRC)

Ostensibly, as shown in Table 1 shows, the movement to FRC in electricity and gas is encouraging.

Table 1: Planned Schedules to FRC

| Jurisdiction | Electricity | Gas |

| NSW | 1 Jan 2002 | 1 Jan 2002 |

| Victoria | 13 Jan 2002 | 1 Oct 2002 |

| ACT | Under review to be announced March 2002 | 1 Jan 2002 |

| SA | 1 Jan 2003 | 1 Sep 2002 |

| WA | 2005 | 1 July 2002 |

| NT | 2005 (subject to public benefit test) | n/a |

| Tasmania | 2007 | 2007 |

| QLD | No plans at this stage | Jan 2003 (subject to cost/benefit study) |

However the true picture is less sanguine. The actions of Australian Governments to date seems to indicate and extreme nervousness in liberating markets where there is a risk that prices may rise -- especially prices to smaller customers. And it's all very well to avoid the political brickbats in doing so but if this undermines the ability of the producers to profitably build new capacity and new transport links, the outcome is higher prices all round.

The fact is that gas and electricity are commodity markets and like other commodity markets the basic products are likely to fluctuate in price. Intermediaries between producer and consumer will smooth much of this, if allowed to operate properly, but will be frustrated if governments keep their hands on the levers.

This is most disappointingly observed in Victoria, even though Victoria has made the most energetic attempts to move into the world of competition.

In Victoria, as in other jurisdictions, successive tranches of retail customers have been freed to choose their own retailer. The process has progressed smoothly and been an integral part of the great improvement in efficiency and reduced prices that are evident in the State. Given this experience, there should be a strong presumption against regulated prices in the household sector. After all, energy retailing has no entry barriers and many capable providers are already in the market. With load profiling and FRC, any attempt by an incumbent retailer to raise prices above underlying costs would invite vigorous rival entry.

BENEFITS OF OPENING UP MARKETS TO COMPETITION

Net benefits are expected from opening markets by almost all analysts of the much maligned "economic rationalist" kind.

These analysts expect such benefits because market opening and unfettered competition forces suppliers to search out the lowest cost inputs and ensure the services they provide are carefully geared to the demands of the customer. To do otherwise will see suppliers losing customers and eventually being forced to leave the market.

That's why measures like the NSW ETEF, or other government regulations that prevent customers from shifting supplier find support with the lazy retailer who simply wants to sit back and avoid challenges. Such measures are often promoted by governments because the consumer loss is hidden -- no new player means nothing better is revealed and those customers being subsidised remain happily subsidised while the others are no wiser about how better off they could become.

But major cost savings are missed and we risk stifling entrepreneurship in retailing.

This is the classic case of government mandated stagnation. Suppliers are not forced to adapt to real needs of the customer. One outcome of such policies upstream in generation was that the long period of government monopoly among Australian supply industries left us with a surfeit of large and relatively inflexible base load plants and a shortage of peakers.

However, a case for temporary price controls can be mounted along the lines that the household sector is less well informed at the present time about the options and, having been protected by a government determined tariff for many decades, some safety net is justified. This was certainly the view taken in the UK and has been adopted for the household and 40-160 MWh customers in Victoria. It rests on a theoretical foundation somewhat akin to the provisions regarding consumer protection codified under Part V of the Trade Practices Act.

The possible price exploitation rests on consumer inertia. But unlike, say the banking industry, where there are real inconveniences to the customer changing retailer, in electricity and gas the process is straightforward and costless. Even so, many would argue that since the host retailer at "Day 1" has a monopoly of the current franchise customers, this could give rise to short-sighted opportunistic behaviour. (1) That said, it would surely need to be acknowledged that the underlying ability of the consumer to shift to any one of a great number of actual and potential alternative retailers, could never justify such oversight beyond a very short period.

