Backgrounder

INTRODUCTION

Regulation is a political activity. It sets the framework for the market economy by defining the boundaries between private action and government action. It is, since the failure of overtly socialist models of political economy, the primary method by which the government relates to individuals and communities.

Regulations, and the regulatory agencies which administer them, cast an increasingly large shadow over the freedom to interact, both economically and socially, in Australia.

The first part of this Backgrounder looks at the rapid growth in regulation-making, and the recent institutional changes in Australia's regulatory agencies. It charts the consolidation and expansion of the three major economic regulators -- the Australian Competition and Consumer Commission (ACCC), the Australian Prudential Regulatory Authority (APRA) and the Australian Securities and Investment Commission (ASIC) -- and examines the theoretical justifications for constructing such "mega-regulators".

The second part attempts to explain how these mega-regulators are themselves able to encourage their own growth. It looks at the internal pressures towards regulatory and institutional expansion, as well as the political pressures which the agencies themselves are able to exert upon directly elected politicians.

Table 1: Pages of Commonwealth Acts of Parliament passed per year, by decade

| Total Pages | Average per Act | |

| 1900s | 1,072 | 6 |

| 1910s | 1,195 | 3 |

| 1920s | 1,515 | 3 |

| 1930s | 2,530 | 3 |

| 1940s | 2,795 | 4 |

| 1950s | 5,274 | 6 |

| 1960s | 7,544 | 6 |

| 1970s | 14,674 | 9 |

| 1980s | 29,299 | 17 |

| 1990s | 54,573 | 31 |

| 2000-2006 | 40,266 | 35 |

REGULATION AND REGULATORY AGENCIES:

GROWTH AND CONSOLIDATION

REGULATION IS INCREASING

The most striking feature of the overall level of regulation and of the regulatory burden in Australia is its growth over time.

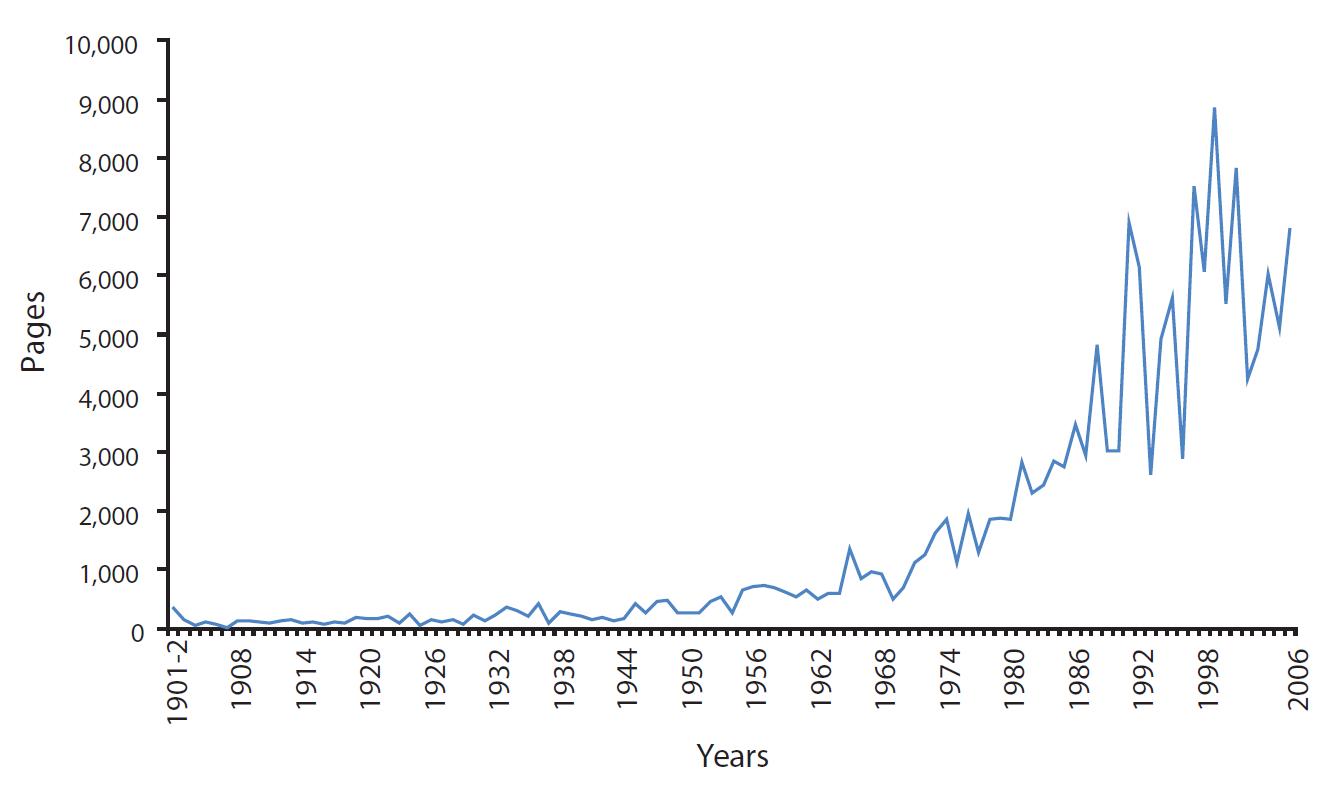

Legislation is wider in scope and content than regulation, but it can serve as a useful proxy. Chart 1 depicts the growth in Commonwealth legislation since Federation, by looking at the number of pages of Acts of Parliament passed per year.

Chart 1: Pages of Commonwealth Acts of Parliament passed per year, 1901-2006

While the growth in legislative activity has been sustained over time, it is interesting to note the dramatic increase over the past few decades. For instance, if we mark the year 1980 as the beginning of the reform period in Australia, through 2006, more than five times the number of pages of legislation than it had in the eight decades preceding it.

Furthermore, as Chart 1 reveals, it is striking how little legislative activity was required at the time of Federation to unify the country -- 358 pages, spread over two years -- compared with how much it takes to manage the Commonwealth in 2006 -- a massive 6,786 pages.

