Submission to the Victorian Department of Infrastructure

SUMMARY

The privatisation of the Victorian industry has brought a considerable increase in efficiency, partly as a result of structural re-organisations and ownership changes since the privatisation process commenced. The electricity industry has certain features not shared by most other industries, including non-storability of its product, but these are not unique and should not be used as justification for enhanced regulatory oversight of mergers within the industry. There is a danger that inefficient corporate structures will follow from special regulatory measures that hinder corporate strategies within the industry through inhibiting vertical integration.

MARKET POWER AND THE FOUR ELEMENTS

OF ELECTRICITY SUPPLY

Issues of market power have been major motivations of the structural separation of the various elements of the electricity industry in Australia (generation, transmission, distribution and retailing). The realisation in Australia from the early 1990s that generation and retailing could be competitively supplied gave rise to the acceptance that having rival suppliers would result in greater efficiencies and lower costs in these two areas.

At the same time, recognition that the transmission and distribution were likely to remain monopolistic meant a separation to ensure firms did not favour affiliates in retailing or generation. The separation took forms ranging from full corporate disaggregation to "ring fencing" areas that might be used to favour affiliated businesses.

The emergence of retailing as an important function in the electricity market was not widely expected at the time of the structural separation of the former integrated monopolies. Nor was the importance of retailer risk avoidance and control anticipated, partly because maximum prices at the wholesale level were considerably lower than the current cap of $10,000 per MWh.

The need to avoid unnecessary risk has led to retailers and generators contracting on a wide variety of terms with a great many different financial instruments. Ownership is the ultimate such instrument, and retailer developed and owned new generators are now familiar. Generators have also forward-integrated into retailing (Snowy/RED, Yallourn/TXU). An early development along these lines was the TXU contract with Ecogen Energy, which though falling short of ownership, is considered to be similar in effect.

