Submission

INTRODUCTION

We are pleased to offer its advice to IPART in this submission.

For over six years, we have been an advocate of reduced government intervention in markets. Competitive markets with secure and privately owned property rights have proven to be the only guarantors of low prices and entrepreneurial advance across the spectrum of industries in Australia and worldwide.

NSW has a retail and generation market that is potentially rivalrous. Political impediments have unfortunately prevented the NSW Government from adding private ownership to this market framework. We believe this has detracted from the commerciality of the NSW industry and is having a progressively debilitating effect on the various businesses in terms of their corporate development. Moreover, in spite of the best intentions of the government, its ownership of the industry inevitably leads it to intervene in commercial decisions in ways that will eventually prove harmful.

In this respect, public ownership of the industry has offered increased opportunity for the government to introduce the Electricity Tariff Equalisation Fund (ETEF). This dominates the market structure in NSW. It sets a government determined price for small customer's energy (about half the market), with the generators and retailers compensating each other when the wholesale price deviates from that specified level.

A review of the ETEF arrangements goes beyond the terms of reference of the Review of Regulated Retail Tariffs that the Minister for Energy has sought from IPART. Nonetheless, these wider issues are germane to two matters on which the Minister has sought advice, namely "an appropriate retail margin" and his requirement that the Tribunal take account of "arrangements for the recovery of all reasonable full retail competition costs".

THE ROLE OF THE RETAILER

While we have no special expertise on the precise level of prices that would prevail in a truly competitive market in NSW, we have firm views on the role of the retailer in competitive markets. In many markets the retailer enjoys the most slender of margins -- in grocery supermarkets a profit margin of perhaps only 1-2 percent -- but even so the retailer is a crucial link between the manufacturer or primary producer and the customer. The retailer, in competitive markets, is the agent of the customer, not out of any benign camaraderie but because the alternative is that customers are lost and bankruptcy looms. To ensure its continued profitable existence the retailer must be constantly on the look-out for different consumer requirements and must ensure its own service costs are constantly pared back.

This process of competition is now generally accepted as offering the best means of setting the price and quality mix that gives consumers the best value. It operates in both the static sense of bringing about the lowest cost outcomes for a given set of demand and supply configurations, and in the dynamic sense of encouraging a ceaseless search for improving upon this in the light of shifting demands and input costs.

All regulatory bodies claim that they are seeking to replicate this competitive outcome in the context of a market in which there are some natural monopoly elements that require synthetic costs to be developed. No reputable authority would nowadays claim, outside of specific circumstances, that regulatory overrides offer superior outcomes to those of a free and competitive market. Regulators simply do not have the capability to assemble and process the information that profit-driven suppliers routinely undertake.

A regulatory role is reserved for where there is natural monopoly or important unpriced spill-overs from an activity (neither of which occur with electricity retailing) or under certain limited circumstances where the market might provide inadequate information for customers to take informed choices. Normally the favoured regulatory response in such circumstances is to insist upon providers supplying more information than they would otherwise provide or for the authorities themselves to supplement the market provision of information.

RETAIL REGULATION

Ostensibly because of informational issues, most jurisdictions on moving to a disaggregated electricity system have also introduced a phasing system with vesting contracts at a specified price. The current NSW arrangements have also been undertaken to allow a smooth transition to genuine markets. IPART recognises that it would be poor public policy to use such a mechanism to depress the price below that which would prevail under competitive conditions.

But contracts specified by the government are clearly an anathema to a market where the parties seek out their own deals and in doing so bring about the optimal level of demand and supply. With the price fixed for half of the NSW market, the signals that allow this to take place are severely muted. There is no "appropriate" retail margin because the risks have been taken out of the business and assumed by the taxpayer. Similarly, if the government sets the price and requires the participants to buy and sell at that price, this brings no incentive to the retailer to seek out new needs nor for the generator to set up new capacity, especially new capacity that will operate only occasionally and therefore requires a high price. Taken over the longer term these features are likely to mean an industry that does not correspond to market needs and is vulnerable to supply failure.

Hence, ETEF and its associated retail regulation is likely to have a most damaging effect on the long-term health of the NSW industry and deny the NSW consumer benefits in terms of sustainable lower prices. While there is considerable merit in short term measures phasing in of competitive conditions that allow markets to adjust to changes in arrangements that have prevailed for many decades, those measures must be swiftly phased out. Maintaining this regulatory environment over a period of several years will prevent the supply side developments that provide the only guarantee of an industry constantly seeking out changed consumer needs and finding ways to respond to them.

