Address to the Australian Energy Summit

17 March 2005

INFRASTRUCTURE AND ITS RELIABILITY

The issue of infrastructure needs and reliability can be addressed in two ways. The first is to estimate how the market is developing; what sort of new investments are being made; how do consumers value different grades of reliability; where prices and generator reliability trends are heading; the likely location of new gas discoveries and the competitive environment for Australian gas here and overseas; the issues surrounding wind and other forms of generation; peak versus off peak. The list goes on. From this amalgam of needs and costs the authorities can devise the appropriate investment and other needs.

The other alternative is to ensure that we have competitive markets with secure property rights and predictably minor regulatory intrusion that allows these matters to be determined by commercial parties.

In principal, the second option is what everyone with any credibility maintains is the correct approach. We spent half a century of government intervention overinvesting in power stations, over-manning all parts of gas and electricity supply and observing a dismal outcome in terms of reliability by selecting the first option. And with the generation half of the industry, where there are multiple rival suppliers, it is self-evident that a competitive environment can prevail.

NEED FOR NEW INVESTMENT

When officials consider future investment needs in Australia, the first port of call is the NEMMCO Statement of Opportunities. Now NEMMCO is a very fine and well organised body. But it is not and does not claim to be the sort of body that will look at issues examine the various options on costs, competitive conditions and alternative approaches, line up finance and conduct feasibility studies. It is not, in short, an entrepreneur. Indeed, perhaps reflecting a public reaction to a rather alarmist SOO issued in 2003 the 2004 SOO states categorically that those looking to invest should use the SOO as nothing more than a guide.

Examining current capacity, what it is obliged to regard as the minimum level of reserves, the likely growth rates and peak levels driven by temperature ranges, demand side participation of which it is aware, the 2004 SOO arrives at the following estimates of the timing of low reserves by state.

| LRC Point | Reserve Deficit | |

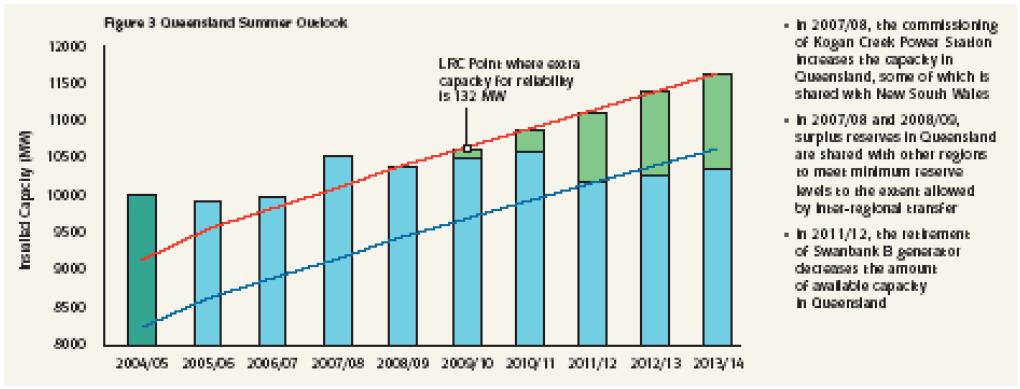

| Queensland | 2009/10 | 132 MW |

| New South Wales | 1008/09 | 157 MW |

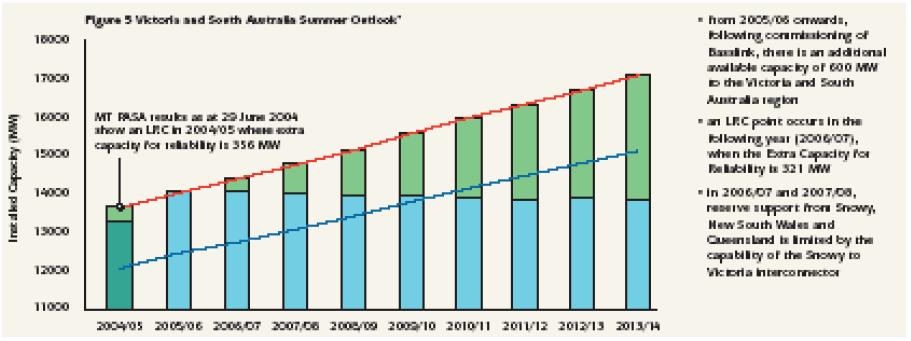

| Victoria/South Australia | 2004/05 | 356 MW |

| (combined) | 2006/07 | 321 MW |

| Tasmania | Beyond 2013/14 | - |

This says that toward the end of this decade we may need new capacity in NSW and we may need new capacity a bit before that in Victoria.