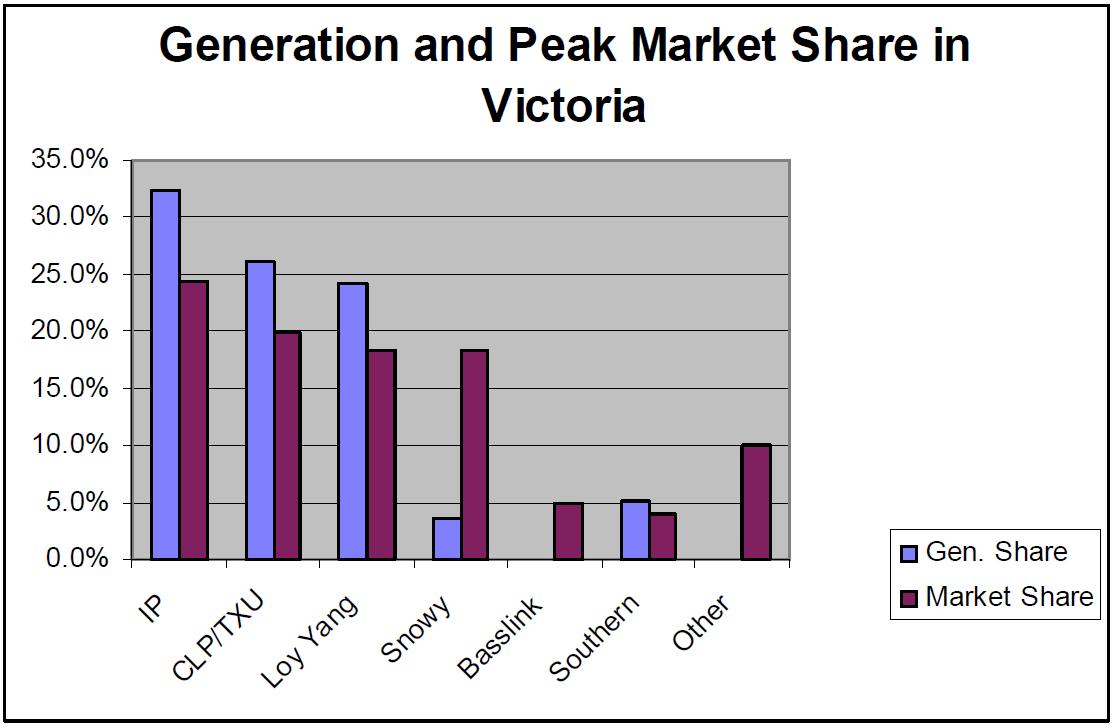

GENERATOR MARKET SHARE IN VICTORIA

The sale of the SECV as six generation businesses (Yallourn, Loy Yang A, Loy Yang B, Hazelwood, Ecogen and Southern Hydro), a transmission business and five retail/distributors has been followed by many secondary sales of these assets and developments of other assets. The latest ownership re-arrangement is the on-sale of some of the former TXU assets to China Light and Power, the owner of the Yallourn power station. This means that 80 per cent of the state's generation is owned by three businesses.

Peak and baseload power are not under common ownership at the present time. Although Valley Power (300 MW) was built by Mission and is now owned by International Power, its output is better described as mid range, as are the TXU/CLP plants at Newport and Jeeralang.

Peak capacity in Victoria comprises the Snowy (1,900 MW deliverable) Southern Hydro (Meridian) (up to 480 MW) and the smaller gas turbine plants of AGL at Somerton (150 MW) and Alinta at Bairnsdale (80 MW). In addition there is the planned Laverton plant of Snowy.

Once the transmission links are factored in, the market share that the state domiciled generators could command is reduced considerably. In addition to Snowy, there are the links with South Australia and Basslink from next year. On this basis the four major suppliers combined have a capacity to supply only three quarters of the market.

In terms of the generation supply to Victoria, the following provides a picture of import capability plus in-state capability once Basslink is completed. This however is only a short term capability as neither Basslink nor Snowy could provide all their capacity for extended periods (though Snowy could be replaced by NSW supplies where its internal resources are low).