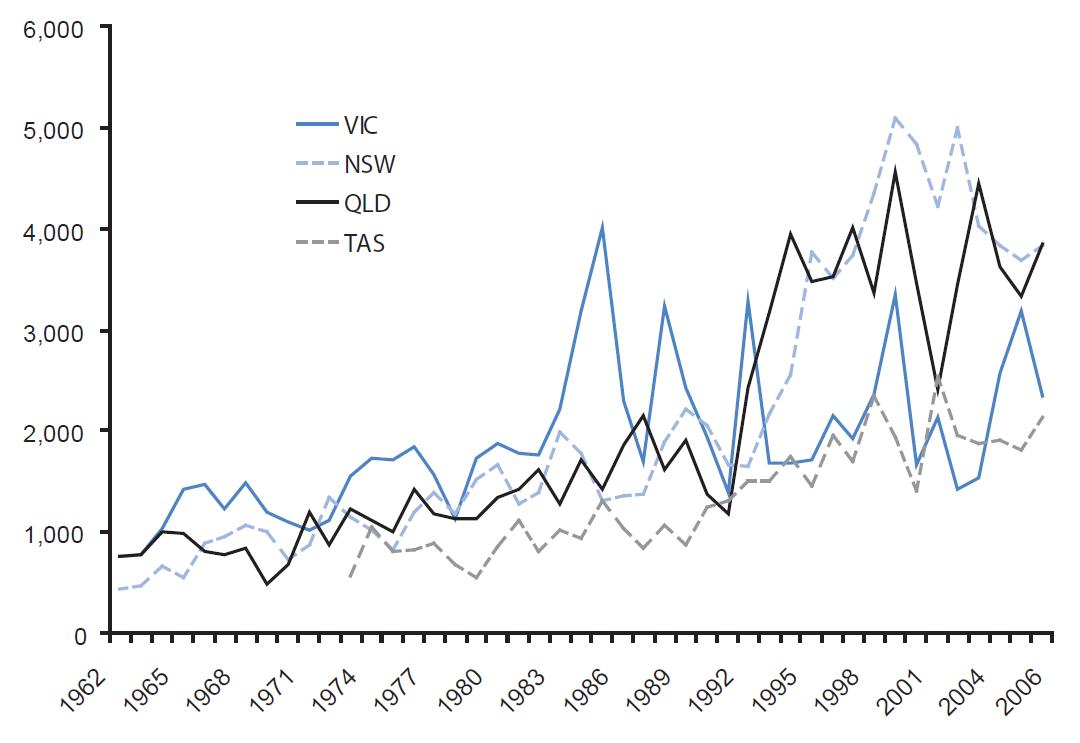

Certainly, the changing nature of Australia's federal structure has significantly expanded the jurisdiction of the Commonwealth legislature, but there have been similar increases in State legislative activity -- not decreases, as would be expected if there had simply been a shift in responsibility from the States to the Federal government.

State legislation has also been marked by significant growth. Charts 3–8 illustrate legislative activity over the past 40 years in Victoria, New South Wales, Queensland, Tasmania, Western Australia and South Australia respectively.

Chart 3: Pages of legislation passed per year, Victoria, 1958-2006

Chart 4: Pages of legislation passed per year, New South Wales, 1959-2006

Chart 5: Pages of legislation passed per year, Queensland, 1962-2006

Chart 6: Pages of legislation passed per year, Tasmania, 1968-2006

Chart 7: Pages of legislation passed per year, Western Australia, 1959-2006

Chart 8: Pages of legislation passed per year, South Australia, 1959-2006

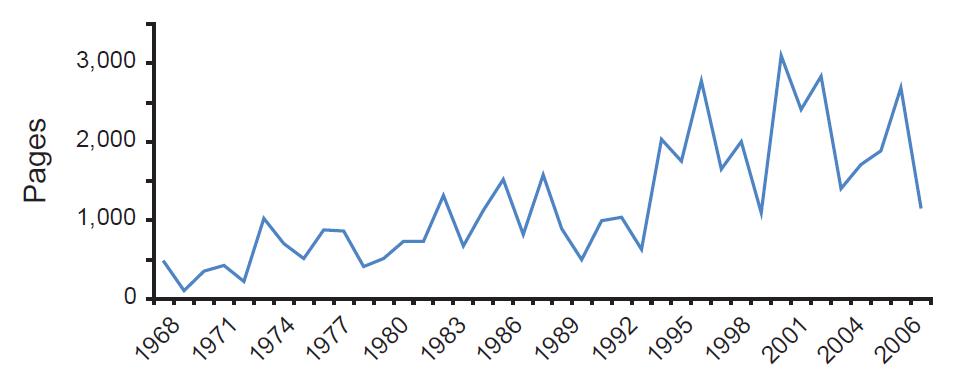

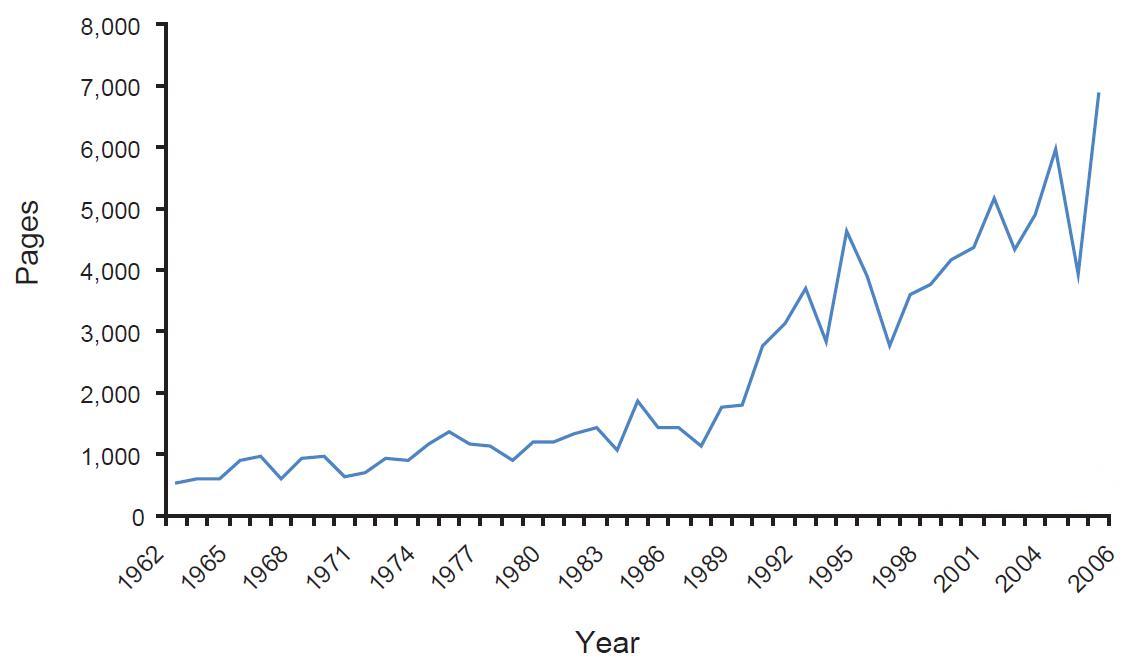

What data is available indicates that subordinate legislation -- regulation -- is growing at a similar pace as legislation. Charts 9 and 10 show how the increase in subordinate legislation in the Commonwealth and the States parallels the increase in total legislation over the last 40 years.

