Address to the ACCC 2004 Regulatory Conference

29 July 2004

HOW THE DEITIES APPROACHED MONOPOLY

Professor Fels was fond of quoting the following famous words from Adam Smith (1)

"People of the same trade seldom meet together, even for merriment and diversion, but the conversation ends in a conspiracy against the public, or in some contrivance to raise prices."

Smith went on to say

"It is impossible indeed to prevent such meetings, by any law which either could be executed, or would be consistent with liberty and justice."

Clearly, he had a more robust view of liberty than those who enacted the anti-trust acts! He was however close to the mark when, to discourage government regulatory activism, he continued

"In a free trade an effectual combination cannot be established but by the unanimous consent of every single trader, and it cannot last longer than every single trader continues of the same mind."

PRICE SETTING

There is a vast literature in economics about prices. Indeed, price is at the heart of the discipline in so far it is the ultimate proxy for the value people assign to a purchase, and the cost to producers in its supply. Price is therefore the means of signaling new supplies and rationing existing supplies.

However, there is not a great deal of material on the procedures by which the price gets set, especially when the product is subject to rapidly changing demand and supply and when costs have a large fixed cost element.

The process by which price was set was glossed over by Adam Smith, who merely stated that "The actual price at which any commodity is commonly sold is called its market price. It may either be above, or below, or exactly the same as its natural price." He noted for example, "All commodities are more or less liable to variations of price, but some are much more so than others. In the linen or woollen manufactures, for example, the same number of hands will annually work up very nearly the same quantity of linen and woollen cloth. The variations in the market price of such commodities, therefore, can arise only from some accidental variation in the demand. A public mourning raises the price of black cloth. But as the demand for most sorts of plain linen and woollen cloth is pretty uniform, so is likewise the price."

Significant in this statement is the acceptance of price rises being demand driven and the need for market, not government force to react to them.

MARGINAL COSTS

One important feature of modern economics is the notion of marginal cost. It is, however, a concept that is difficult for regulators to use either is setting prices or in determining whether suppliers are exercising monopoly powers. Setting supply so that price just covers costs of incremental production is a criteria for efficient production. Where costs are rising with additional output, pricing at marginal cost generally allows this production to be profitable. Where costs are falling because of lumpy capital, a price that barely covers marginal cost defines the least price at which a seller can supply his product to the market for any reasonable time. A price below this is not uncommon for short periods – some goods are given away as a promotional exercise, while electricity commonly is offered at a negative price to ensure a station is operational when a better price is being set. These and other deviations from charging above marginal cost, on closer scrutiny, are not exceptions to the general rule.

Marginal cost based prices that fail to cover average costs mean, if they are applied, their efficiency in allocating the good itself is overcome by the inefficiency in allocating the capital to produce it in the first place. If the capital can be covered by a lump sum, marginal cost pricing for the units as used is highly efficient.

This lump sum charge is easiest to accommodate in government owned facilities. But those facilities are notoriously cost padded and often built unwisely. Elsewhere however we see it in areas like gas pipelines where customers offer take-or-pay contracts, especially to foundation customers (where the "lump sum" price component is often in practice rolled-in with the unit supply price). Such efficiency enhancing features of contractual based prices are, of course, undermined if the supplier is obliged to offer non-foundation customers quantity supply at prices that do not include the risk premium that earlier customers have absorbed.

For electricity, using marginal costs as a basis for price setting has diverse implications for the different sorts of plant. It is useful to think of these as falling in pone of three categories:

- First there is the energy limited plant, usually thought of as hydro based plant, or sometimes gas fuelled where there is a daily limit.

- Secondly, there is the highly capital intensive baseload plant which has a marginal cost in Australia of between $5 and $15 per MWh.

- Finally, there is the high cost plant designed to operate only for a few hours per year but requiring very high prices, perhaps in the thousands of dollars, for those few hours if it is to be viable.

Almost everyone is in agreement that the energy limited plants should bid in a way that ensures they operate at the time when demand provides them the best price. But for the other plants, there is a perception in many quarters that they ought not to "game" the market by exploiting any temporary monopoly powers they might have. In some markets, the manager places a plant-by-plant limit on the price that might be bid. Usually, that limit is associated with some capacity mechanism price under which a portion of fixed costs are covered.