There are clear dangers in overriding the forces of competition, dangers that intensify with the length of time the controls remain. These dangers can be distilled into two primary failings related to where the regulator sets the controlled price too low. Setting prices too low will:

- require cross subsidies and either bring an unravelling of the market balance and/or lead to financial distress among retailers and inadequate incentives for new investment; an extreme outcome of these developments is evidenced in California; and

- crowd out the competitive provision that is being sought forcing (reluctant) host retailers to continue serving unprofitable customers.

These considerations underline one matter on which pricing controls or guidelines must be firmly ruled out, that is the prevention of price increases on the grounds that consumers would prefer not to pay higher prices. Already in Victoria we have put prices in place that have been regulated over the past six years with little provision having been made for the changing costs -- absolute and relative -- on which the prices were first justified. Unless prices are allowed to adjust to the underlying cost shifts, retailing will be seriously harmed and the consumer is the eventual loser.

In this respect, Victoria's most recent decision placed a 3% upper limit on the deviation from the average price allowed of the maximum price for individual customer classes This cements-in distortions, making it easier for new retailers to avoid those customer classes whose tariffs have become highly unprofitable. The danger is that the host retailers will gradually be left servicing the highest cost customers.

In addition, and of more immediate concern to the retailers, the Government put ceilings on the average price increases. Rising energy costs in Victoria led electricity retailers to seek average price increases of between 15 and 21 per cent. On the advice of the Essential Services Commission, the Government pared these back to between 2.5 and 15.5 per cent.

It may be that the Government would wish to shield some consumers from the true market price. If so, there are well-established means of doing so. Requiring cross subsidies from other consumers of the product is not one of these.

The preferred approach is direct provision of support to targeted customers through CSOs and the decisions on the increased prices to the rural customers went some way towards this, with subsidies paid direct to those users. This aside, the upshot of the price restraints is that there has been little incentive for retailers to seek out new customers. In Victoria, after two months of FRC only 3,000 small customers have switched retailer (but even this is fifteen fold the level of NSW). To get to the UK benchmark of 38% of the market switching after 3 years would need upwards of three quarters of a million in Victoria and over a million in NSW.

Compared to setting the price too low, the dangers of allowing excessive prices are considerably less. This is not the least because excessive prices bring their own remedy -- competitors find ways of winning the ostensibly captive markets. The Productivity Commission draft report on Part IIIA of the Trade Practices Act drew attention to this asymmetry in the context of "essential services" and advocated erring on the side of allowing a higher price rather than risking an excessively low price. These approaches are even more appropriate in retailing which does not have the long lived capital assets of network services and consequent ability temporarily to serve customers at marginal cost.

POSSIBLE FACTORS IMPEDING THE PROGRESS TO FRC

ENERGY RETAILING AND DISTRIBUTION GOVERNANCE

Monopoly and vertical integration are often associated with impediments to competition.

Structural separation of the former Victorian electricity monopoly left the retailing and distribution businesses as jointly owned. The two arms were required to observe a strict structural separation in the form of a ring fence. Two of the five businesses have since made ownership separations while two others have formed distinct businesses. Similarly, South Australia has a corporate split between AGL and CKI/ETSA.

With gas, the separation is total in Victoria with retailers and lines owned by separate businesses though TXU has common ownership. Other states also have separate companies owning gas retailing and distribution; in NSW, AGL dominates with two separate companies; in South Australia Origin has the retail with AGL and the pipes are owned by Envestra. Envestra also owns half the pipelines in Queensland where Origin is the retailing arm, whilst Energex owns the other half both as a retailer and distributor. Table 2 summarizes this.

Table 2: Gas Distribution and Retailing

| Distribution | Retail | |

| Victoria | Westar TXU Stratus Envestra Multinet (United) | Kinetik TXU Origin Pulse (United) |

| NSW | AGL Networks Ltd Envestra | AGL Retail/wholesal/ltd Origin Great Southern Energy Integral |

| Queensland | Energex Envestra | Energex Origin |

| South Australia | Envestra | Origin AGL |

Neither the gas nor the electricity market is an oligopoly: the energetic steps already being taken by retailers to attract customers in unregulated energy markets are evidence of this.