From this a more ornate demand projection is drawn. The Blue line is the median forecast at 50 per cent likelihood while the Red line is the reliability forecast, ostensibly based on a 0.002 per cent availability (that is under 10.5 minutes per year of customer interruption on average). The Green bars represent forecast extra capacity for reliability.

The most obvious question to ask about such projections is why are they made at all? Nobody has a Statement of Opportunities for bakeries, or salt mines; still less do we have them for less essential goods and services.

Of course, the answers revolve around several factors, including the long lead times for new capacity and lack of storage. Yet these are features seen with other services like telephony, air travel etc. More pertinent is whether the shared nature of electricity supply creates a situation where there is market failure. This hinges on the "free-rider" notion. It might be argued that since everyone shares in the supply availability because lines are not discriminatory between different suppliers and customers, there is a sub-optimal incentive to ensure supply is available.

Yet these externality issues are all around us within society. The economist Ronald Coase examined a great many historical examples of public goods -- those that once supplied are automatically available to all -- that are said to make it essential for government provision. He found many of them had been supplied in the past by individual enterprises. One case was the lighthouse which was seen as the archetypical type of government facility. In fact historically it was found that lighthouses were built by entrepreneurs who received payment from charges levied on ships at nearby ports. Striking and levying the perfect fee on all users was not possible, but adequate incentives to invest were in place.

So it is with electricity and gas. In the case of gas, there are well established means by which measurements of inputs and outputs can be made and the contract carriage market is the world norm. Gas has many advantages in its flexibility and we have an abundance of reserves. Unfortunately these are in the wrong place in the case of natural gas. We also have coal seem methane which is interchangeable with natural gas and which is plentiful in coastal NSW and Queensland but this is likely to remain somewhat more expensive than natural gas and will not undermine the competitiveness of coal. The key deficiencies in the present regime is the enforced open access of new gas pipelines, a regulatory requirement that almost certainly has resulted in sub-optimal new construction since it imposes greater risk on the developer than on those making use of the facility. Even so, new pipelines have been built.

For electricity, retailers need to balance their demand and supplies and act as the agent of the final consumer. They pick up the tab when the price spirals out of control and this gives them a great incentive to ensure they measure their sales correctly and contract for supplies appropriately. They perform the same essential function in the energy market as elsewhere -- they look to demand, seek to attract customers who they can profitably supply and package supply to meet their customers' needs. The outcome is signals that drive efficient market activity. These signals include the prices that attract the right form of new supply (peak, off peak etc.) They also develop prices that choke off or encourage increased demand.

Of course, all this is made more difficult in the electricity supply industry. The absence of half hourly metering at the domestic level and the price cap are among the market realities that prevent this from operating with full effect. But the question is not whether there is perfection but is their adequacy in market signalling?

One test is the outcome that has been observed. And in fact the market has kept supply and demand fairly well synchronised over the past six or seven years.

Some of this felicitous outcome might be due to government investment on noncommercial terms. But the only plausible cases of this are in Queensland and Tasmania; elsewhere we have seen market responses ensuring the gaps are filled and filled with the sort of capacity that most people thought most appropriate.

Given this history and the very prominent role of retailers who stand to lose considerably from being short where prices are rising, if the NEMMCO SOO figures are a guide we would expect to see this reflected in forward markets. NECA constructs a synthetic forward market based on the supposed actions of traders. Though the forward market shows some tightness in South Australia in the first quarters of 2005 and 2006, there is no upwards prices trend. In other words, the activities of those in the market demonstrate no urgency for major new capacity. I would maintain that NSW faces unique difficulties in attracting new investment as a result of its ideological resistance to privatisation, its government's demonstrated willingness (illustrated in the Redbank case) to tear up unwelcome contracts and its deep green anti-coal perspective. However even in NSW, there is no apparent sign of panic buying to cover positions prior to 2008.

Retailers and generators are taking the view that demand and supply are more or less in balance. And it is these commercial parties -- retailers and generators -- rather than the central agencies that are the best judges of this since it is they who have most to lose or gain if they forecast incorrectly.