Chart 9: Pages of new Commonwealth subordinate legislation, 1962-2006

Chart 10: Pages of new state subordinate legislation, 1962-2006

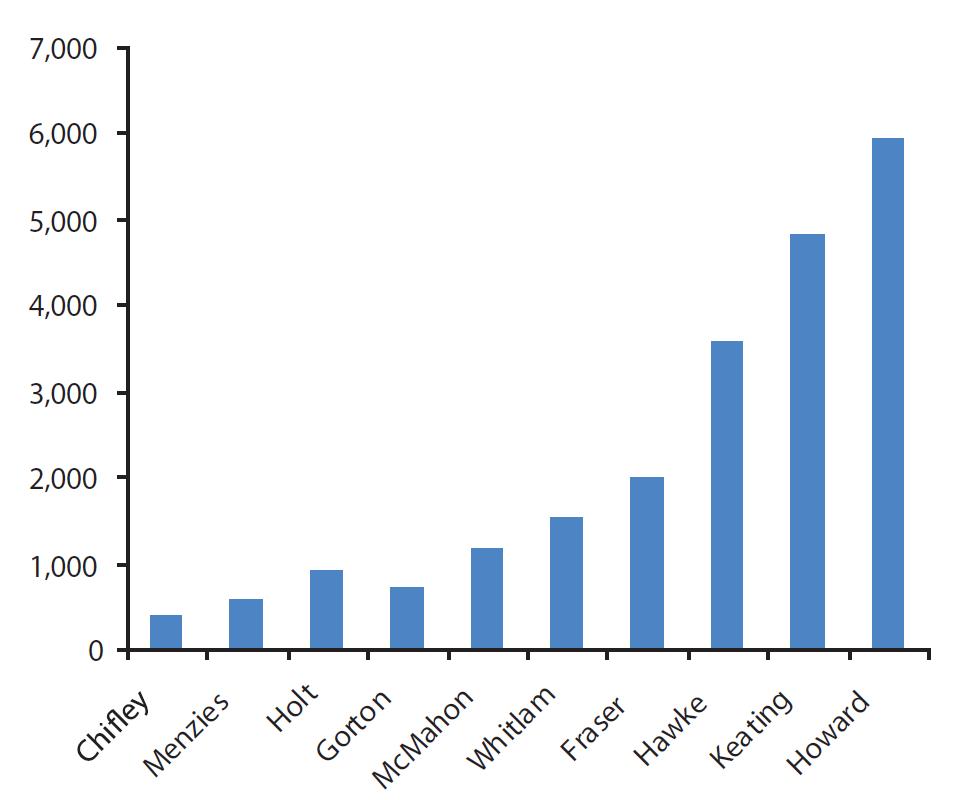

Chart 2 reveals an interesting aspect of this increase. Legislative activity is government independent -- changes in government have little effect on the legislative activity. For this reason, Chart 2 illustrates how the Coalition Government under Prime Minister John Howard has been the highest legislating government in Australia's history. A similar analysis is possible with data on regulation cited in Chart 9 -- the Howard Government has overseen the largest regulatory expansion since Federation.

Chart 2: Average pages of Commonwealth Acts of Parliament passed per year, by government

For the firms and individuals effected by regulatory and legislative increases, the impact is cumulative. Individuals not only have to act in accordance with the legislation and subordinate legislation passed in any given year -- they also have to contend with the entire body of law as amended. Some of this legislation and regulation replaces existent law; but it is clear that it is growing -- if not at the same heady pace that legislation and regulation in general is being passed.

One potential cause of the increase in activity is the move during the 1980s to the use of plain-English drafting -- as opposed to the traditional legislative language inherited from England in the nineteenth century -- as well as the use of double-spacing. (1) Formatting changes can alter the words-to-page ratio. Tasmanian legislation in its consolidated form has been published from 1996 on a larger paper format, but with an increase in white space. Similar changes have occurred in South Australia and Queensland.

Nevertheless, there is little to suggest that the plain-English drafting reform or formatting changes are the sole, or even primary, cause of increasing legislative activity -- the increased activity both preceded the reform and continued after it had filtered through the various tiers of government. Technical changes in the manner in which legislation is drafted cannot explain modern legislative and regulatory excess.

Anecdotal evidence also suggests that regulatory activity is spiralling ever-upwards. The Federal Government's 2006 Taskforce on Reducing the Regulatory Burden on Business noted that a particularly striking example of the level of regulation was the 24,000 different types of licences administered by the three levels of government. (2)

Much of the increased regulatory burden is not sector-specific, but is related to workplace law. The Australian Construction Industry Forum nominates recent changes to industrial relations and occupational health and safety law as a significant addition to the regulation facing its industry, as well as taxation changes. (3) Indeed, the Income Tax Assessment Act is often used as a barometer of legislative and regulatory growth. It has grown from 120 pages in 1936 to more than 7,000 pages today.

The Insurance Council of Australia attempts to describe the level of regulation affecting its industry by noting its effects on business structure and practice. Regulatory compliance now comprises between ten and 25 per cent of board and senior management workload. One large insurer estimated a much higher workload, at least 40 per cent of senior executive time, and up to 60 per cent of board time. (4) One small insurer estimated that the compliance burden had grown five-fold since five years ago, and ten-fold since ten years ago. Another insurer estimated that compliance expenses as a percentage of operating income had more than doubled in the last five years. Another estimated that the staff numbers in regulatory compliance committees had grown by 20–30 per cent in the last two years up to 2005. (5) A PricewaterhouseCoopers analyst has noted that, for the insurance industry over the last five years, the cost of complying with the prudential regulatory framework has increased significantly. (6)

The Credit Union Industry Association notes that the burden on both its credit union membership and other banks and building societies has increased since the Wallis Inquiry, due to the mandatory implementation of Basel II, recent Financial Services reforms, changes to prudential standards, and the adoption of international accounting standards. (7) An example of this increase is provided by the Business Council of Australia: a total of 227 pages of documentation need to be given to a customer in order to open a simple cheque account with an overdraft limit and home loan, roughly five times the number of pages in 1985. (8) The Australian Bankers Association reports that one bank has doubled its annual compliance expenditure levels every five years since 1994–95, with a similar growth in staff dedicated to regulatory compliance. (9)

Telstra notes that the number of regulatory instruments applicable to its business has grown since 1997 from 20 to 348, (10) and that the number of reports required by the ACCC have been increasing by two to three each year. (11)

There has been little quantification of the extent of local government regulatory activity, but there are indications that it, too, is increasing. The Australian Chamber of Commerce and Industry writes that there has been a marked upswing of local government regulation as a constraint to investment between 2003 and 2005. (12)

Some of these anecdotal impressions of the regulatory burden may even understate the economic impact of regulation, by focusing inordinately on the paper-burden cost, rather than the total regulatory cost. Paper-burden costs typically constitute one-third of the total cost of regulation. (13) These costs include the cost of employees dedicated to regulatory compliance, and external legal, economic, and financial consultants.