Procedures are in place to effect a speedy and costless transfer of a customer from its host retailer to another that is able to offer a superior price.

The notion that the incumbents are able to exploit their current monopoly is not plausible in the Victorian retailing situation. Hence, even if there were no Trade Practices Act as an insurance for consumers, the case for regulation either to combat monopolistic pricing or promote competition is extremely slender. Indeed, the downside rests with regulatory not market failure. There is no evidence that host distributors have favoured their retailing arms and most privately owned suppliers have seen virtue in separation. However, some may find economies in retaining the two tasks within a single corporate structure and we should not require costs be needlessly incurred by demanding corporate disaggregation.

METERING

An issue of considerable contention in Australia and overseas is the lack of demand side response within the electricity market. It is said that there are only a few hundred MW of demand in the SA/Vic market that can be controlled. This is a very small share of the market. Clearly one reason for firms not wanting to negotiate demand side contracts is that, smelters excluded, energy only constitutes 2-10% of costs and downing tools is more expensive than making a small saving.

In the case of households the lack of interval metering is a major factor. Indeed, this lack and the consequent need for load profiling has a perverse effect. Retailers would find those households who are the heaviest users to be the most attractive targets, notwithstanding that such households typically use air conditioning which has been a major factor in bringing greater peakiness and hence higher costs.

A debate which divides retailers, consumerists and economists is what to do about the lack of metering. It all comes down to price of the meters and costs of reading them. But according to McKinseys, (2) household users exhibited considerable demand elasticity in a Texan study. Without specifying the price changes involved, the study claims that an experiment with "dynamic pricing" through real time metering brought consumers to shift one third of their load out of peak periods.

Such a magnitude could vastly increase the savings from electricity markets and the importance of retailers in achieving these. The issue remains the cost of roll-outs. One firm, Email, is discussing a $60 meter if the volume is 400,000. But this would seem to need additional expenditures for the meter to be a tool that can offer genuinely controllable usage. The fact remains that notwithstanding all the potential gains and talk of mass roll-outs of interval meters nobody has yet done it.

MARKET LIQUIDITY

One feature of government controls, and a manifestation of their effect in preventing competition is the dampening effect this has on the development of alternative financial instruments. Such instruments like swaps, caps and a whole host of exotic names develop in response to the need to defray risk. That said, these derivatives are no different from the now ancient notion of futures to which Shakespeare gave such a bad name in The Merchant of Venice.

Bad name or not, it is to the mutual advantage of buyers and sellers to obtain greater certainty of expenditures and revenues. This allows them to plan ahead without the innovatory-sapping and potentially financially devastating effect of government control.

There have been claims that the Victorian market has been short on liquidity. The force of such claims was particularly strong in the period leading up to what was expected to be a tight supply/demand situation during the present summer months. Lack of liquidity is more likely to occur where there are only few suppliers or customers. The relatively isolated markets in Australia always will run such risks.