REGULATORY FAILURE

The 2003 SOO was widely interpreted as heralding a series of imminent problems. These were fantasy, they stemmed from the highly conservative approach taken by NEMMCO and the agencies in each of the states to estimating demand. Unfortunately NEMMCO itself faces asymmetric incentives. It pays nothing for attempting to acquire supply over and above those available to the market but faces censure if it fails to alert jurisdictions to an impending major shortfall.

NEMMCO's track record would seem to add support to the hypothesis that it is somewhat pessimistic in its projections of supply and demand balances.

SA demand forecasts as provided to NEMMCO by the Electricity Supply Industry Planning Council of SA are as follows:

The shortfall in 1999/2000 may be attributable to some inexperience in forecasting. 2000/1 was a 1/100 year temperature peak (which the reliability standard does not seek to cover) but was met thanks to the timely arrival of Pelican Point. It is noteworthy that the level has not been reached again in the following four years. And the SOO forecast has exceeded the actual at the 90 per cent level in four successive summers. Aside from flying in the face of global warming scares, the chances of this occurring at random are 10,000 to one!

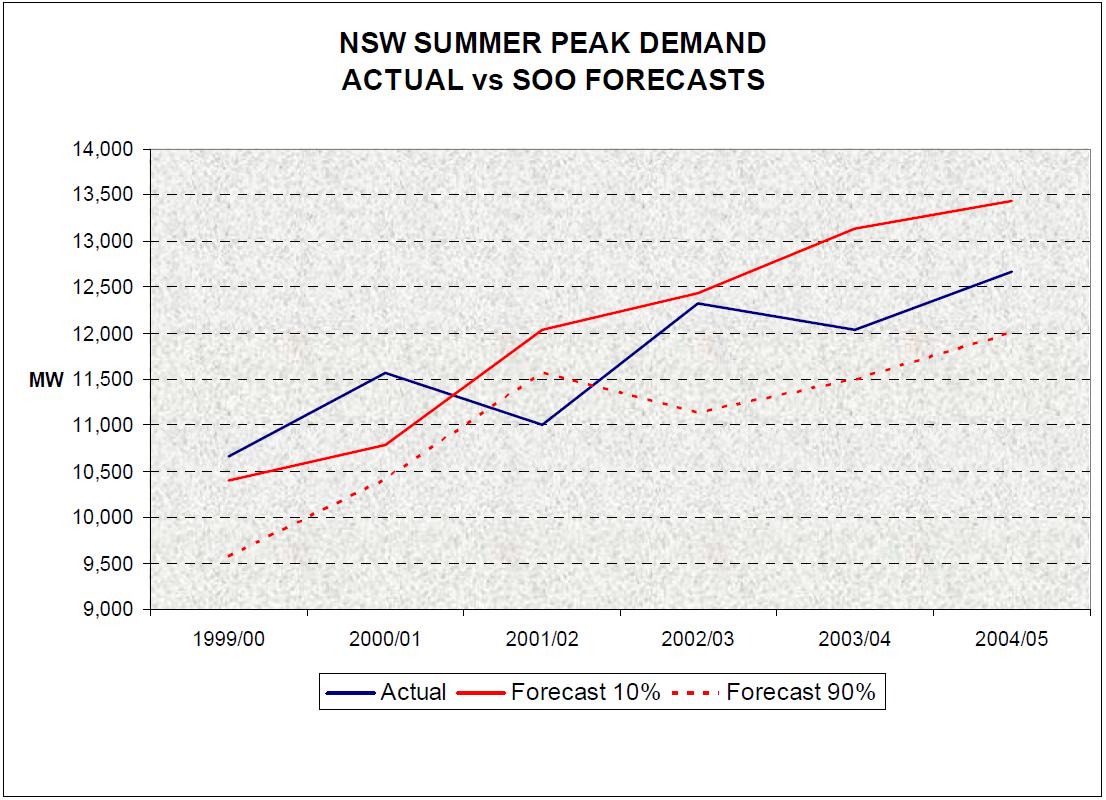

The NSW forecast has been closer to actual.