In short, the regulatory narcotic will need to be administered in constant, and perhaps increasing, doses to maintain the patient's basic functionality unless measures are taken to ween it off the drug.

RETAIL OPERATING MARGINS

The price setting for retail margins has proven to be highly controversial. The Victorian Government's decision on standing prices for below 160 MWh customers has produced levels of competitive activity below that expected in a full retail competition environment. Only about 4,000 households have switched retailer and the marketing activity of host retailers has been subdued, while the decision prompted the owner of one retailer to announce that it is seeking a buyer.

Table 1 summarizes some recent data on retail margins. IPART will need to judge how meaningful such comparisons are.

Table 1

| Average ($/Customer) | Range ($/customer) | |

| Europe (DataMonitor) | 73 | 50-95 |

| Australia (IPART, ACTEW, Aurora) | 75 | 40-116 |

| United Kingdom (OFGEM) | 108 | 100-117 |

| Victoria (ORG) | 65 | 50-80 |

Sources: Origin Energy; ORG

One indication of the openness of a market that has price restrictions in place is to examine customer churn rates. Low rates of churn are indicative of low incentives for competitors to seek customers and this in turn indicates that prices are being held too low. The result is the market is failing to achieve the level of competition required to create the optimal price/quality mix for customers.

In this respect, after nearly three months, the number of household customers that have shifted from their host retailer in NSW amounts to only a few hundred. The UK now has a level of churn for both gas and electricity of about 38 per cent, a level that has prompted the regulator to lift all price restraints. To get to the UK benchmark of 38% of the market switching after 3 years would need upwards of a million customers in NSW to switch.

IMPACT OF GOVERNMENT INTERVENTION ON INDUSTRY LIQUIDITY

Liquidity in the market is important both in allowing businesses to cover immediate shortfalls or shortages of energy and to allow retailers to offer longer term contracts to generators, especially those seeking such security to finance new plants.

The recent Issues Paper of the Energy Market Review recognised that the availability of such liquidity with "Innovative and sophisticated financial markets (is) crucial to the development of energy markets as they enhance market participants' capacity to manage the new commercial risks associated with these markets, particularly exposure to volatile wholesale electricity markets." (p.8)

One feature of government controls, and a manifestation of their effect in preventing competition is the dampening effect this has on the development of alternative financial instruments. Such instruments like swaps, caps and a whole host of exotic names develop in response to the need to defray risk. That said, these derivatives are no different from the now ancient notion of futures to which Shakespeare gave such a bad name in The Merchant of Venice.

Bad name or not, it is to the mutual advantage of buyers and sellers to obtain greater certainty of expenditures and revenues. This allows them to plan ahead without the innovatory-sapping and potentially financially devastating effect of government control.

There have been claims that the Victorian market has been short on liquidity. The force of such claims was particularly strong in the period leading up to what was expected to be a tight supply/demand situation during this year's summer months. Lack of liquidity is more likely to occur where there are only few suppliers or customers. The relatively isolated markets in Australia will always run such risks.