Now, private enterprise works best when the firm seeks to maximise the shareholder value from its operations, a construct that is actually the normal requirement under company law. Once a central body starts to second guess what is Aristotle's "just" price and Adam Smith's "normal" price and starts to enforce this, we have an unwinding of the market system that is the foundation of efficiency.

It is the basis of Frank Wolak's work (2) that the market in California deviated from the competitive ideal. While this is uncontroversial, much of his analysis is posited on wrongdoing where prices exceed system marginal costs because those bidding into the market were taking advantage of temporary monopoly. The paradigm promoted in this analysis relies on non-energy limited plant bidding their true marginal costs.

Yet we do not see such behaviour being routinely followed in markets. Thus for example:

- Newspapers have a trivial marginal cost and are clearly operating in oligopolistic markets yet seldom does the price fall to zero even when there is very intensive competitive wars

- Cable tv once the satellite space is booked is relatively cheap to bring to additional homes yet seldom does its price fall to near zero levels

- Airlines seldom sell seats at the bare minimum needed to cover marginal costs (though Ryanair in Europe appears to do so) even when planes are far from full

- And, as work we have published by Timothy Brennan of the University of Maryland illustrates, hotels seldom drop their prices to the real marginal cost even after they have been built and tend to do so only in distress situations where there has been a sustained fall in demand.

One reason why marginal cost based prices cannot occur on a regular basis is that the marginal producer would not recover the cost of its plant and would avoid building it in the first instance, and the whole supply system unravels. There are analysts of the electricity market who consider the situation is saved by having energy limited plant bid to maximise its revenue but this begs questions on how to treat plant competing in similar market segments. Surely it would not be appropriate to require such plant to operate with less flexibility. Even if an exception were to be made for energy limited plant, this clearly would not work in all electricity markets.

Cramton (3) demonstrates that bidding above marginal costs is the norm in most bid based markets where there is some unhedged capacity. The supplier is inhibited from using this potential by the existence of other suppliers, and by risk that demand can be curtailed.

The latter risk might seem to be slender in the context of a highly inelastic electricity market but, at the margin it is real. He produces the following diagram. This shows that even though the demand is highly inelastic for the market as a whole, for the relevant part of the market at the margin, a small scope to reduce demand offers some reasonable elasticity. Thus, if we have a 9000 MWh demand in the Vic/SA region even if only some 100 MW of this responds to price (last year according to NEMMCO there was some 250 MW of demand side response) the price elasticity faced by an individual firm in possession of some residual market power can be significant. In some cases, the supply bids are able to be made by large firms adjusting the voltage or frequency controls within their facilities.

More important than this discipline on the supplier in electricity markets is the discipline of competitors. All suppliers seek to maximise profits and economists or regulators who try to prevent this are frustrating the market processes that drive efficiency. There are hardly any real life examples of perfect competition in which the supplier is a pure price taker and if efficiency rested on this premise, market economies would not have prevailed in the way they have. For the profit maximising firms that populate the electricity industry in Australia, bidding above marginal cost is actually, and quite properly, inevitable.

As Cramton illustrates, a 1000 MW plant will bid the last MW at the price cap if this can be profitable. Thus, simplifying the Australian market, if the last MW of a 1000 MW plant is bid at $10,000 per MWh and this sets the price for an hour, the plant receives this for all its output, earning a revenue of $10,000,000. If it fails to set the price and the marginal bid is $9900, the firm earns ($9900*999) $9,890,100, losing out only on the last MW and foregoing revenue of $9900 from the last MWh. If its marginal cost for the last MW is $100, it has foregone $9800 in the example.

Hence, it is outlaying $9800 hoping to gain additional revenue for all its output or ($100*1000) $100,000 less the $100 incremental cost. In the example, if it estimates the chances are better than 10:1 of setting the higher price, this is the best option. The constraint on the firm's actions is the existence of other firms all seeking to do the same thing, but losing marginal revenue when their competitor edges them out. The more players, the more potent that constraint until, with the stylised perfect market, comes fully constrained behaviour.

Over time, as firms learn more about their competitors' behaviour the scope to gain diminishes. This tends to mute the degree to which firms will put some capacity at risk since their competitors' behaviour becomes familiar. But they will commonly leave some supply at high levels because that behaviour is never fully anticipated and because the circumstances of competitors are likely to change as a result of outages etc. Prices are therefore not closely related to fixed costs but reflect marginal costs, demand and the levels of competition.