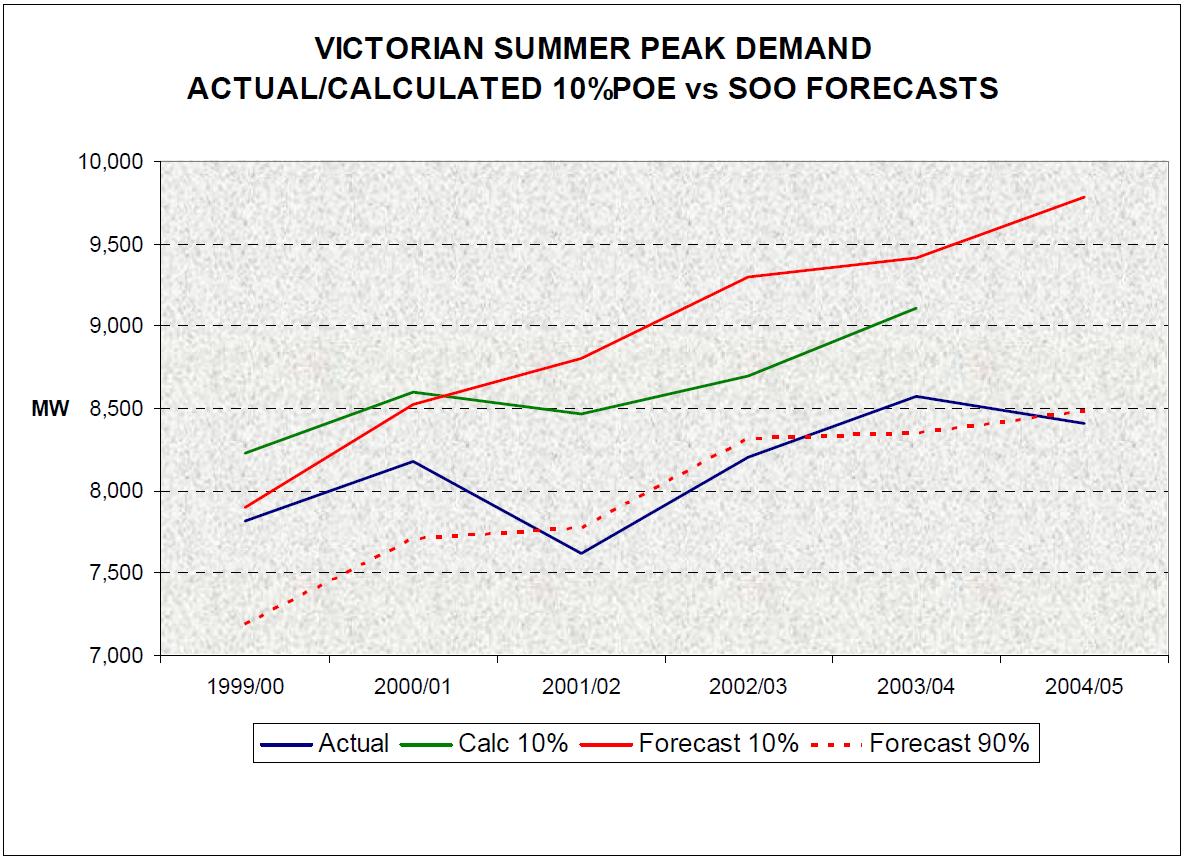

But again, Victoria has been considerably below the 10 per cent risk level and has more closely tracked the 90 per cent level.