Rapid legislative and regulatory activity imposes its own costs. The enormous amount of regulatory change since the 1996 Wallis Inquiry has added substantially to the administrative burden of the insurance industry, for example. (14) Furthermore, a by-product of rapid activity is widespread uncertainty, which has the effect of depressing investment and economic activity.

But the contemporary political focus on "red tape" presents the problem of over-regulation in a narrow light. The structure of regulation is so central to some firms' business models and profitability that regulatory governance and compliance is an "all-of-firm" question. For these firms, it is not easy to separate regulatory compliance costs from business costs. (15) The anecdotal estimates above, which focus predominantly on the easy-to-measure paper-burden costs, are likely underestimations of the total costs for many industries.

The full cost of regulation is much greater than the visible cost of compliance. Certainly, the distribution of costs brought about by regulation varies by industry. In the food sector, the primary cost of regulation is a paper-burden cost. But for much of the economy, the paper-burden cost is dwarfed by the restrictions on economic activity imposed by the regulations. For instance, the "chilling effect" of access regulation far outweighs the paper-burden cost of those regulations by holding back infrastructure investment. The cost of investment forgone is much harder to quantify, but a much more significant burden than the paper-burden.

As Gary Banks argues, "regulations not only create paperwork, they can distort decisions about inputs, stifle entrepreneurship and innovation, divert managers from their core business, prolong decision-making and reduce flexibility". (16) These effects are, on average, far more significant than the red tape which is required by regulators to assess compliance. Focusing only on paper-burden costs is like focusing on the time spent filling out a tax return rather than the amount of tax paid. Political platitudes to lower the red tape burden offer little, at least if they are not part of a general push to decrease overall regulatory intervention in the economy.

It would be a mistake to limit the analysis of regulation to the regulatory paper-burden. Nevertheless, the increases in the compliance cost of regulations can provide a rough proxy for the increases in the regulatory burden across the economy.

REGULATORY AGENCIES ARE GROWING

Another method by which we can attempt to measure regulatory growth is by looking at the structure and size of the regulatory agencies themselves.

There are approximately 60 Commonwealth regulators and national standard-setting bodies. (17) There are a further 40 Federal ministerial councils which set and administer regulations. Although hard to estimate, Federal regulatory agencies employ over 34,000 people, with a combined yearly budget of well over $4.5 billion.

The Victorian Competition and Efficiency Commission identified 69 regulatory bodies in that State, with a combined budget (excluding the Metropolitan Fire Brigade, Country Fire Authority and Parks Victoria) of over one billion dollars per annum, and a staff of 6,895. (18) The Productivity Commission extrapolates these figures to come up with an estimate of 600 regulatory agencies across the country. Extrapolating that figure, and taking into account government departments with regulatory functions, ministerial councils, inter-governmental bodies, and the range of quasi-official agencies and boards, it is likely that nationwide at least $10 billion is spent on regulating the Australian economy annually.

Using the number of staff as a proxy of agency size, many of the agencies have experienced significant recent growth. For instance, the Australian Fisheries Management Authority has nearly doubled in size in the last decade, from a staff of 100 to 186. Staff numbers at Food Standards Australia New Zealand have increased by 50 per cent, from 100 in June 2000 to 146 in 2006. Staff at the The Australian Pesticides and Veterinary Medicines Authority has increased in that same period from 113 to 133.

In Victoria, the Office of the Chief Electrical Inspector had grown from a staff of 35 in 1999 to 59 in 2005, when it was merged with the Office of Gas Safety to become Energy Safe Victoria with a staff of 89. The Victorian Building Commission has increased its staff to 111 from 81 in 2002. The Essential Services Commission has increased from 34 to 62 since 2001. In New South Wales, the Independent Pricing and Regulatory Tribunal has more than doubled in size in the past decade, from 32 in 1997 to 73 in 2006. (19)

AGENCY CONSOLIDATION AND THE "MEGA-REGULATORS"

There is a large variety of regulatory agencies dedicated to regulating specific industries, such as the federal Civil Aviation and Safety Authority or the Australian Fisheries Management Authority.

Table 2: Resources of selected Australian Government regulatory agencies in 2004-05

| Agency | $'000 | Staff |

| Australian Customs Service | 1,026,351 | 5,572 |

| Australian Maritime Authority | 71,925 | 247 |

| Food Standards Australia New Zealand | 18,967 | 146 |

| Australian Prudential Regulation Authority | 95,052 | 570 |

| Australian Securities and Investments Commission | 217,967 | 1,471 |

| Civil Aviation Safety Authority | 120,547 | 672 |

| Australian Pesticides & Veterinary Medicines Authority | 21,263 | 133 |

| Australian Taxation Office | 2,525,935 | 21,511 |

| Australian Competition and Consumer Commission | 84,168 | 596 |

| Australian Communications and Media Authority | 73,799 | 500 |

| Australian Fisheries Management Authority | 43,162 | 186 |

| Australian Quarantine and Inspection Service* | 290,000 | 2,800 |

| Total | 4,589,136 | 34,410 |

*Data from 2003-04

Source: Annual reports.

Adopted from Productivity Commission, Regulation and its Review, 2004-05

But occupying a central role in Australia's regulatory system are a few key economic regulators with economy-wide scope. Rather than being confined to narrow jurisdictions, typically these agencies not only regulate a wide variety of industries, but are also multi-dimensional in scope. That is, Australia's major economic regulators regulate for both economic and social outcomes, as well as undertaking technical regulation such as standards setting. These regulators are not built around the institutions that they administer, but rather are built around "functional" lines. (20) For example,

- the Australian Securities and Investment Commission (ASIC) is responsible for consumer and investor protection;

- the Australian Prudential Regulatory Authority (APRA) is responsible for prudential regulation; that is, market failure associated with information asymmetries in financial contracts; and

- the Australian Competition and Consumer Commission (ACCC) is responsible for policing anti-competitive behaviour economy-wide.