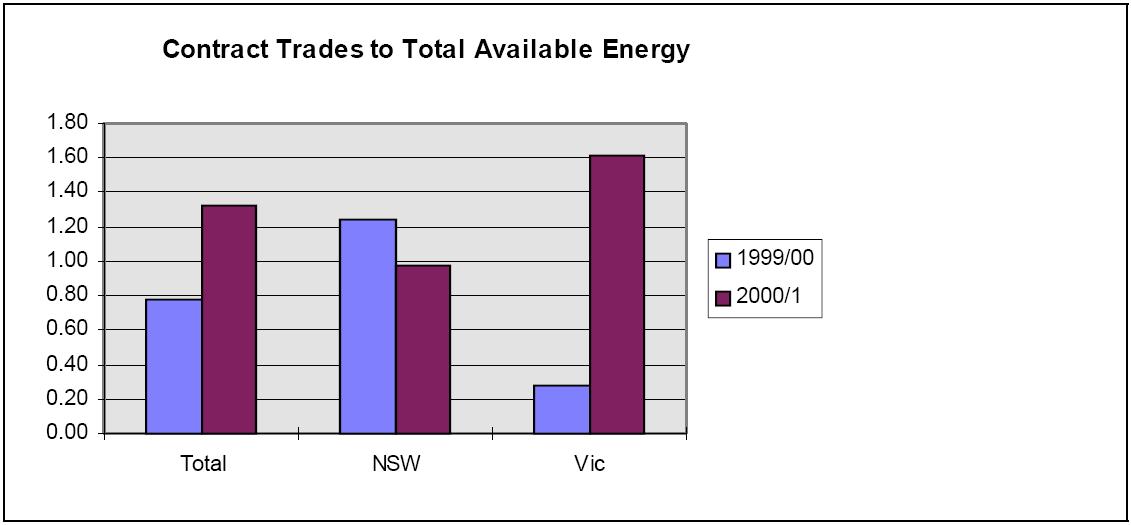

Whatever the merits of the claims for Victoria -- and any retailer that was under-contracted has in the event been fortunate -- there is a very rapid growth in derivative or futures contracts. AFMA data is the best we have available on contract transactions. AFMA's Over-The-Counter data indicates a very strong growth in liquidity -- over 50% last year for the market as a whole. Chart 1 illustrates this.

Chart 1

A notable feature of Chart 1 is that in relation to the energy market, the turnover of contracts in NSW declined last year while that of Victoria increased fivefold. Whilst the Victorian market is far from mature in terms of trading activity (typically commodity markets have a physical delivery to trade turnover ratio of 1:6) there is far greater trading than in NSW. Victorian retailers and generators were seeking out ways of defraying their risks but in NSW there was far less need to do so because the Government has mandated a form of insurance through ETEF.

Particularly strong growth was recorded in swaptions, an instrument that gives retailers the ability to pursue business opportunities without being locked into energy. In contract numbers, swaptions in Victoria increased fourfold while in NSW they decreased. This is a most significant feature since an instrument like this gives marketers an opportunity, at low cost, to seek new custom secure in the knowledge that they have contract coverage in the event that they are successful. Chart 2 shows the changing demand of different derivatives.

Chart 2

The compulsory insurance scheme ETEF is clearly the main reason for the difference between NSW and Victoria. In NSW this is stunting the growth in the market and denying consumers the best deals.

USE OF MARGINAL COSTS IN SETTING WHOLESALE PRICES

The ETEF defines long run marginal costs to incorporate a "reasonable" profit. Even so, the true price that a new generator would enter the market must cover all, not just the marginal costs. And it is that price of new generation that dictates the long run price of generation.

The following analysis of the use of marginal cost is taken from Brennan. (1)

The "marginal" generator has to expect that prices will, on average, cover not just its variable costs but its fixed capital costs as well. This can lead in simple cases to prices substantially above average variable costs in peak periods.

To get a feel for the flaw in the marginal costs test, let us turn first to a more familiar industry—resort hotels. Imagine that in a seaside town, one can build hotels. The optimal size for a hotel is 100 rooms. Once built, it costs $50/day to maintain a room, including cleaning, electricity, water, and predictable wear-and-tear from usage. The fixed annual capital costs for the hotel are $1,095,000 per year ($30/day/room, for 365 days and 100 rooms). There is no relevant restriction on entry, i.e., if one thinks that one can profitably operate a 100-room hotel in this town, one can build it. Firms are assumed to be acting competitively, i.e., take the going room rate as given in making decisions whether to build a new hotel.

Suppose first that demand to use this resort is roughly the same all year round. In that case, hotels will enter up to the point where the price of a room is $80/day. $50 of that $80 covers the cost of maintaining a room—the average variable cost. $30 of that $80 goes to cover the capital cost of the hotel. At prices above $80, more hotels would be built. If price were forecast to be below $80, say $50, no one would enter. The marginal costs test would fail to predict competitive prices in the market.

Next, imagine that demand for hotel rooms at this resort town is seasonal. For three months out of the year, people really want to come to the beach. The rest of the time, demand for rooms is weak. In such a situation, a decision to build a new hotel will be predicated on filling it up during the summer season. Accordingly, the price of hotels in the summer will be $170/day. $50 of this rate is the average variable cost, and $120 is needed to cover the cost of the hotel entirely from summer occupancy. However, because every hotel gets to charge this rate during the summer, not only those hotels built to serve summer clients, they all will capture their capital costs at that time. The price of a room off-season would then be only $50. The marginal costs standard would predict off-peak rates, but would fail on-peak rates. Holding hotels to a marginal costs standard would mean that not only that none would be built to serve summer visitors to the resort. It would also imply that year-round hotels would be unable to recover their capital costs as well.

Back to electricity

The fundamental peak-load pricing principles that hold for hotels regarding peak-load pricing hold for electricity as well. First imagine that there is only one kind of electricity generator with 100 megawatts of capacity, with average variable costs of (say) $30 per megawatt-hour (MWh). Suppose also that of the 8760 hours in a year, demand is at peak for 450 hours, about 2% of the time. Finally, suppose that the fixed annualized costs of building and maintaining the generator is $7.65 million, a figure chosen to come out to $170 per MW per peak hour. (This is also about 30% of the total variable cost of running a plant full out.) For simplicity, again, assume that at off-peak times capacity exceeds the amount of electricity demanded at $30/MWh. By analogy with the hotel example, the price of electricity would be $30/MWh off peak and $200/MWh ($30 + $170) on-peak.