The other major factor in quelling the firms' proclivity to take advantage of their demand curves is forward contracting. Once a firm has a contract, it has no incentive to bid at greater than marginal costs for the contracted part of its output. To the extent it does so it is, in fact, overriding the benefit it had arranged to have price certainty for a specific volume. Suppliers are as keen to forward contract as are the retailers, since this means risks are hedged. The forward contracts normally have a premium over marginal costs reflecting the market behaviour that has been described.

Contracting is also the means by which high cost marginal plant is normally built. High cost occasional use plant is developed to be used in abnormal circumstances. Individual users often have "back up" generation for their own use. Where such generation is made available to several users, it has a similar insurance contract effect, rather like the supply side contracts that retailers have to enable back-offs at needle peaks.

To achieve a stable supply of electricity means it is actually necessary for some firms to bid some capacity above marginal cost and to seek to raise prices. Without this there is too little incentive for additional investment in marginal, occasional use plant. (4) If marginal costs are all that can be earned, this would mean very discontinuous investment decisions driven by sudden soaring prices which, unless locked in, would collapse as soon as the capacity was brought on-stream. Indeed, it is hard to see how any investment in high fixed cost assets would take place.

APPLICATIONS TO AUSTRALIAN SUPPLIERS

But, let's look at some station bids on a hot day in summer. The following charts are derived from the excellent material on the Intelligent Energy Systems website.

The first, Loy Yang A is offering power at the limit of its capacity at a relatively high price but it is also raising its supply price at the peak hour to the $9000 per MWh level.

Another privately owned generator, Loy Yang B has all its capacity offers carefully sculpted to its marginal costs. Just a small margin is offered at the capacity limit at a price of $500 per MWh

The intermediate Newport station bids in an apparently erratic fashion. Again however, this reflects contracts (especially with TXU and for reactive power) and its marginal costs. If the firm can push the price up for the odd short period, they'll take it thank you very much.