Functional regulation is said to be more suitable for economic systems that are highly complex, and when the boundaries between industries are blurred. With jurisdiction across the economy, functional regulators are able to identify similar characteristics in firms from different sectors and regulate appropriately. (21) In an "institutional" or industry-centric regulatory system, firms may avoid regulation by engaging in activities in which the regulator may not have specialist expertise to regulate, or the regulator may develop standards which contradict those of other regulators.

Some academics have argued that institutional regulation, by "siloing" off industries into distinct and separate categories, is more resistant to possible "runs" of risk across industry sectors, (22) although there has been some evidence to suggest that adopting a functional approach to financial regulation in Australia has not been harmful in this way. (23)

This Backgrounder looks specifically at the three major functional economic regulators, the ACCC, ASIC and APRA. However, it is worth noting that the Australian Communications and Media Authority and the Reserve Bank of Australia are also major economic regulators. Furthermore, both the Australian Taxation Office and the Australian Customs Service also have substantial regulatory powers.

THE WALLIS INQUIRY, 1997

The 1997 Financial System Inquiry ("Wallis Inquiry") was only the third major inquiry into the Australian financial system since Federation, after the 1936 Royal Commission and the Campbell Inquiry in 1981. After the "four revolutions" which followed the Campbell Inquiry, the financial market and its structure went through a dramatic overhaul, with the introduction of new institutions such as foreign exchange firms, recognised bond dealers and new types of trusts and management funds, as well as entrance into foreign exchange markets and new secondary mortgage markets. (24) In the decade between 1985 and 1995, the number of commercial banks in Australia increased from 13 to 49. (25)

Chart 11: Agency consolidation

The purpose of the Wallis Inquiry was to assess the appropriateness of the regulatory framework which had been constructed during the period of financial deregulation in light of these changes. The "modest trend" towards agency consolidation internationally was noted in the Inquiry's discussion paper -- the Inquiry predated the now proto-typical example of an "all-in-one" regulator, or "mega-regulator", the United Kingdom's Financial Services Authority (FSA).

Governance and the concentration of power were factors for the participants of the inquiry when recommending the ideal regulatory structure. The Inquiry rejected a proposal to amalgamate existing financial regulators into a "mega-regulator" on the grounds of efficiency and specialisation. The Inquiry was concerned with regulatory governance, writing that a single regulator may become "excessively powerful". (26)

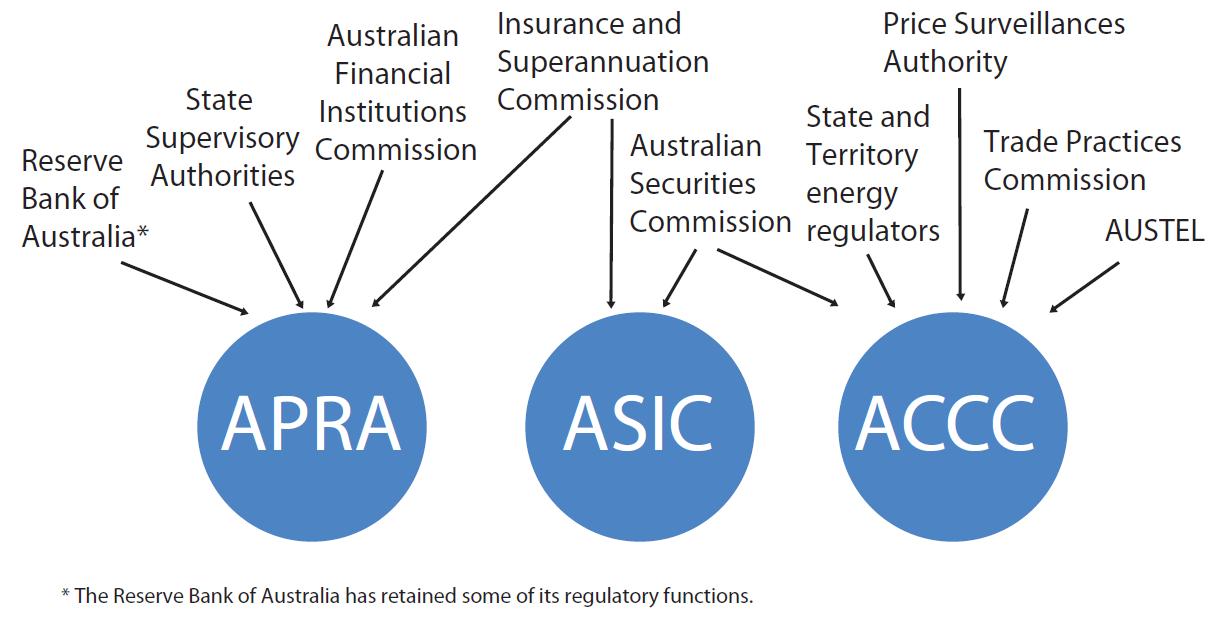

But, nevertheless, the Wallis Inquiry's final recommendations, as adopted by the government, consisted of major agency consolidation into two main organisations: the Australian Prudential Regulatory Authority (APRA) and the Australian Securities and Investment Commission (ASIC). This model was popularly known as the "twin peaks" model, from a 1995 article which recommended delineating financial regulation according to function -- prudential (APRA) and disclosure (ASIC). (27) Advocating this consolidation of agencies, Treasurer Peter Costello wrote ahead of the Wallis Inquiry:

The regulatory framework is hopelessly out of date. You have superannuation funds that are now in home lending and are essentially running banks and you have banks coming into superannuation -- you have got different institutions offering the same product, different regulators regulating the same product because they are offered by different institutions. Why do not we cut all that away and say whatever the nature of the financial institution we will have a regulator covering prudential and a regulator covering consumer protection and we can sweep a whole lot of that away? (28)

Although the "twin peaks" model amalgamated regulatory functions in a less centralising manner than the United Kingdom's FSA, it was, nevertheless, a significant consolidation of regulatory power. By drawing the vast bulk of regulatory functions away from the Reserve Bank of Australia (the bank did gain some of the roles then played by the Australian Payments System Council), the new model eclipsed the international consolidations described in the Inquiry's discussion paper. It is not inaccurate to refer to the new tri-regulator model as a system of "mega-regulators", even if the FSA provides a more "pure" example of such an institution. The result of the Wallis Inquiry was the creation of two functionally-structured mega-regulators with economy-wide jurisdiction.

AUSTRALIAN PRUDENTIAL REGULATORY AUTHORITY

Before the Wallis Inquiry, prudential regulation was structured institutionally -- a framework which emphasised the differences between the regulated institutions rather than the similarities. The Insurance and Superannuation Commission (ISC) regulated insurers and superannuation funds. The RBA regulated the banking sector. The constitutional division between the Commonwealth and the States had resulted in regulatory authority for building societies, friendly societies and credit unions residing in the eight State-based "State Supervisory Authorities" (29) and the federal Australian Financial Institutions Commission (AFIC).