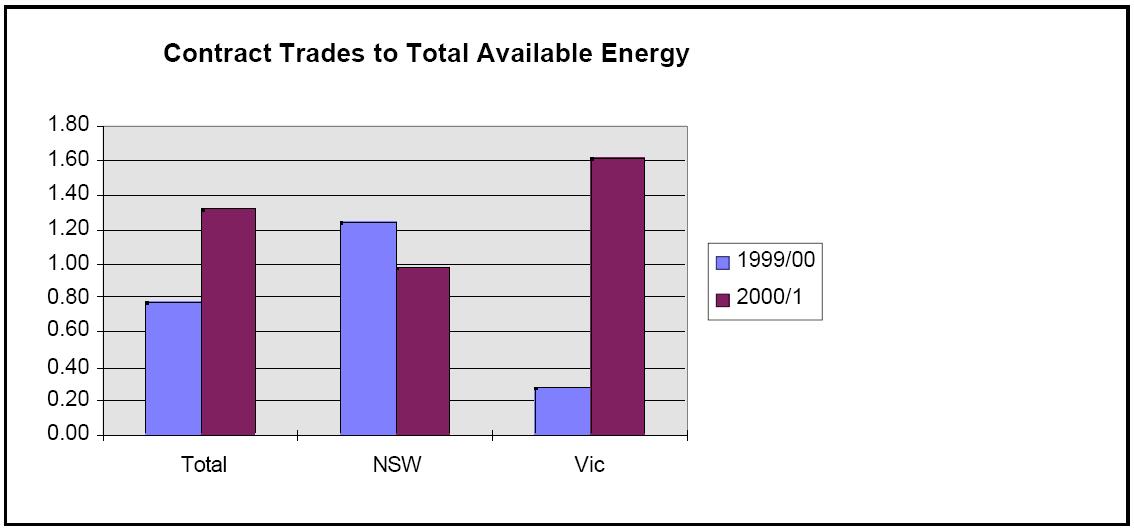

Whatever the merits of the claims for Victoria -- and any retailer that was undercontracted has in the event been fortunate -- there is a very rapid growth in derivative or futures contracts. The Over-The-Counter data published by AFMA indicates a very strong growth in liquidity -- over 50% last year for the market as a whole. Chart 1 illustrates this.

Chart 1

The other notable feature of Chart 1 is that in relation to the energy market, the turnover of contracts in NSW declined last year while that of Victoria increased fivefold. Victorian retailers and generators were seeking out ways of defraying their risks but in NSW there was far less need to do so because the Government has mandated a form of insurance through ETEF.

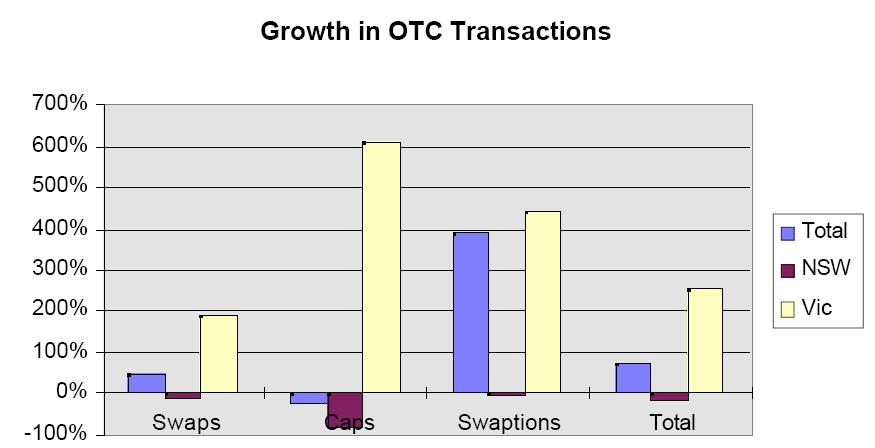

Particularly strong growth was recorded in swaptions, an instrument that gives retailers to pursue business opportunities without being locked into energy. In contract numbers, swaptions in Victoria increased fourfold while in NSW they decreased. This is a most significant feature since an instrument like this gives marketers an opportunity, at low cost, to seek new custom secure in the knowledge that they have contract coverage in the event that they are successful. Chart 2 shows the changing demand of different derivatives.

Chart 2

The compulsory insurance scheme ETEF is clearly the main reason for the difference between NSW and Victoria. In NSW this is stunting the growth in the market and denying consumers the best deals.

AUSTRALIA ENERGY MARKET LIBERALISATION

AGAINST THAT OF OTHER COUNTRIES

A number of analyses attempt to grade different jurisdictions according to a range of 22 criteria including:

- Is there a detailed plan enabling consumer choice?