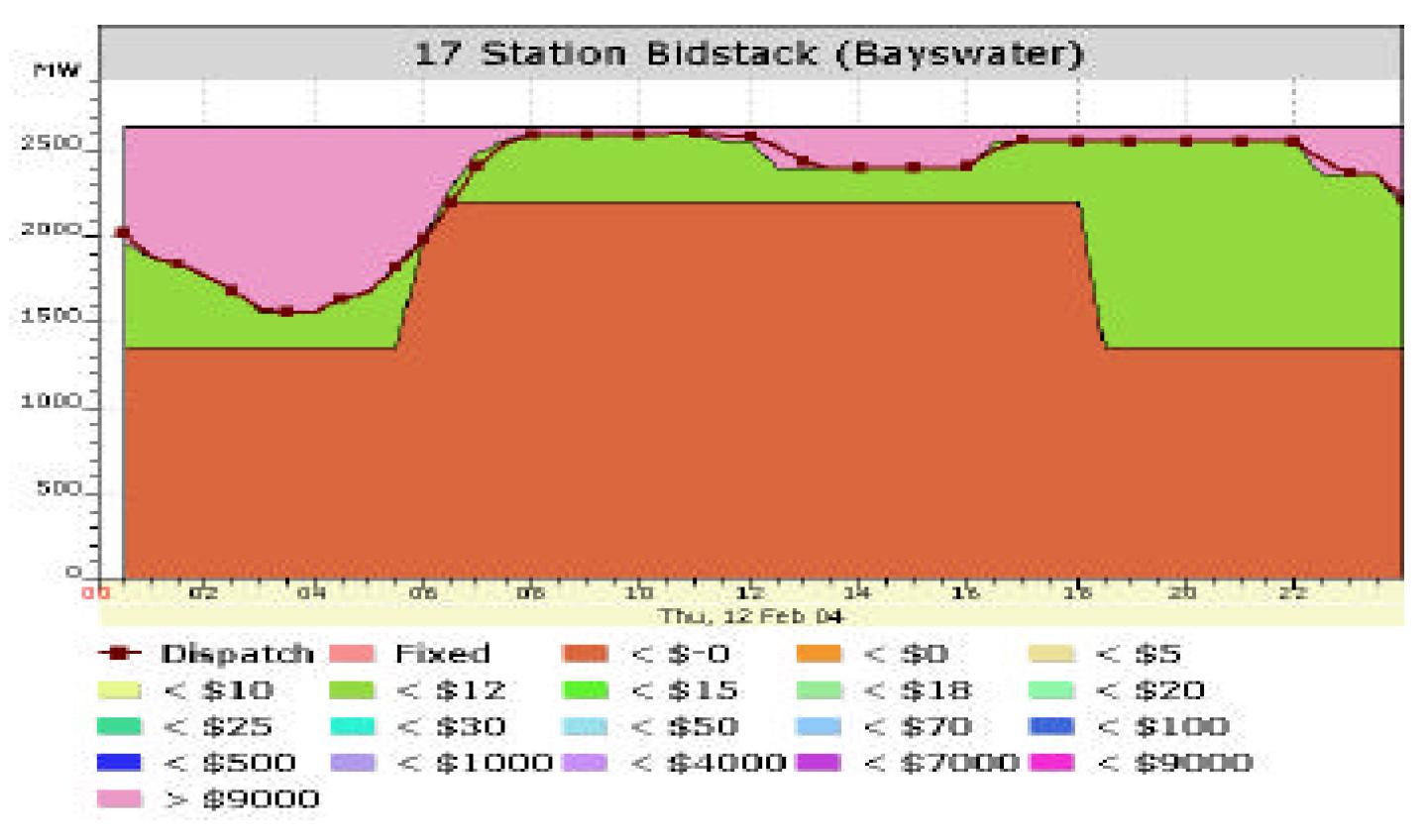

The same pattern is seen with the government owned stations. Here is Bayswater seeking to gain increased spot revenue where it has an absence of contractual cover.