Under the post-Wallis Inquiry reforms, APRA, as a functional regulatory agency, has assumed prudential regulation of finance-based industries. It required eleven pieces of legislation, which constituted over 4,000 pages, including four new Acts and two omnibus Acts. In total, APRA's foundation amended and repealed more than seventy existing Acts. (30)

APRA absorbed the ISC entirely, as well as roughly seventy staff from the RBA with bank regulation roles.

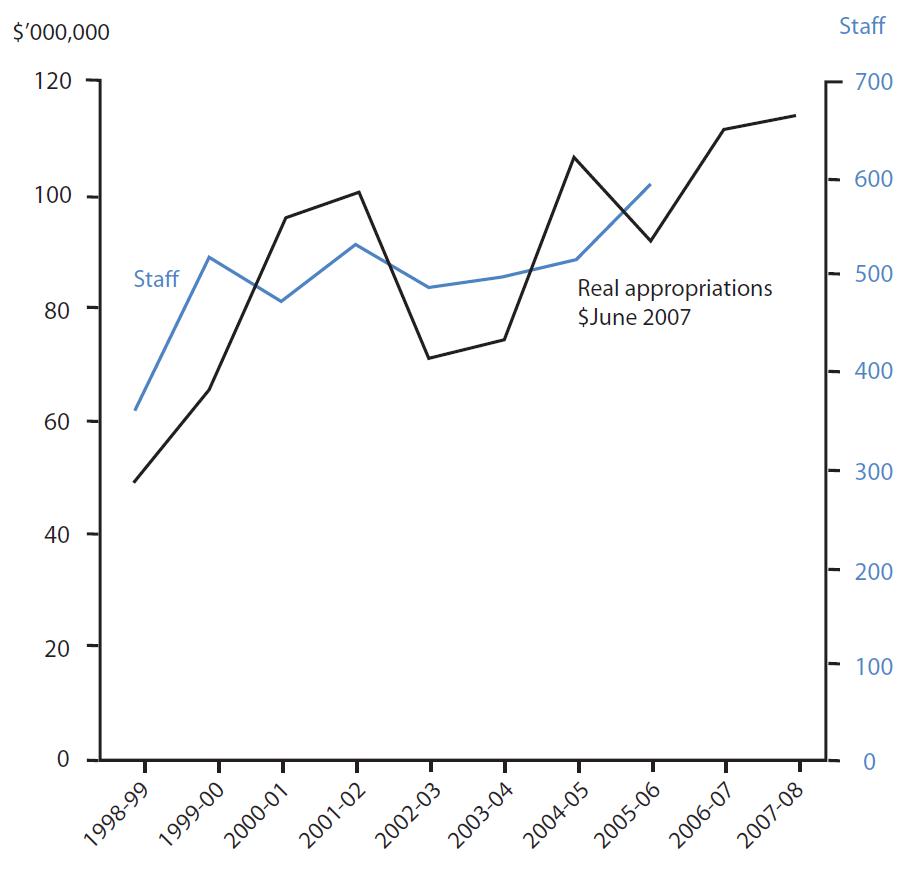

Chart 12: APRA, Staff and Annual Appropriations, 2000-01 to 2007-08

Source: Staff: APRA Annual Reports. Appropriations: Commonwealth Budget Papers

The agency has since experienced rapid growth, from a staff of roughly 400 at the time of transition to 570 in 2006. The annual federal appropriation for APRA has grown 50 per cent, to a budgeted $92 million in 2006–07.

In addition to the legislation which founded APRA, the prudential regulator has overseen more than 66 major regulatory changes since 2000. (31) In 2007, APRA regulates more than 1,900 entities (excluding small APRA funds). (32)

For the insurance industry, the creation of APRA represented a significant increase in the regulatory activity covering the sector. Under the ISC, the insurance industry had been regulated relatively lightly. In the view of the new consolidated regulator, this was unsatisfactory. APRA's Executive General Manager, Policy, Chris Littrell argued that:

Until 2001 the Australian general insurance industry was characterised by an unsatisfactory culture of reluctant regulatory compliance by some entities, even among our largest companies. (33)

Indeed, following the HIH Insurance collapse, Littrell argued that eliminating this cultural clash was one of the key tasks the regulator faced:

As an integrated supervisor, APRA is in a position to observe the managerial differences between our regulated sectors. Banks in general are run by people who are or have been risk managers, and by people who understand that regulation has its good points. In Australia at any rate, many insurance companies have been dominated by salesmen, who often viewed regulation as something to be avoided. Having come up the career ladder by dealing with actuarial restrictions, they tended to treat regulatory requirements as another annoyance to overcome, rather than a guide to good practice. (34)

While HIH's collapse and the subsequent Royal Commission heralded the beginning of a major wave of increased regulatory activity in the insurance industry, its genesis was the foundation of APRA itself, which coupled the insurance industry with the much more highly regulated banking industry. Indeed, plans to increase regulation of the general insurance industry preceded the 2001 collapse of HIH. The Financial Services Reform Act 2001 classified most insurance as a "financial service" -- with the notable exceptions of reinsurance, health insurance and government insurance -- and required an Australian financial services licence. Financial product advice, dispensed by intermediaries not directly providing insurance, also required licences under the 2001 Act. The Act also imposed significantly increased product disclosure requirements, as well as capital and corporate governance requirements. (35)

The industry is implementing a second wave of HIH-inspired reforms, APRA Stage II, which, among other things, requires new business plans to meet future capital liabilities, annual financial condition reports, and regular external reviews.

In its submission to the Taskforce on Reducing the Regulatory Burden on Business, the Association of Superannuation Funds of Australia, claimed that since the establishment of ASIC and APRA, supervisory levies paid by superannuation funds had increased dramatically. Those of APRA's expenses related to superannuation have grown, even though the number of superannuation funds themselves has decreased significantly. (36)

For the banking sector, a good deal of the regulatory change after the foundation of APRA was concerned with the transfer of regulatory authority from the still-existent RBA towards the new prudential regulator. (37) But the most significant regulatory change has been the adoption of the Basel II Capital accords. Australia's authorised deposit taking institutions (ADIs) will begin to adopt the Basel II Framework in January 2008.

