The Productivity Commission Report on the Gas Access Regime

INTRODUCTION

The regulatory arrangements covering gas pipelines have been under review for many years. The initial need for regulation stemmed from the natural monopoly inherent with most pipelines and the fact that those built pre the mid 1990s had some exclusive franchises and, in the context of the Hilmer reforms, required some fair basis under which they could be opened for use by new suppliers. Prior to the PC's Gas Access Regime Review (1) there were two earlier reviews. These were that by the Productivity Commission of Part IIIA of the Trade Practices Act (Review of the National Access Regime),which reported in September 2001 and the Energy Market Review (the Parer Review), which reported in December 2003.

Both these reviews recommended some deregulation of the present controls on the gas pipeline industry, especially with regard to new facilities. In addition, decisions by Australian Competition Tribunal in the Eastern Gas Pipeline (Bass Strait to Sydney) the Minister regarding the Moomba to Sydney pipeline have been deregulatory rulings that might set precedents.

Dissatisfaction with the present arrangements is clear given the failure of any transmission pipeline owner to accept the regulatory rulings of the ACCC or (in the case of WA) the local regulator. Subsequent litigation and reviews have contributed to uncertainty. Although strongly contested by the ACCC, most participants in the development of gas pipelines consider the current arrangements bring prices below those justified on market risk grounds and consider such outcomes are bringing a sub-optimal level of investment. Issues are:

- when do market disciplines provide better outcomes than regulation both for existing networks and for new ones and how (or whether) to provide a transition to a deregulated state?

- whether there are less intrusive means of regulating pipelines other than the presently prevailing cost based price determination which leads to considerable lobbying costs and controversy regarding the prices actually specified

- are the present pricing principles appropriate?

Unfortunately, while the PC report contains much of value and incorporates a high standard of analysis, many of its key recommendations are anodyne, contain considerable ambiguity and would enable regulatory agencies to maintain the very approaches that the PC is highly critical of in its analysis. Decisions made by the Commonwealth Minister and the Australian Competition Tribunal have provided guidance for the better administration of gas pipelines under National Competition Policy and under the Gas Code. Following those decisions, in order to facilitate a more market-oriented administrative regime, the Productivity Commission should have been more forceful and specific in its recommendations. It should, for example, have offered firm guidelines that regulation is unnecessary once a market is supplied by competing pipelines.

DEREGULATION OF EXISTING PIPELINES

The PC recognises that the existing Gas Access Regime is likely to be distorting investment as firms seek ways to escape oversight. The PC notes that

The Gas Access Regime's coverage test sets too low a threshold for cost-based price regulation. That is, coverage decisions could involve the regulatory error of applying cost-based price regulation when its costs outweigh its benefits, including with respect to investment. (2)

And it adds

Generally, cost-based price regulation should be considered only if service providers have substantial market power. Where market power is not strong, such as where there is emerging competition, in the long run the costs of regulated prices are likely to outweigh the cost of the market failure that such regulation attempts to correct. FINDING 4.5

The final PC Gas Report exposes at length the hubris and faulty analysis employed by the ACCC in its pro-regulatory approach to the industry. But the recommendations offer no directions as to how this can be reformed. Much reliance is placed on recommending an "overarching objects clause" that would:

"promote the economically efficient operation and use of, and economically efficient investment in, the services of transmission pipelines and distribution networks, thereby promoting effective competition in upstream and downstream markets."

These goals are unexceptional and would be readily agreed by all with any pretensions to "economic rationality" and perhaps also by those who express opposition to such themes. Indeed, the ACCC has always formulated its decisions within such a framework. In the event, therefore the PC has offered licence to the ACCC to continue on its present course. That course has focussed on finding a basis for reducing the prices charged by gas pipelines in order to reduce prices to the consumer. Critical in making assessments of pipelines' prices is the regulator's capital value assessment of the pipeline and estimated Weighted Average Cost of Capital that is employed.

In respect of the former, capital value once sunk is considerably less than when it is being contemplated. A major debate among economists concerns how to estimate capital value of "essential facilities" that have monopoly power. The ACCC has invariably sought to reduce the prices sought by pipeline owners, often by arguing that its value is less than its replacement cost. The appointment of Professor Stephen King as a Commissioner is significant since his work for the ACCC and other clients has often featured a strong emphasis on having prices set on a basis that does not require the recoupment of many of the costs that the supplying firm has "sunk" in the process of its investment. (3) While a windfall to consumers, such approaches offer a signal to investors that has the "chilling" effect on investment about which the PC has expressed considerable concern.