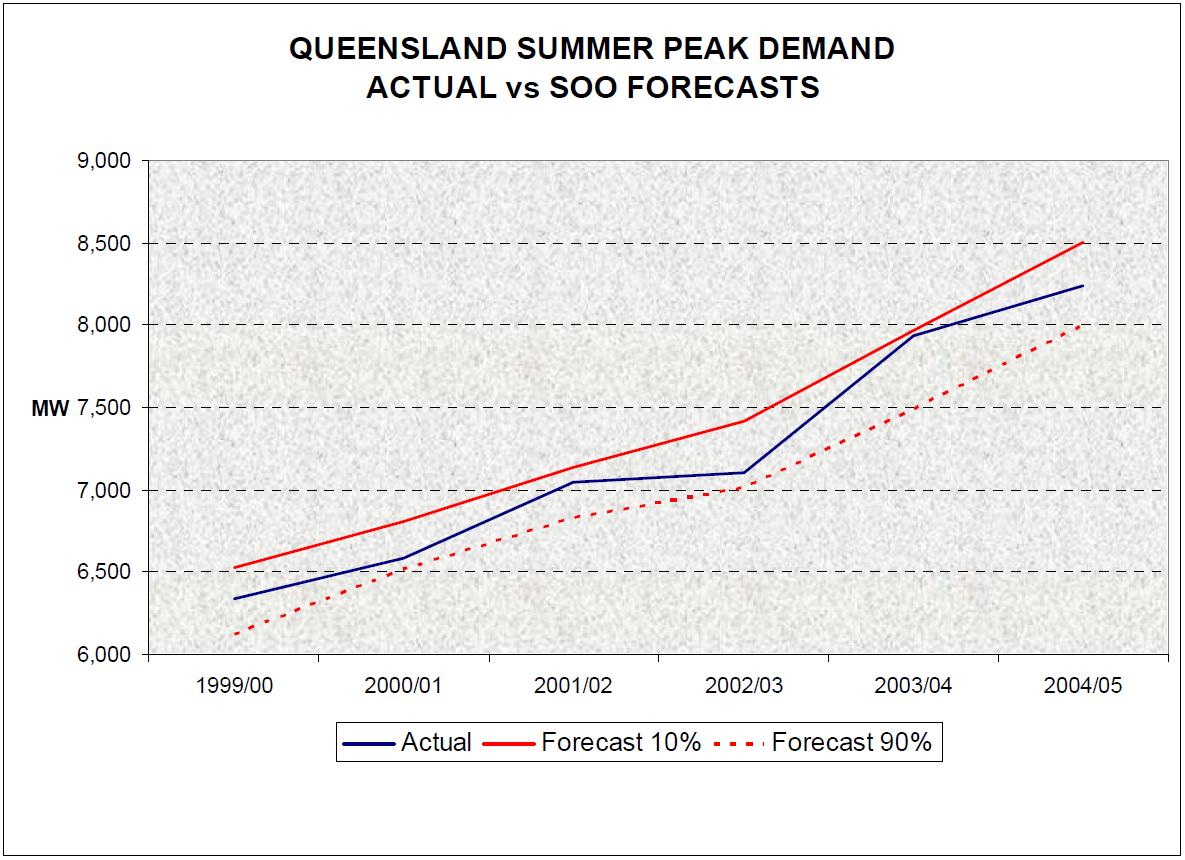

Queensland forecasts have been more accurate.

If Ministers are confronted with publicity that a failure in the electricity supply is a strong possibility, they are likely to act in manner that could backfire on long term market stability. A danger is that governments will be panicked into taking precipitate action that will undermine the markets.

Such action can take many forms:

At its mildest it is jawboning and undertaking pre-feasibility studies at below real cost as the NSW Government is already doing

- At one extreme it might entail the government building new government plant or requiring one of its retailers to sign a long term contract for new capacity. But in hiving off a part of the demand in this way, the viability of the non-contracted suppliers is reduced -- they face a lower price for their product and this can set in train a vicious circle whereby no new plant is introduced unless it receives privileged prices. The outcome is a return to central planning.

Other measures involve different types of capacity charge, which are attractive to Ministers who focus on the public goods nature of electricity but which do not appear to be as low cost as the energy only market we presently have. The pre-NETA UK system had a payment based on Loss of Load Probability times VoLL. Capacity markets mean a regulator determining what the right capacity is and who has capacity and how much they should be paid for it. It is only conceivably useful if it provides a signal some years out rather than in near time periods and designing this is especially difficult. It comprises a series of interventions in commercial parties' decision frameworks. Among the deficiencies of this is a muting of the market for reliability -- for example in the demand side bidding. It also leads to pressures to cap energy bids in ways that prevent prices from providing commercial returns. We have shown that an energy only market allows capacity to be created without such interventions while those markets that have had a separate capacity payment have often found this to be unsatisfactory (it reached almost one quarter of returns in the England and Wales markets but in New England was almost always valued at zero).

A less costly outcome of over-forecasting demand is the activation of the Reserve Trader to supplement supply. As NEMMCO has no facilities, to do this it must use plant that is already available, if mothballed. To the degree that such plant is needed, we are likely to see higher prices on both spot and contract markets and it would, if the market shares the NEMMCO view of the future, be made available in any event. On this line of reasoning, the Reserve Trader provisions are irrelevant since the capacity made available is phantom capacity that would have otherwise been contracted or made available for trading on the spot market.

However, there is a likelihood that the price would be higher from the contracting (otherwise the suppliers would have preferred to have left the capacity available for spot trading or contracted with genuine customers at a lower price) and there is strong evidence that at least some of the capacity made available would not have been had the Reserve Trader not been activated. This appears to have been the case with the Ecogen facilities in 1997. In such cases, unless the market is failing in some way, the costs are higher -- eventually to customers.