The implementation of Basel II under the auspices of a mega prudential regulator has, for many organisations, had the effect of imposing a dramatic increase in regulatory burdens. Basel II constructs an internationally consistent framework for banking capital requirements and accounting standards. For large, internationally active banks, implementing Basel II has much important significance. However, for smaller domestically based ADIs, Basel II provides little benefit. For credit unions, whose involvement in international markets is low, the cost of implementing the framework is precipitously high. Similarly questionable benefits have accompanied APRA's uniform adoption of the International Financial Reporting Standards, which affects major, internationally active Australian banks and small domestic cooperatives such as the St Mary's Swan Hill Co-operative Credit Society alike. (38) APRA's activities illustrate clearly the perils of uniformly applying regulations that are designed for a specific type of institution.

AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION

Under Australia's "twin peaks" regulatory model, the Australian Securities and Investment Commission regulates company and financial services law for consumer, investor and creditor protection. Where APRA regulates for the viability of financial institutions, ASIC's many briefs include regulating conduct and disclosure, administering the Corporations Law and consumer protection. To do so, it administers eight separate Acts, including the Corporations Act 2001, Australian Securities and Investments Commission Act 2001, and the Insurance Contracts Act 1984.

ASIC was drawn from the Australian Securities Commission, and upon its establishment in 1998, absorbed the consumer protection responsibilities in insurance and superannuation of the ISC. It also drew consumer protection responsibilities in finance from the Australian Competition and Consumer Commission, replicating Section 52 of the Trade Practices Act in the ASIC Act. Further, ASIC absorbed the consumer protection responsibilities of the Australian Payments Systems Council and financial sector industry codes of conduct. (39) In 2005–06, ASIC had regulatory responsibility for 1.5 million corporations and 4,415 financial services businesses. (40)

ASIC's growth has been the most marked of the economic regulators. Since 1999, the regulator's annual real appropriations have increased by 93 per cent. In that time, more than 200 extra staff were hired, growing from 1,221 to 1,471.

Regulatory agencies are reluctant to divulge the resources dedicated to different aspects of their operations, but the 2005–06 Annual Report provides a breakdown of ASIC's staff operations. (See Table 3.)

Table 3: ASIC staff by team, 2005-06

| Team | Role | Number |

| Enforcing the law | Investigate and act against misconduct | 373 |

| Protecting consumers | Protect consumers | 100 |

| Promoting compliance | Ensure companies and licencees comply with the law | 187 |

| Regulatory work | Set ASIC policy on regulating markets and business | 137 |

| Operations | Company data, insolvency, IT and HR | 480 |

| Finance | Finance, risk, knowledge management, corporate services | 117 |

Source: ASIC Annual Report, 2005-06

According to publicly available data, regulation and enforcement consume between 50 and 60 per cent of ASIC's staff numbers and finances, a proportion which has increased since its founding. (41) The categories that ASIC uses to classify its activities could be misleading -- nevertheless, it is notable that the development of regulatory policy, that is, changes in regulatory policy, employs more than 100 full-time staff.

ASIC has overseen a rapid and comprehensive overhaul of corporate governance law under the Corporate Law Economic Reform Program (CLERP). Changes to Australian's corporate law under CLERP have spanned nearly a decade, so far comprising:

CLERP 1-5: Corporate Law Economic Reform Act 1999, covering fundraising, director's duties, takeovers and accounting standards.

CLERP 6: Financial Services Reform Act 2001, covering Wallis Commission reforms.

CLERP 7: Corporations Legislation Amendment Act 2003, covering lodgement and compliance procedures.

CLERP 9: Corporate Law Economic Reform Program (Audit Reform & Corporate Disclosure) Act 2004, covering the regulation of corporate governance.

The continuous reform of the CLERP decade is set to continue: The Federal Government released three discussion papers on corporate law and compliance in March 2007. (42)

Chart 13: ASIC, Staff and Annual Appropriations, 1999-00 to 2007-08

Source: Staff: ASIC Annual Reports. Appropriations: Commonwealth Budget Papers

The rapid, comprehensive change in corporate law under the continuous process of CLERP, as well as the Wallis Inquiry-era reforms which inaugurated ASIC, have been matched by the regulator's use of legal instruments to modify the Corporations Act 2001. Since 2002, ASIC has issued more than 380 class orders, which materially alter the make-up of corporate law. (43) Indeed, the Association of Superannuation Funds of Australia argues that ASIC's reliance on instruments such as class orders has been a major cause of the increased complexity of corporate regulation in the last decade. (44)

The gains from the expanding reach of regulatory intervention in the structure of the firm are uncertain. Prominent corporate collapses have been a regular feature of Australian economic history since before Federation. (45) There is, however, little evidence to suggest that the dramatic increase in corporate, securities, financial and banking regulation that followed the wave of corporate collapses in the late 1980s has had any significant impact on subsequent collapses.

There is a very real likelihood that the excessive restraints placed upon corporate form and function, particularly at the executive and upper management level, can have a detrimental effect on entrepreneurial activity. Regulatory micro-management places a significant burden upon innovative practices and structures. It also imposes substantial costs upon firms. For instance, regulatory measures which attempt to foster "compliance culture" by imposing personal legal liability for business decisions upon executives reduce the incentive to take up those senior management positions, and raise the salaries of those who do. (46)

As with all tax and regulatory burdens, firms try as hard as possible to pass these costs on to the consumer. It is indicative that an August 2006 CPA Australia survey found that, in the view of those surveyed, the overwhelming beneficiaries of CLERP 9 auditing reform processes were regulators and auditors. (47)

Chart 14: ACCC, Staff and Annual Appropriations, 1998-99 to 2007-08

Source: Staff: ACCC Annual Reports. Appropriations: Commonwealth Budget Papers

AUSTRALIAN COMPETITION AND CONSUMER COMMISSION

The Australian Competition and Consumer Commission (ACCC) was also conceived as a national functional regulator for Australian competition and consumer regulation. The 1993 Hilmer Committee wrote that it:

...started from the proposition that competition policy across all Australian industries should be desirably administered by a single body... As well as the administrative savings involved, there are undoubtedly advantages in ensuring regulators take an economy-wide perspective and have sufficient distance from particular industries to form objective views on often difficult issues. (48)

Before the creation of the ACCC, the Australian Trade Practices Commission (TPC) monitored and enforced competition regulation under the 1974 Trade Practices Act. The Prices Surveillance Authority administered the Prices Surveillance Act 1983, focusing on the abuse of market power. (49) In 1995, the Trade Practices Commission and Prices Surveillance Authority were folded into the newly-created ACCC to administer the Trade Practices Act. In 1997, the telecommunications regulator, AUSTEL, was abolished and responsibility for telecommunications-specific competition regulation transferred to the ACCC. (The responsibility for technical and standards regulation for the telecommunications industry was moved to the Australian Communications Authority, now the Australian Communications and Media Authority.)