To these sorts of issues can be added a range of others. Thus Littlechild (2) cites Joskow and Kahn as saying that market power may be inferred where the short run marginal cost of supplying electricity from the last unit that clears the market in each half hour is frequently below the clearing price. In doing so, however, he points out that such analytical frameworks are based on perfect knowledge, markets in equilibrium, and a structure where the suppliers have made the optimal decisions about scale, technology, etc.

He adds that in the real world of plant breakdowns, water shortages, changes in demand,

"It would be commercial suicide for a generator to assume that the market will always be in equilibrium and that it should price at marginal cost. The world is too risky for that. Investment in new plant is very expensive and typically takes a long time to recover. This is not to argue that the generation market is different from other markets ... in the real world, competitive markets generally are not characterised by price equal to marginal cost. That is the wrong benchmark for judging possibly anti-competitive behaviour. Life is more complex and in particular more risky than the marginal cost criterion recognises. In a competitive market each participant will seek to reduce its risks and cover its investment whenever and wherever it can. It cannot price at any time on the basis that each of its assets will earn an equilibrium return for the rest of its life." (p. 10)

These risk-associated features require a premium and are unlikely to be factored-into the price level set for the regulated customer classes under ETEF. Accordingly, that price level is likely to be lower than the true competitive rate. Of course, there would be an additional (sovereign risk) premium required to the degree that suppliers expect price capping to reduce future price levels.

OUTCOMES WHERE PRICES ARE SET TOO LOW

In setting wholesale price levels below true competitive levels for half of the market demand, the regulations would be seriously distorting the messages that the market might give regarding new capacity. Prices held artificially low are unsustainable and will lead to market distress. They are likely, for example, to provide inadequate signals for new capacity to be brought into the market.

Compared to setting the price too low, the dangers of setting excessive prices are considerably less. This is not the least because excessive prices bring their own remedy -- competitors find ways of winning the ostensibly captive markets. The recent Productivity Commission draft report on Part IIIA of the Trade Practices Act drew attention to this asymmetry in the context of "essential services" and advocated erring on the side of allowing a higher price rather than risking an excessively low price.

These approaches are even more appropriate in retailing which does not have the long lived capital assets of network services and consequent ability temporarily to serve customers at marginal cost.

Indeed, as soon as full retail competition is in place, it is difficult to see any scope for price setting. Any price that is set above market levels will mean customers will be won away from the incumbent supplier by a rival seeking to take advantage of a profitable opportunity. In fact, an existing retailer may be vulnerable to a rival who is able to better its price because the target customers are complementary to others that it presently serves. This might allow a rival to make price offers below the cost of the incumbent even if the latter is technically efficient.

CONCLUDING COMMENTS

Synthetic price setting is always difficult and should be terminated as soon as possible. Even the most well informed and skilled regulatory authority cannot assemble and analyse all the information that are routinely used by markets. We need commercial forces to determine prices and undertake the discovery process whereby new products and services are designed and capacity is tailored to market needs.

This submission points to a number of matters which lead us to the view that regulated prices are set too low in NSW. The evidence for this is:

- retail operating margins seem to be set somewhat lower than those set in the UK, the one market where regulation has proven to be a successful bridge to full competition; they are also comparable to those of Victoria where evidence to date has shown little competitive activity in the regulated customer classes;

- the notion of cost pass through for generation is likely to understate the true costs of generation; perhaps some assessment of what these might be could be undertaken by examining contract market prices in NSW and other states

- the fact that NSW has seen even less retail churning than Victoria is strong prima facie evidence that there is insufficient "headroom" for rival retailers to make profitable offers in the regulated customer class.

Finally, we would reitterate that with markets like electricity retailing where there are no entry barriers, the authorities should err on the side of setting price ceilings too high rather than too low, since competition provides an antidote for the former but not the latter.

ENDNOTES

1. Timothy J. Brennan, Checking for Market Power in Electricity: The Perils of Price-Cost Margins, (forthcoming).

2. Stephen Littlechild Electricity: Regulatory Developments Around the World , The Beesley Lectures on Regulation Series XI, IEA/LBS, London 9 October 2001 (Revised version 12 November 2001)

No comments:

Post a Comment