Figure 1

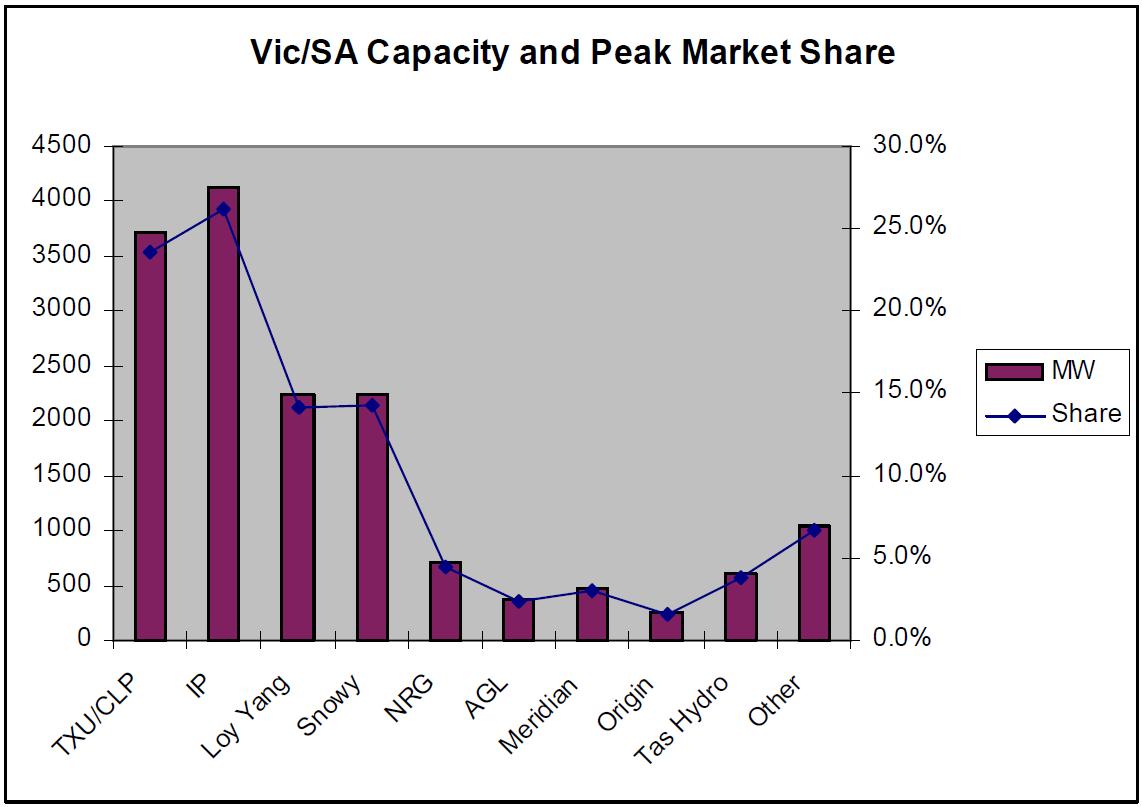

An alternative way of looking at the Victorian market is to consider it as a joint market with South Australia. NEMMCO often sees this as particularly meaningful for its own analyses. On that basis, joint supply is as follows.

Figure 2

Peak Power supplies are as in the case of Victoria plus the two Origin CCGT plants at Ladbroke Grove (83 MW) and Quarantine (95 MW).

The baseload supply structure comprises three major suppliers (CLP, Loy Yang Power and International Power) with NRG as a smaller but still substantial baseload supplier.

RETAIL MARKET SHARE

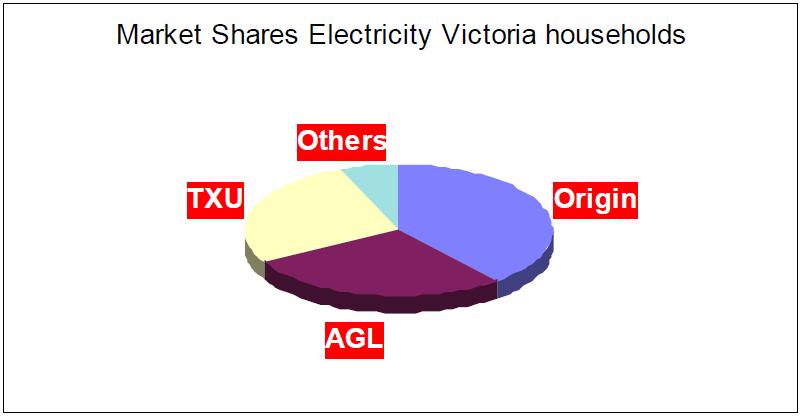

Origin Energy is the closest major retailer to a retail-only business. It has no generation in Victoria and less than two per cent of the combined Victoria SA supply. It has the largest market share among Victorian households as illustrated below

Figure 3

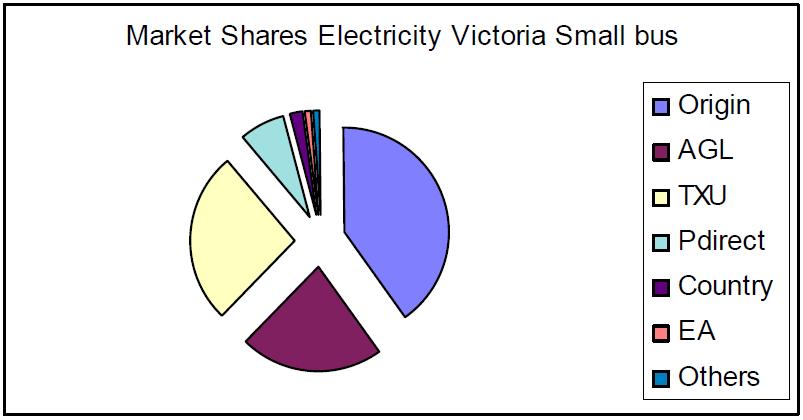

Origin also has the largest share of the small business market, into which some smaller retailers like Powerdirect have also made incursions.