Operating the Reserve Trader last year sought an additional 300 MW capacity for Victoria/South Australia but only managed to contract about 80 MW on terms that it considered to be acceptable. All of that might have been available in any case, and the contracts represented therefore people who would otherwise have been operating in the spot market, as the Smelter Trader does when it plays with about 200 MW. With the delay in Basslink, NEMMCO might once more seek additional supplies for 2005/6.

Following the 2003 SOO where considerable publicity was given to a NEMMCO picture widely interpreted to offer cause for concern, the National Generators' Forum contracted ROAM to undertake a modelling of the situation using the NEMMCO "reserve margin" against the Reliability panel's "unserved energy approach". Roam came up with the following, which might bear out the suggestion that NEMMCO is overconservative. In fact, NEMMCO has since moved to apply a less stringent interpretation of its required approach which can be seen in some closer correspondence with the ROAM analysis for 2004. In some cases this is also caused by new plant being committed.

First Season Where Reserve Standard is Breached

| SOO 2003 | ROAM Modelling of NECA methodology | SOO 2004 | |

| Queensland | Summer 2005/6 | Summer 2007/8 | 2009/10 |

| NSW | Summer 2005/6 | Summer 2008/9 | 2008/9 |

| Victoria | Summer 2003/4 | Summer 2009/10 | 2006/7 (1) |

| SA | Summer 2003/4 | Summer 2008/9 | 2006/7 |

RISKS OF INADEQUATE SUPPLY AND NETWORK EXPANSIONS

As far as generation is concerned the key risks are that government action will mask the signals and eventually result in a supply shortfall.

- One of these I have already mentioned in passing stems from the NSW Government's actions in discouraging private sector new generation. Creating sovereign risk through welching on contracts by arranging for a gaggle of green activists to protest is no way to encourage new private sector investment. And that Government in its Green Paper maintains that it would be most reluctant to have new capacity built other than by private sector participants. Certainly in the case of coal power stations -- and it is unlikely that other forms would prove as competitive -- some form of sovereign guarantee would be necessary before a firm or its bankers were to embark on a new facility.

- Staying with NSW, the mandatory insurance system or ETEF, provides a weaker incentive for retailers to ensure that they are forecasting market demand accurately since the government has eliminated risks of failing to do so accurately. This may bring mistakes and unexpected demand shifts.

- Similar threats can emerge in other states if the retail price caps are kept below market levels. This is however an area where governments in Victoria and SA have managed to control their propensities to intervene and are allowing prices to shift market levels. NSW however retains very low allowable retail margins which seriously restrict competition.

- Another risk, very much in the spotlight at present, is that regulators will offer inadequate incentives for expansions and optimal maintenance. This may have been a feature of the fragility of distribution networks, especially in Queensland where the regulator demanded a 17 per cent cost saving of Energex. It is doubtful that it was a feature of the 14 March 2005 failure of the line through Heywood to South Australia which operates to a high degree of reliability but is not designed to be 100 per cent available.

- Interventions favouring subsidised and uneconomic generation can suppress demand which means reduced new investment especially in the sort of energy intensive industries that Australia is well placed to win. The various schemes like MRET and NGAC add costs to industry and in the case of NSW, mean that some 23 per cent of electricity is now slated to be subsidised (2); this probably rules the state out of consideration for major new energy intensive industry. Less draconian measures are in place in other states -- Queensland has its 13 per cent gas requirement and Victoria was less than firm in controlling its state financed green groups who campaigned to prevent the Hazelwood expansion; nor has the state made a wise choice in its appointment of a relatively activist Presiding Judge to the Land and Environment Court whose legal interpretations prolonged the case and added expenses.

- Some private sector generation businesses claim that the new capacity building by the Queensland government is not based on commercial principles but are being subsidised indirectly by a government intent on using its cheap coal as an industry development tool. Though subsidised plant adds to capacity in the first instance, each new tranche of it considerably reduces the incentive of commercial parties to seek out opportunities to build plant in line with market requirements. Subsidised plant puts us on the slippery slide to total government ownership or control of the industry.

- Much the same risk has in the past been offered by subsidised transmission. If a power station is stranded by low cost power being brought in from elsewhere it suffers lower than expected returns. If this is due to it being stranded as a result of government regulations that effectively subsidise costs, damage is done to the market's automatic ability to supply demand.