- how much of the market is open to competitors?

- what percent of customers have actually switched?

- Is there separation of distribution and retailing to prevent favouring affiliates?

- Is the generation structure privately owned and disaggregated from retailing?

- Is network pricing cost based?

- Is gas and electricity policy linked?

One in the US by CAEM ranks Pennsylvania, Texas and New York as the most liberal (though New York has a peculiar wholesale market whereby the jurisdictional regulator can override the supplier's bid price in real time -- a contingency which seems to be highly intrusive). Table 3 reproduces the CAEM rating of the US states.

Table 3: US Ratings by Market Liberalisation

| Pennsylvania | 66 |

| Texas | 65 |

| New York | 64 |

| Maine | 62 |

| DC | 56 |

| Maryland | 56 |

| New Jersey | 47 |

| Arizona | 47 |

| Virginia | 45 |

| Illinois | 45 |

| Montana | 44 |

| Connecticut | 43 |

| Michigan | 42 |

| Massachusetts | 41 |

| Ohio | 39 |

| Rhode Island | 36 |

| California | 34 |

| Oklahoma | 0 |

| South Carolina | 0 |

| South Dakota | 0 |

| Tennessee | 0 |

| Utah | 0 |

| Wisconsin | 0 |

| Wyoming | 0 |

| Nebraska | -8 |

| Colorado | -8 |

| Idaho | -8 |

| Alabama | -8 |

| Louisiana | -8 |

| Minnesota | -8 |

| Mississippi | -8 |

The Canadian Province of Alberta scores slightly higher than any of the American States, though Ontario scores poorly and the other provinces are down with the US Good Ol' Boys and farming states.

Within Australia, my own estimates (3) (see Appendix) are that Victoria would be close to the levels of liberalisation of the leading US states and that NSW would also get close to this except for one blemish (in the CAEM eyes, though a Blue Ribbon to some) namely the lack of privatisation. In fact NSW actually rates just above California! This though turns on the degree to which the FRC s are bringing true market openings and there has to be doubt with regard to Victoria and considerable scepticism with regard to NSW.

A similar study in Europe, commissioned by the British and Dutch Governments and undertaken by the Oxford University group OXERA found the UK and Norwegian markets were most liberalised and that of France the least. That too developed its measures in response to examinations of market share, barriers to entry and the switching and price impacts of liberalisation.

The indicators still show Australia to be ahead of most other jurisdictions in electricity and gas reform but our position can easily be punctured. Of course, there is some inevitable arbitrariness in these league table measures. Remember, only two years ago, California was harnessed with Pennsylvania, New Jersey, Maryland in the van of reforming states in the US!! Even so, measures like these are useful in placing pressure on jurisdictions to move in the right general direction.

APPENDIX

APPLICATION TO AUSTRALIA OF US LIBERALISATION CRITERIA

| Attribute | Jurisdiction | Score | Notes |

| 1 | Qld | -10 | adopted for users over 200MWh/pa; rejected for smaller users |

| NSW | 10 | adopted for all; market fully open from 1 Jan 2002, with some constraints | |

| Vic | 10 | adopted for all; market fully open from early 2002, with some constraints | |

| 2 | Qld | 3 | actual percentage not obtainable, but some customers contestable (clearly less than 50%) |

| NSW | 10 | all customers contestable | |

| Vic | 10 | all customers contestable from early 2002 | |

| 3 | Qld | 0 (customers) 1 (load) | 10 percent contestable customers have switched (source: report on costs and benefits of FRC). This is <1% customers and about 10% load |

| NSW | 0 (Customers) 2 (load) | about 20% of contestable business customers switched no household | |

| Vic | 0 (Customers) 5 (Load) | about 28% of contestable business customers switched few household | |

| 4 | Qld | 7 | corporate separation with codes of conduct; legal separation of distribution/retailing under Elect Reg 94; financial and accounting separation under NEC |