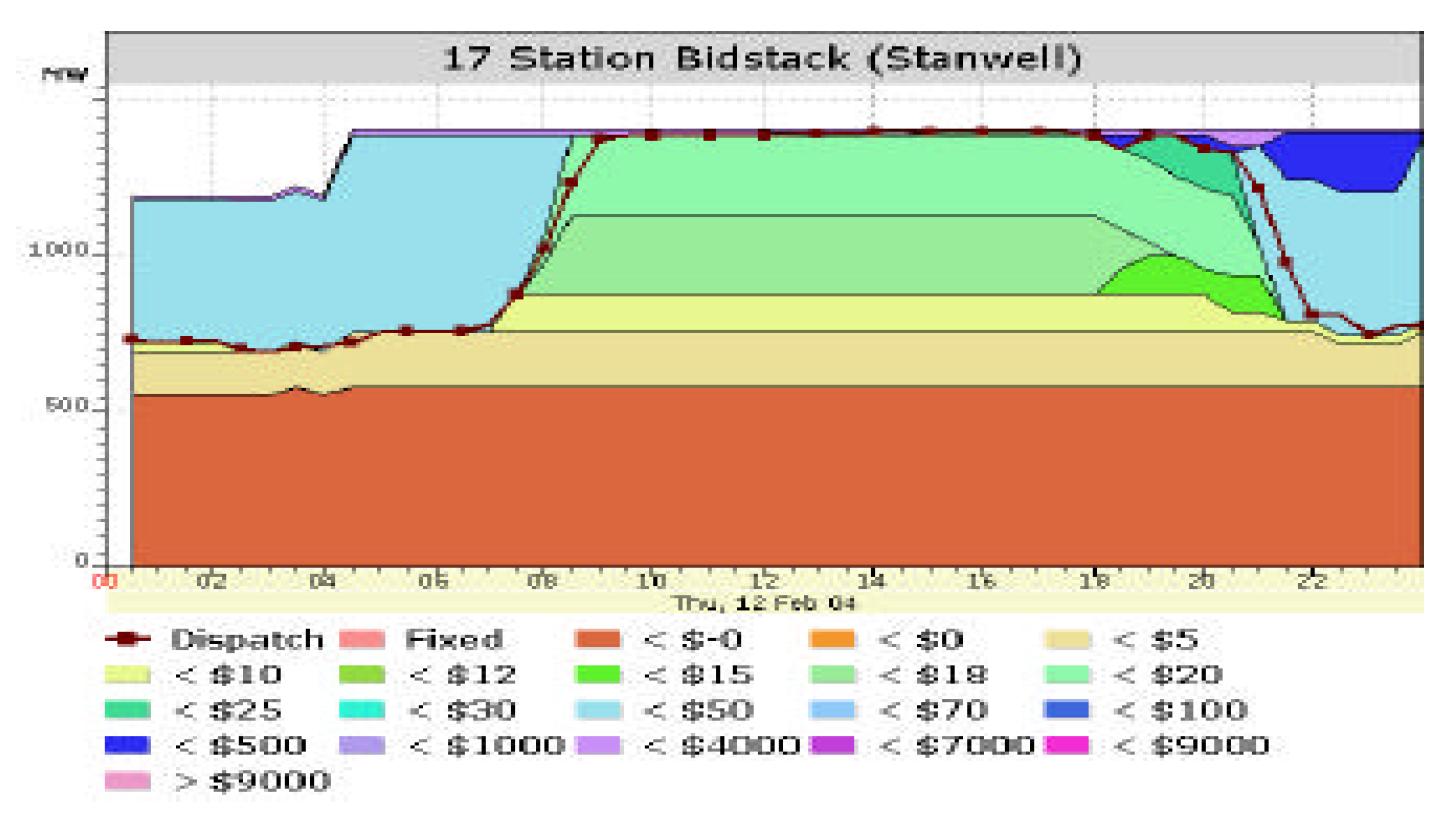

By contrast, Stanwell is bidding closer to its marginal cost with only a thin sliver of supply being offered at extortionate prices and with a bit of a try-on (which failed on this day) for a highish price late at night.