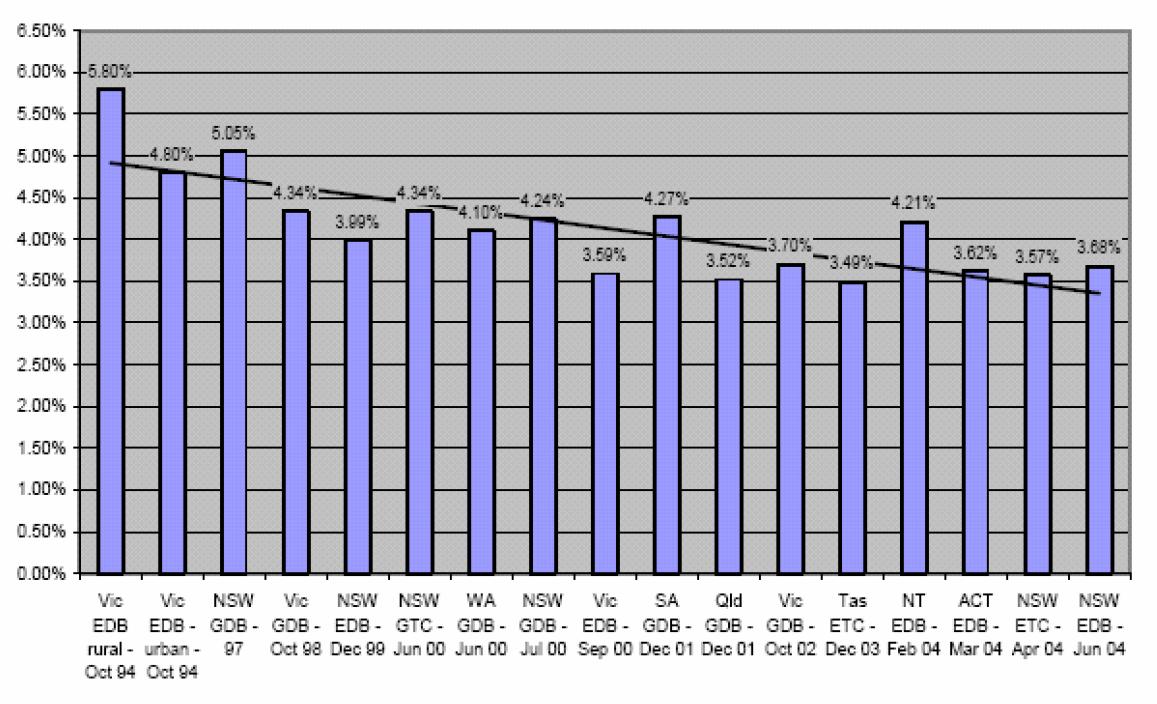

The Energy Networks Association (ENA) has illustrated a declining margin over the "risk free" rate in regulatory decisions illustrated as follows (4) and claims that UK and US regulatory decisions are more generous to the investor (a claim the ACCC and its own consultants dispute). The ENA's estimated trend is as follows:

Having assessed that the price determinations by the ACCC have been inappropriately harsh to the supplier, the PC's solutions to counter these are threefold:

- Specifying (Recommendation 7.1) that tariffs should be set to meet the efficient costs of providing access to the reference services and give a return commensurate with the risks.

- This might be little more than an exhortation to the regulator to undertake the process it already considers it follows.

- To assemble prominent people in order to reach a consensus. Recommendation 7.11 says

A study should be undertaken by a group of recognised experts in the field of financial economics that considers whether a robust method can be developed for setting businesses' expected rate of return on capital under incentive regulation. This should include a review of the use of the capital asset pricing model by Australian regulators.

- It is doubtful that the desired consensus could emerge.

- The Report also recommends a light handed monitoring option. The recommendation on this is somewhat weaker in the final report (in which the Gas Access Regime should "provide for a light handed form of regulation") compared to the draft report which added that the present approach of "access arrangements with reference tariffs would only occur in the more extreme circumstances".