Figure 4

JOINT PROVISION OF RETAIL AND GENERATION

The original market design in Victoria and elsewhere envisaged stand-alone businesses concentrating on generation, retail/distribution or transmission. Retailing and distribution were separated by a required ring fencing arrangement.

While this was considered to be a source of potential fragility, the retail/distribution separation has proved to be enduring permanent. Origin Energy, operating without any distribution activities and with only minor generation resources, has become the purest example of a stand-alone retailer but both AGL and TXU have clear internal separations between the two business functions.

The first major move by a business upstream or downstream was the foundation by Yallourn of a retail arm, Auspower. Treated as something of an aberration initially, it has targeted only the largest customers. Other generators have since established retail arms, while retailers, notably AGL and TXU have moved into generation, in the case of TXU not only through its own company ownership but also through an independent entity which is comprehensively contracted. Snowy Hydro, as well as commencing building a new gas power station at Laverton, has also bought the startup retailer RED.

At the present time the only entity with a rough correspondence of generation and retail is CLP.

Estimated supply and retail market shares of Victoria are shown below. (Basslink also gives the Tasmanian retailer Aurora a generation source for Victoria, a market it is targeting).

Table 1: Estimated Victorian Market Share

| Retail Sales | Supply capacity | |

| Origin | 36% | 0% |

| TXU/CLP/Auspower | 27% | 20% |

| IP | <1% | 25% |

| AGL | 22% | 1% |

| Loy Yang | 0% | 18% |

| Snowy | <1% | 5-18% |

| Other | 15% | 18-31% |

Hence, competition has led to a variety of market participants. We neither have the re-aggregation of the SECV, which some feared may be an outcome, nor do we have stand-alone players operating exclusively in one area of supply. Instead we presently have one firm with a high degree of retail and generation ownership, some with a degree of integration and others concentrating almost exclusively on one or the other. Such developments are not uncommon in resource intensive industries -- they can, for example, be seen in aluminium and forest products.

ISSUES RAISED IN CROSS OWNERSHIP

RULES FOR THE ENERGY SECTOR

THE ISSUES PAPER'S APPROACH

The Issues Paper includes a comprehensive and well thought through analysis of the matters confronting policy makers. It pulls together material on recent judicial determinations and market developments that point strongly towards a conclusion that the existing restraints have outlived their usefulness, could be having a detrimental effect on market certainty and could be inappropriately creating some unique regulatory arrangements in Victoria that are inconsistent with a national market.

The Issues Paper correctly notes that market power is only a concern if it is persistent, recognising that nearly all firms in other than totally atomistic supply markets have some ability to influence price in a transient manner. It accurately describes the issues where market power might be of concern as being excessive concentration or where a firm has control of a monopoly facility -- a transmission or distribution line -- and uses this control to favour an affiliate.

MERGERS AND INDUSTRY POLICY IN ELECTRICITY SUPPLY

Mergers that have the capacity to bring excessive market power are controlled under section 50 of the Trade Practices Act, largely administered by the ACCC which has put a number of tests in place that form the basis for examining merger proposals. The ACCC is a highly professional agency to which the Australian Parliament has extended considerable powers. The ACCC's powers are circumscribed by the Parliament since it could, under imprudent leadership, involve itself in commercial matters to such a degree that innovation is inhibited and businesses become regulator-oriented rather than customer-oriented.

The current Victorian cross-ownership provisions augment the ACCC's powers for one industry in one state. This is an inconsistency in both activity and geographic coverage, stemming from the mid 1990s privatisation process. While "belts and braces" regulation may have had an appropriate role given the experimental nature of the Victorian electricity privatisation, the outcome of the experiment has seen the maturing of a customer responsive industry the efficiency of which surpasses that of other jurisdictions when measured by a range of factors. Concerns about premature re-aggregation have now diminished and the specific legislation still in place may impede industry restructuring in ways that best take advantage of economies of scale and scope.