- Finally, there remains the risk of other interventions. I think we have finally thwarted the rebidding demon which, by requiring generators to bid "ethically" and constraining their abilities to respond to sudden emergency issues, would have gummed up the bidding system and created costs and uncertainties. Price suppressing mechanisms like those proposed tend to blunt the signals about scarcity and they reduce the abilities of investors to obtain recompense on their outlays. Market power is a transitory phenomenon in the NEM and preventing any attempts to exercise it means reduced revenues and dangers to the investment incentive.

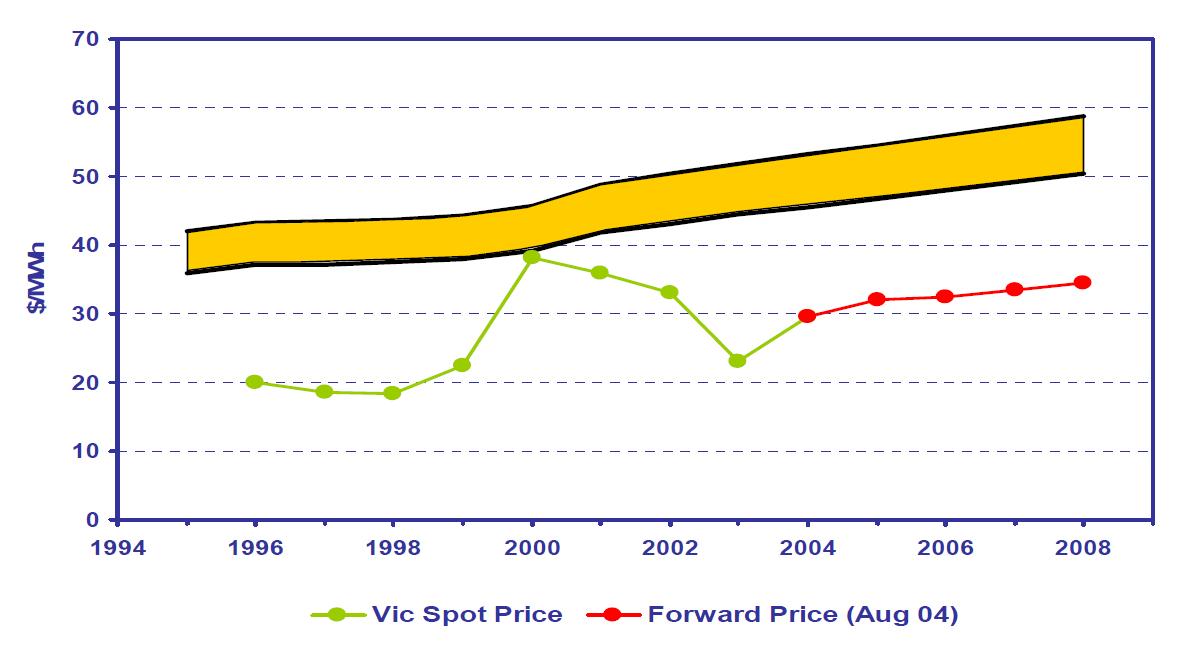

The message is that the real dangers to the supply industry in both gas and electricity in Australia are those stemming not from too little government but from too much. The industry has expanded and maintained low costs in the six years it has been operating. The price levels in Victoria compared to those expected at privatisation are shown below.

Where issues have arisen, government has often exacerbated them, as with the excessive level of enforced rationing in Victoria in 2000 following industrial relations problems. Similarly, the competing commercial parties managed the South Australian gas crisis of January 2004 following the loss of the Moomba pipeline and government intervention that mandated particular outages in particular plants probably meant the available gas was used sub-economically.

The recent loss of the main Heywood link to South Australia has brought calls for additional infrastructure spending to provide absolute reliability. There may be a case for this but governments also need to be made aware of the second and third round effects of actions that in the first instance seem to shore up and to cheapen supply.

Governments have a tremendous capacity to cause major disruptions in the market and add major costs to customers. In many ways the longer we have the present period of policy drift with the MCE, the less likely are we to see poor regulatory interventions.

ENDNOTES

1. SOO 2004 predicted reserve shortfalls from 2004/5 in SA & Vic, triggering Reserve Trading. Basslink was expected to shore up reserves in 2005/6, with a reserve deficit returning in 2006/07.

2. This is based on the NGAC requirements of a maximum of 52,000 kilotonnes of CO2 emissions by 2010 and business-as-usual emissions assuming 2% annual growth at 68,400 kilotonnes in that year.

No comments:

Post a Comment