These recommendations, which leave the ACCC as the main regulatory body, are dependent on that agency adopting a changed philosophical framework of control. Yet there is no indication of such a change. There is certainly no sign that the ACCC has agreed to the following statement of the Minister:

A Moomba to Sydney gas transmission service in future may be contracted for via the Moomba–Adelaide pipeline system (MAPS) and SEA [South East Australia] Gas pipelines and either of the Interconnect or the EGP [Eastern Gas Pipeline] ... It is therefore no longer appropriate to think in terms of gas transportation as being only from a single well head or processing plant along a single transmission pipeline to a single offtake point. (5)

Indeed, in an address in Sydney, (6) the energy Commissioner, Ed Willett, said that it is incorrect to consider the Moomba to Sydney pipeline to be in competition with that from Bass Strait. He argued that the price for gas carriage remains too high and maintained his faith in the synthetic estimates of the true price estimated by the ACCC's New York based consultants. And he argued that the evidence of pipeline building, "rather put the lie to the industry's claim that ACCC regulation has, in the words of one major player "had a chilling effect" on investment." (7) The ACCC position remains one of unreconstructed faith in itself as an institution out-performing competition in creating efficiency.

In contrast, the Minister's decision on Moomba to Sydney cautiously reaches out to a market based approach. For the PC to have offered support for this would have allowed some better underpinning of it. In this respect the PC could have provided guidance about when regulatory agencies ought not to be routinely involved in price setting and access conditions.

In line with its assessments, guidance could have been along the lines implied by Minister Macfarlane in his statement and might have argued for "an onus on the regulator to exit regulatory control once more than one pipeline of a significant size was serving a particular market, whether or not there was duplication of the pipelines".

GREENFIELD SITES

The regulatory moratorium flagged in the PC's Inquiry into Part IIIA and the Energy Market Review is strengthened in the PC final report on Gas Access. It also notes

The Gas Access Regime is likely to be distorting investment in favour of less risky projects, including altering the nature and timing of pipeline investments. Pipeline construction might be delayed, for example, and there might be greater emphasis on building capacity that is essentially fully contracted prior to construction. Such alterations can inhibit the emergence of competition in upstream and downstream markets and generate inefficiencies. FINDING 4.3

Other findings further develop this. The final report recommends the Minister should be able to offer a binding no-coverage ruling for 15 years with the pipeline remaining uncovered thereafter unless a successful coverage application finds otherwise.

However, the regulatory approach is rather stricter than that envisaged by the Energy Market Review which argued that it would be difficult to foresee a case for regulating new transmission pipelines and that regulatory strictures should be developed accordingly. This unfortunate backward step is aggravated by leaving the decision on coverage with the Minister rather than setting a standard on which the NCC might recommend a deregulatory approach. This is especially so once it is recalled that in the past the NCC has expressed a wish to see all new pipelines regulated unless the pipelines offered competitive provision to the supply area as well as the market and unless they could be assured that the parallel pipes would operate non-collusively. This very strict test of market power would never see a deregulated transmission system

MERIT APPEALS

The PC recommends a full merits appeal of the regulator's decision.

This is welcomed by the industry but in the context of a properly constituted regulatory organisation that has been set tight rules as to the approaches it must take, such a full appeal mechanism is unnecessary. In recommending that approach, the PC is unfortunately (but realistically) acknowledging that its recommendations will not be sufficient to ensure a body determined upon a different regulatory outcome than that which it favours itself will be able to reinterpret the generalised form of any code that is developed in the light of the recommendations. A more forceful and precise regulatory form could have obviated this.

ENDNOTES

1. Review of the Gas Access Regime, Productivity Commission, Report No. 31, 11 June 2004 and made public 10 August 2004.

2. P.107

3. The PC quotes King and Gans as saying "... a regulator, who sets an access price after the relevant investment is sunk, has a strong social incentive to set a low access price. Such an access price will promote efficient use of the facility, competition and social welfare without deterring the investment that has already occurred". (p. 104). However there is also a recognition in their work of the adverse effects of "asymmetric truncation" that lops off the high returns of successful entrepreneurship.

4. See Address by Bill Nagle to ACCC Regulation Conference, July 2004

5. Macfarlane I. (Minister for Industry, Tourism and Resources) 2003, Applications for Revocation of Coverage of Certain Portions of the Moomba to Sydney Pipeline System: Statement of Reasons.

6. Ed Willett, Energy Market Access and Regulation, address to the Australian Energy & Utility Summit, 22 July 2004.

7. In the same address on later occasions, the ACCC has cited the work of ACiLTasman in suggesting the benefit of the ACCC's regulation (of electricity plus gas) was somewhere between $2-11 billion. That analysis was discredited at the ACCC's annual regulatory conference (30 July 2004) and also is heavily criticised in the PC Gas Access Review.

No comments:

Post a Comment