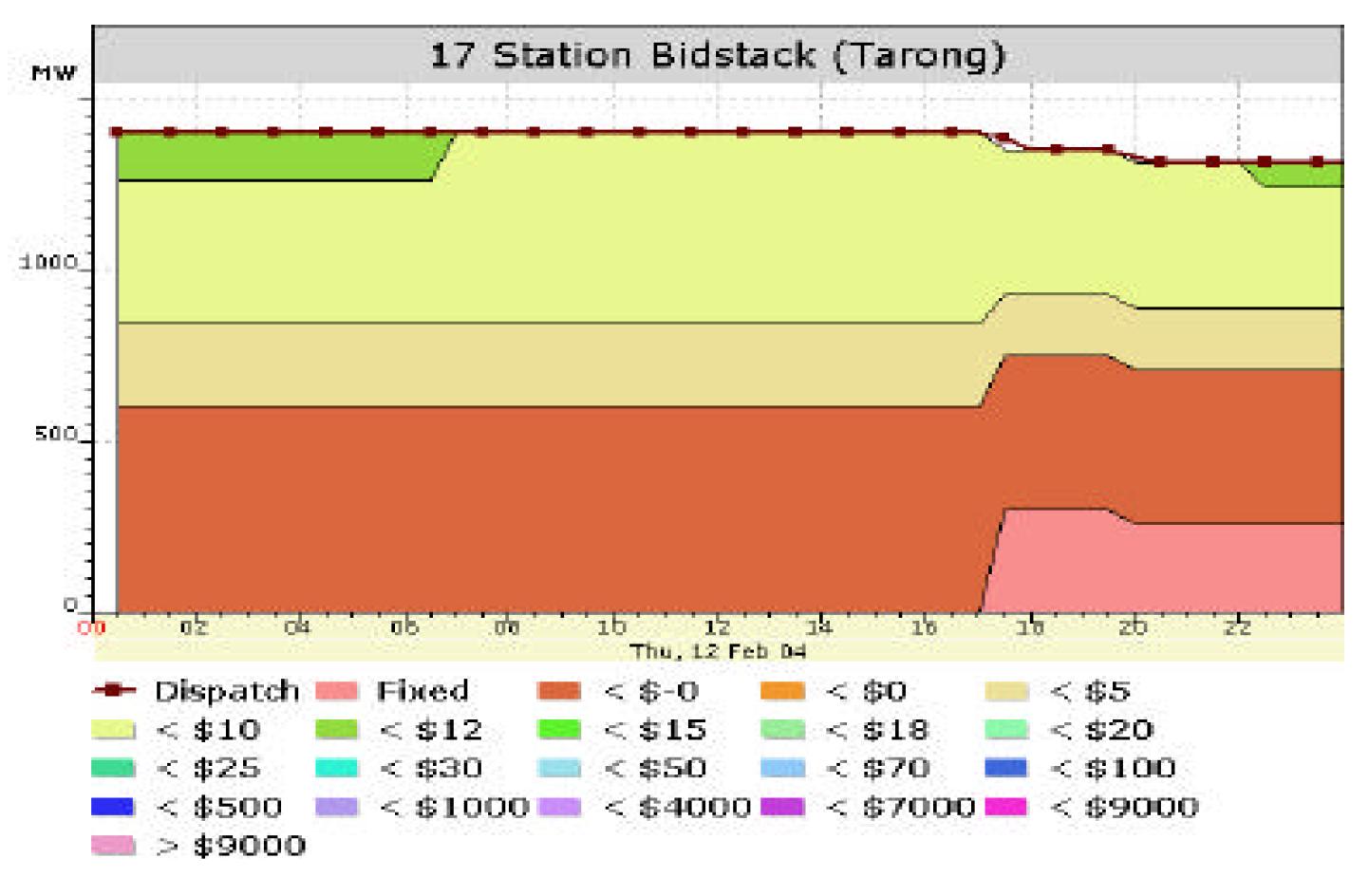

And Tarong is not engaged in any "gaming" at all, bidding only its marginal cost for what is, presumably, a fully contracted supply.

SOME OUTCOMES IN AUSTRALIAN ELECTRICITY MARKETS

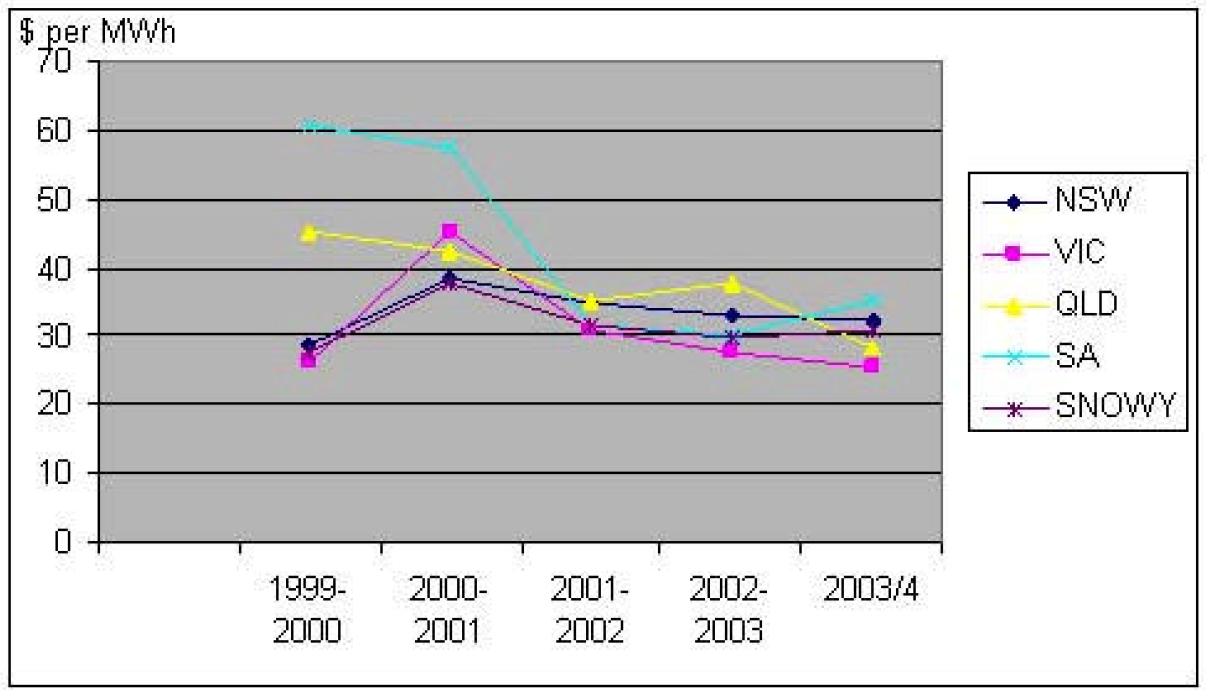

Overall prices remain low. They are still below the fabled $40 per MWh level that was said, back in 1995 to be the new baseload investment level. (5) Prices last year ranged from $25 in Victoria to a heady $35 in South Australia and few would see the following graphed prices as doing other than trending down.