In this respect, it is implausible for a government policy organisation, or regulatory agency, to be able to correctly divine the appropriate structure for an industry. Even the highly regarded Japanese MITI, with its very close ties to industry was recognised to have made a crucial error in strongly discouraging Honda during the 1960s from becoming a motor vehicle manufacturer. MITI, which was then highly respected for its apparent industry policy acumen, argued that any additions to Nissan and Toyota would eat into the benefits of scale economies in the industry.

A key part of the Victorian industry's present level of efficiency is the dynamic and ceaseless examination by commercial parties of the assets and associated workforces of the industry's component parts with a view to ensuring they are yielding the best value to shareholders. None of the privatised businesses have their original ownership structure, an indication of the adaptability and value searching features of the industry.

Private ownership within a rivalrous industry environment is a key to creating sustained efficiency and customer value. Laws that monitor, and where appropriate curb any monopolistic behaviour are important supplements to the natural processes of the marketplace. However, if there are benefits in strengthening the ACCC's powers so that aspects of its decisions, in this case cross-ownership rules, are not appealable, this should be set at a national level and cover all industries.

In this respect the Issues Paper is compelling in saying,

"Applying quantitative ownership restrictions only with respect to the entities that are licensed within one State (Victoria) may lead to errors -- such as by overstating the market power that may be created by a merger within a State (and potentially precluding a merger that offered substantial benefits but had no effect on competition), but ignoring the market power that may be created by mergers that occur outside of the State (and potentially permitting a merger that may have an adverse effect on competition)."

IS THERE A NEED FOR ADDITIONAL MERGER CONTROLS IN ELECTRICITY SUPPLY?

In examining whether there may be some unique features of the energy industry, the Issues Paper focuses on two matters. The first of these concerns the inter-dependencies of different firms along the supply chain. As the paper correctly argues, these are covered by regulatory arrangements (ring fencing, open access, etc.) that are not, by and large, controversial.

The second unique feature to which the Issues Paper draws attention is that the product cannot be stored. This is not, strictly speaking, a unique feature since electricity shares these attributes with other products like theatre tickets, airline tickets and hotel rooms. Like electricity, the prices of these commodities tend to be highly volatile to allow for scarce supplies to be rationed and to unload a glut. The price volatility and high price excursions create opportunities for niche players either in the supply itself or in the process that results in its smoothing. As with industries like air travel, electricity's non-storable features do not provide a case for additional oversight of mergers.

Where electricity differs from other non-storable goods is:

- nearly all its balancing of supply with demand has to occur on the supply side; and

- it is not possible for supply shortcomings to be isolated -- either they do not occur or they affect a large number of customers.

These and other features of the electricity industry place it among the most difficult of markets to understand and to manage. Balancing supply and demand in both the short term and the long term is only possible by leaving the parties considerable flexibility to operate. In most respects this calls for even less bureaucratic intrusion on the industry's operations than can be accommodated in other industries.

It is sometimes maintained that the lack of consumer response to electricity pricing peaks (which can reach hundreds of fold average price levels) requires additional regulatory intrusion. Given metering limitations and the relatively small share of electricity within the overall benefits to which it contributes, almost all of the supply/demand adjustment does, indeed, take place on the supply side and this vastly increases the spot price volatility.

Integration is one consequential business strategy, alongside long term contracting, to smooth the costs to the retailer. Hence retailer-generator combinations, where they occur, are designed to reduce the risks of cost blow-outs resulting from a product sold at a fixed price but with inputs that have a potentially volatile cost.

One fear of the ACCC in seeking to oppose integration is that retailer/generator combinations will have an element of either exclusivity or discriminatory pricing and be able to extract monopoly rents. This is most unlikely however, since the vulnerabilities are in peak power provision which involves a low cost capital expense and for which there are some demand side alternatives to generator supply.