| NSW | 3 | financial and accounting separation under NEC; draft paper on ring-fencing proposes legal separation and conduct rules | |

| Vic | 3 | financial and accounting separation under NEC; position paper on ring-fencing does not propose legal separation but proposes conduct rules | |

| 5 | Qld | 2 | |

| NSW | 2 | Qld, NSW, Vic part of national market with some interstate connectors but with different rules on full retail contestability and different market reconciliation IT systems | |

| Vic | 2 | ||

| 6 | Qld | 10 | retailer sends consolidated bill including TUOS and DUOS |

| NSW | 10 | as above | |

| Vic | 10 | as above | |

| 7 | Qld | 10 | NEC permits any person to apply for registration as a metering provider: clause 7.4.2 |

| NSW | 10 | NEC permits any person to apply for registration as a metering provider: clause 7.4.2 | |

| Vic | 10 | NEC permits any person to apply for registration as a metering provider: clause 7.4.2 | |

| 8 | Qld | -10 | generation mostly public (>90%) |

| NSW | -10 | generation mostly public (>95%) | |

| Vic | 10 | generation privatised | |

| 9 | Qld | 3 | permits bilateral and these comprise >95% of sales. This accompanied by mandatory "gross" pool |

| NSW | 5 | as above | |

| Vic | 5 | as above | |

| 10 | Qld | 10 | not an issue |

| NSW | 10 | not an issue | |

| Vic | 10 | not an issue | |

| 11 | Qld | 10 | not an issue |

| NSW | 10 | not an issue | |

| Vic | 10 | not an issue | |

| 12 | Qld | 5 | national privacy legislation forbids release of information without affirmative customer consent |

| NSW | 5 | as above | |

| Vic | 5 | as above | |

| 13 | Qld | 0 | Household Retail Competition rejected |

| NSW | 5 | brochures | |

| Vic | 10 | benchmarking studies, brochures, list of suppliers, customer charters, advice to large users on how to tender arrangements | |

| 14 | Qld | -5 | Household Retail Competition rejected |

| NSW | -5 | incumbent is the default, no requirement to switch | |

| Vic | -5 | incumbent is the default, no requirement to switch | |

| 15 | Qld | 5 | |

| NSW | 5 | Regulator regulates tariffs for default customers | |

| Vic | 5 | Default provider must publish intention to change tariffs two months in advance | |

| 16 | Qld | 5 | |

| NSW | 5 | ||

| Vic | 5 | ||

| 17 | Qld | 10 | Regulators given discretion under National Electricity Code to adopt price caps or other incentive-based forms of regulation. Qld has revenue cap, cost of service approach |

| NSW | 10 | NSW has revenue cap, cost of service approach. Distribution companies consider they have been short-changed | |

| Vic | 10 | Vic has weak service incentive scheme. Distribution companies appealed latest decision but lost | |

| 18 | Qld | 2 | distance and congestion related transmission pricing. Very limited real time pricing at retail level (eg economy and super economy plans -- tariffs 31 and 33) |

| NSW | 4 | Differentials to reflect distance | |

| Vic | 4 | as above | |

| 19 | Qld | 5 | NEC permits distribution generation interconnection to grid. Some critics have raised questions over adequacy of prices paid to such generators |

| NSW | 5 | as above | |

| Vic | 5 | as above | |

| 20 | Qld | 0 | some regulatory commentary on issue of convergence. Little concrete action. |

| NSW | 5 | Integrated decision making | |

| Vic | 5 | as above | |

| 21 | Qld | 10 | Commission now totally changed from regulatory model |

| NSW | 5 | Elements of monopoly power purchase remain | |

| Vic | 10 | Commission now totally changed from regulatory model | |

| 22 | Qld | 0 | Government allocation increased from $5.16 million in 2000 financial year to $5.68 million in 2001 financial year |

| NSW | 10 | Government allocation increased from $5.648 million in 2000 financial year to $7.038 million in 2001 financial year | |

| Vic | 10 | Government allocation increased from $7.9 million in 1999 financial year to $12.9 million in 2000 financial year |

CAEM ATTRIBUTE DESCRIPTION AND SCORING

Issue: Has the PST adopted a general policy favoring retail electricity restructuring or customer choice either by legislation or by commission order? If yes, has the public utility commission or board also established a detailed plan enabling customer choice? Conversely, has the PST explicitly rejected retail competition?