Average Annual Price

Although the NECA analysis of flat contracts (see below) shows a little upward movement for the coming years, few enterprises would be rushing to build new baseload plant by 2007 on the back of these prices.

The point about all this is that with almost total freedom of electricity firms to seek the best possible price for their product, they like other such suppliers in the economy are only achieving a modest level of profit. Nonetheless, increased capacity at the needed peaking end has been commissioned

A relatively free market has proved to offer adequate incentives for new capacity. Since the late 1990s in the eastern connected system, this has amounted to over 4,000 MW - about a ten per cent increase in a system that was largely oversupplied. This has been broadly of the type that might have been expected to be built: a mixture of intermediate and peak in increasingly peaky South Australia and Victoria, mainly baseload in Queensland, where energy demand is growing more rapidly. The table below indicates the particular capacity commissioned. In addition to this, construction of over 700 MW of capacity is committed and considerably more is at various stages of evaluation, including one not shown here, Kogan Creek, that is now actually underway.

| Year | Max capacity (MW) | |

| Oakey Creek | 1999 | 344 |

| Roma | 1999 | 84 |

| Callide C | 2001 | 1000 |

| Millmerran | 2002 | 900 |

| Swanbank E | 2002 | 410 |

| Total Qld | 2738 | |

| NSW Redbank | 2001 | 150 |

| Bairnsdale | 2001 | 94 |

| Somerton | 2002 | 160 |

| Valley Power | 2002 | 390 |

| Total Vic | 644 | |

| Ladbroke | 2000 | 100 |

| Pelican Point | 2001 | 510 |

| Quarantine | 2001 | 100 |

| Hallett | 2002 | 220 |

| Total SA | 930 | |

| NEM Total | 4462 | |

This investment outcome is a vindication of the "energy only" market approach adopted in Australia. Supplier bids that are free to incorporate all costs provide the same incentives for entrepreneurs to build new capacity in electricity as they do in all other industries. As long as there is workable competition, prices that are free to fluctuate will give the appropriate signals. Such market structures are superior to other options like a two part tariff with a "supply" charge and a "capacity" charge. They avoid regulatory guessing to set prices for capacity payments and consequent restraints on each plant manager's price strategy to ensure that market bids reflect marginal costs.

The NEMMCO 2004 Statement of Opportunities released at the beginning of August shows some tightening of demand in the Vic/South Australia region for the coming summer in particular. It appears that Snowy is to build a relatively large gas fired plant in Melbourne and Basslink is progressing but these will not be available until December 2005. It is also the case that the forecasting methodology may underestimate the plant availability, since it relies on forecasts from suppliers that are not independently verified. In any event, the lack of a substantial forward price hike indicates that the retail industry is not anticipating shortages.

In summary though, the Australian market has worked well. It has delivered low prices, and provided adequate incentive for new capacity. Its frailties are associated with continued government intervention and, perhaps, muted incentives that are inherent in government ownership.

The vulnerabilities from government intervention are seen especially with household sector retail price controls and mandatory retail insurance provisions. These could distort new investment signals. Concerns over government ownership would be intensified if this resulted in non-commercial investment activity as a form of industry assistance since this could undermine private investors' confidence in the industry. But for the present, market processes are working well and market imperfections in the form of government regulation and ownership have not seriously undermined the supply industry's efficiency.

ENDNOTES

1. Adam Smith Wealth of Nations Ch 10

2. see, for example, http://papers.ssrn.com/sol3/papers.cfm?abstract_id=503464; http://www.accc.gov.au/content/item.phtml?itemId=489167&nodeId=file410db2dbc3069&fn=Session%201:Market%20Power%20-%20Frank%20Wolak%20paper%201.pdf. Though Wolak supports a deregulatory approach in principle in, ftp://zia.stanford.edu/pub/papers/response.wolak.pdf

3. Peter Cramton, Competitive Bidding Behaviour in Uniform-Price Markets, Hawaii International Conference on System Sciences, January 2004

4. It would be possible for government to undertake such investment but this begs the same questions as any other government investment, namely at what level to make the investment and how to do so without this impacting on the incentives of the mainstream suppliers.

5. Though very low coal costs and, according to some sources, a low target return on capital, has allowed development of the new Queensland Government owned generator at Kogan Creek to proceed on contracts said to be under $32 per MWh.

No comments:

Post a Comment