In terms of concentration of suppliers, the industry needs no further regulatory oversight than that generally applying. However, like other network industries, electricity supply has a distinct regulatory oversight need to prevent the monopoly line parts of the supply from favouring affiliates upstream or downstream. Indeed one issue that it is pertinent to examine is whether there should be restraints on mergers between distribution businesses and transmission businesses. The current cross ownership provisions between transmission and distribution in electricity specify restraints on a distributor owning more than 20 per cent of Transmission. A question not raised in the Issues Paper is whether a transmission business that serves different distribution businesses could, through overhead allocation for example, favour its affiliate over other distribution businesses.

The Issues Paper asks whether quantitative ownership measures in addition to the TPA are useful and raises the issue of whether the limitations on grid reliability may provide a reason for maintaining greater atomisation in Victoria to prevent rent extraction.

Our answer to these questions is negative. If some power -- either via an interconnector or from an older facility -- is less reliable than other power and the other power can earn a premium price, this does not represent a deadweight rent loss. It offers market signals that reward the more reliable sources of power, and if these provide sufficient reward other power sources will be incentivised to enhance their own reliability. This may be by engaging in contractual arrangements with supplementary power sources, embarking on deals with particular loads or financing a more robust interconnection. If the government seeks to enforce a more atomistic industry structure it is likely to blunt these incentive mechanisms while raising industry costs. Rent, in the way that it is described in the Issues Paper is therefore merely a profit for features that are valuable to the consumer.

Of course if the industry were to be heavily concentrated so that, say, only two firms were dominant, there may be concerns about improper exercise of market power. This is not the case in Victoria, where as illustrated in Figure 1 there are six supply sources with a capability to supply more than 5 per cent of the market.

CONCLUDING COMMENTS: WHERE WILL

THE MARKET STRUCTURE SETTLE?

The present market structure was not anticipated ten years ago at the time of privatisation. Not only was it unexpected that retailing would emerge as a separate and powerful activity within the supply chain, but the cross-ownership provisions did not originally contemplate it as a separate activity. The concerns referred to "distributors".

Since privatisation we have seen a whirlwind of corporate and ownership reorganisations in the industry. These represent attempts by owners to forge associations and synergetic structures that maximise the wealth of the entities concerned. In the process, efficiency is created. Regulatory arrangements inhibiting the ownership changes that have taken place would have had adverse effects.

As with other industries, it is unlikely that the structure of the energy market will ever settle down into a stable equilibrium. If we think of even the most mature markets like motor vehicles, we see permanent change as the assemblers juxtapose their purchasing between in-house and outsourced and as different firms merge and sometimes de-merge.

It is unlikely that there will ever be a blueprint of the ideal corporate structure in electricity supply. It is now impossible for a business to operate in a totally integrated fashion. The risks of relying exclusively on in-house generation sources are too great and would not be tolerated by retail risk managers who have to face comparisons with their peers in other businesses. Once a truly self-contained integrated supply model is abandoned, the competitive structure of the industry will, without any regulatory compulsion, result in the retail and generation functions being separated. The firms' owners will create such a split of their own volition to avoid mistrust on the part of outside parties. These parties must be dealt with at arms length so that they are assured their confidential information does not reach other parts of the business with which they compete. Hence we see, with the major private sector retailers: AGL, Origin and TXU, a similar business outcome of clear separation from related arms of the business, irrespective of whether the retailing is a totally separate firm.

Such models are commonplace in other industries, including the motor industry and other manufacturing industries that assemble components from a mixture of outside and in-house suppliers. Similar models of separation are to be seen in service industries - Qantas for example operates with several independent "silos": aircraft operations, catering, travel services, cleaning and so on. All of these contract at arms length both with sister businesses and with other firms, many of which provide competitive services to other "silos".

For electricity supply, it seems likely we will see some integrated firms, others concentrating on one function only, others seeking to nimbly pick off niche markets from the bigger suppliers. However, even if the outcome were to be an industry that is relatively concentrated with say, three major vertically integrated providers and several niche players is there a role for government to impede this? As long as the industry remains rivalrous, the answer should surely be no. To act otherwise would be likely to reduce efficiency by having relatively uninformed regulator/bureaucrats making industry structure decisions.

No comments:

Post a Comment