Weighting: 8%

Issue: How much of the market is open to competitors?

Weighting: 5%

Issue: What percentage of the PST's electric customers have actually switched from the traditional utility's service to the services of a different supplier?

Weighting: 10%

Issue: Has the PST adopted rules that prevent utilities from using market power over distribution facilities to favor their competitive functions (provided by either the utility or its affiliate)?

Weighting: 10%

Issue: Has the PST adopted uniform business practices for all utilities in their jurisdiction? Has the PST agreed to implement uniform business practices in concert with other PSTs?

Weighting: 10%

Issue: Which billing method has the PST adopted? Does the utility send both its own and another provider's bill, or are bills for both services sent by the marketer? Or does each company send its own bill?

Weighting: 3%

Issue: Does the PST allow metering to be a competitive service provided by a third party?

Weighting: 3%

Issue: What market structure has the PST adopted for electric generation?

Weighting: 10%

Issue: Does the PST require bilateral contracts or a pool structure for wholesale electric transactions?

Weighting: 5%

Issue: How does the PST determine the amount of stranded costs that a utility will be permitted to recover?

Weighting: 3%

Issue: How does the PST permit utilities to recover stranded costs?

Weighting: 3%

Issue: Is customer information available to marketers in a manner that facilitates competition among service providers? What arrangements are made between the utility, other retail providers, and the customers to facilitate the identification of customers, their usage, and their location?

Weighting: 3%

Issue: Does the commission administer a mass-media consumer education program as part of its restructuring efforts? If yes, does the commission evaluate the program for customer awareness and understanding of how to select a retail electric supplier?

Weighting: 3%

Issue: Has the PST mandated a regulated option (default service) for customers who do not choose a competitive supplier, or are consumers required to choose a competitive supplier (or assigned to one)? If such a default provider is mandated, must the utility be the default provider or can a nonutility company bid to be the default provider?

Weighting: 3%

Issue: If a default provider exists, is it required to sell at a firm price, is there provision for an adjustment after the fact, or is there a volatility passthrough provision?

Weighting: 3%

Issue: If a default provider exists, how is the default rate established?

Weighting: 3%

Issue: Has the PST adopted performance-based pricing for distribution facilities?

Weighting: 3%

Issue: Has the commission adopted efficient pricing reforms for network assets?

Weighting: 3%

Issue: Has the PST adopted policies to facilitate interconnection of distributed generation to the grid?

Weighting: 3%

Issue: Does the PST link the restructuring of its electric market to the restructuring of its gas market?

Weighting: 2%

Issue: Has the PST comprehensively reformed its internal organization, practices, procedures, and processes to take into account the changing dynamics of regulation in moving from a monopoly model to a customer choice mode?

Weighting: 2%

Issue: Is the funding adequate for the PST commission or board to perform its traditional regulatory responsibilities, in addition to new obligations resulting from the transition to customer choice?

Weighting: 2%

ENDNOTES

1. In fact the so-called Cournot model of oligopolistic competition predicts that the markup of a supplier depends not only on demand elasticity but also on the supplier's share of market output. The larger the share, the more market power a supplier has and the greater its markup.

2. Power by the Minute, February 2002 http://www.mckinseyquarterly.com/article_abstract.asp?tk=83967:1142:8&ar=1142&L2=8&L3=48

3. Jennifer Hocking and Michelle Tandy greatly assisted in preparing this assessment.

No comments:

Post a Comment