In 2005, the Australian Energy Regulator was established, as an independent but constituent part of the ACCC. In practice, the AER will operate largely as a section within the ACCC. (50)

After its assumption of telecommunications regulation, the ACCC has grown from a staff of 359 in 1999 to 596 in 2006 -- a 66 per cent increase. The agency's budget has more than doubled.

In 2005–06, the ACCC was involved in 53 litigation proceedings, and accepted 54 enforceable undertakings from firms. (51)

Compared with APRA and ASIC, the ACCC has overseen a relatively stable regulatory environment, at least since 1997. Some changes are, however, worth noting. In 1998, the regulator lost some jurisdiction as responsibility for misleading and deceptive conduct in financial services was transferred to ASIC. However, ASIC has since referred the responsibility for health insurance back to the competition regulator. The ACCC was given responsibility for price monitoring and price "exploitation" during the transition to the New Tax System, which may account for the sharp increase in the growth of staff in the 1998–2000 period. This increase in agency size has, tellingly, been sustained since those powers expired.

Warren Pengilley has described the omnibus role of the ACCC as "educator, policymaker, prosecutor, advocate, adjudicator, executioner and arbitrator". (52) Elsewhere, he noted that

[Regulatory activity] ...resembles the attitude of the Soviet Navy to the North Sea. When the Soviet Navy does not know what to do with its submarines' spent nuclear fuel, it simply throws it into the North Sea without much consideration for the long-term effects of its action. We have done much the same in this country in relation to regulation. When we have some sort of an economic or pricing problem, we simply throw it to a regulator to fix without much consideration of the long term effects of what we are doing. (53)

THE REGULATORY AGENCY AS A

SOURCE OF REGULATORY GROWTH

BUREAUCRACIES GROW

The growth of regulatory agencies can be explained in a number of ways. For example:

- As the volume and complexity of regulation grows, the cost and expertise required to administer it grows similarly.

- There may be a political desire to provide extra resources for increased regulatory activity. The voter reaction to a corporate collapse or scandal may lead politicians to "beef up" the resources of the financial regulator, regardless of the efficacy of doing so.

These explanations locate the cause of agency expansion outside the agencies themselves, and depict the regulator as a passive recipient of budget and resource decisions made by directly elected politicians.

However, further explanations of bureaucratic behaviour derived from the public choice school help flesh out some other sources of agency growth. Regulatory agencies differ in many important respects from traditional bureaucracies, but they are influenced by many of the same incentives and share many of the same structures. The model of bureaucratic growth provided by public choice theory can be usefully applied to independent regulatory agencies. After all, regulators are, like bureaucracies, non-profit organisations financed by appropriations, rather than the sales of output. Similarly, bureaucracies and regulators are motivated not by the profit-maximisation that characterises private industry, but by discretionary budget maximisation. (54)

As a consequence, regardless of any increase in regulation, we should expect regulators, acting as bureaucracies, to expand their discretionary budgets accordingly. Agency growth can, at least in some part, be caused by the agency itself.

Jurisdictional growth can also encourage agency expansion. Empirical evidence suggests that bureaucratic budget maximisation is partly dependent on the size of the jurisdiction administered. In small jurisdictions, it is difficult to conduct public policy that favours a minority, as voters -- or regulated firms with political capital -- are able to inform themselves about that policy at a lower cost. In larger jurisdictions, however, voters and firms are constrained both by the costs of acquiring information and by the lower possibility that doing so could materially effect the policy. (55) Larger jurisdictions also increase the cost of moving away from the jurisdiction -- the bureaucracy effectively asserts a monopoly power over those it administers.

Two major driving forces have led to a jurisdictional expansion of regulatory agencies. The first is the centralisation of regulatory agencies. Agency consolidation has been made possible by moving regulatory jurisdictions from the States to the Commonwealth -- for example, the Wallis-era reforms eradicated the State-based State Supervisory Authorities in favour of federal regulators.

The second is the transition from institutional regulation to functional regulation. Functional regulation can be usefully seen as a jurisdictional expansion, as regulators focus not on single industries, but on broad categories of marketplace activity. This expansion in regulatory scope is just as much a jurisdictional expansion as a geographic one.

REGULATION EXPANDS

Former British Prime Minister Tony Blair has nominated a tendency towards greater risk-aversion by regulators, legislators, and the general public, as a source of increased regulation.

In my view, we are in danger of having a wholly disproportionate attitude to the risks we should expect to see as a normal part of life. This is putting pressure on policymaking [and] regulatory bodies ... to act to eliminate risk in a way that is out of all proportion to the potential damage. The result is a plethora of rules, guidelines, responses to "scandals" of one nature or another that ends up having utterly perverse consequences. (56)

The notion of "risk society" that Blair draws upon describes a society "increasingly preoccupied with the future (and also with safety), which generates the notion of risk". (57) A "risk society" is not a society that is more hazardous -- rather, it reflects a preoccupation with potential hazards and a desire to manage them. This focus on risk transmits, at least in a democratic system, a similar preoccupation with managing it in the political class. As Blair has argued, the risk society is a society increasingly dependent on regulation as the panacea to its ills. The risk society is also one in which the sheer volume of regulation creates a correspondingly large volume of unintended public policy consequences.

But Blair's description of the regulatory expansion attributable to external democratic factors also ignores existing and potential internal sources of regulatory growth. Inherent in regulatory activity is its tendency to expand into new areas. Increased regulation is a consequence of a systemic bias towards increased regulatory activity. Regulators are biased towards expansive interpretations of their jurisdiction, levels of excessive risk, the "immorality" of certain forms of corporate conduct, and so on.

Regulation expands both vertically and horizontally. (58)

Vertical regulatory expansion

Regulation expands vertically, that is, deeper into the affairs of the regulated firms, as the regulator attempts to gauge how compliant firms are, or ascertain whether there are new opportunities for regulation.

As firms and individuals deal with the introduction of new regulation, they gather knowledge about its specifics. And, as profit-maximising entities, they endeavour to avoid the costs of the new regulation by technological, process, or structural innovation. In response, the regulator, interpreting these actions as a failure of the regulatory framework, endeavours to expand its jurisdiction to cope.

Edward Kane views the relationship between regulator and firm as a continuous game of cat and mouse:

Market institutions and politically imposed restraints reshape themselves in a Hegelian manner, simultaneously resolving and renewing an endless series of conflicts between economic and political power. The approach envisions repeating stages of regulatory avoidance (or "loophole mining") and re-regulation, with stationary equilibrium virtually impossible. (59)

The result of this game is a spiralling volume of regulation and a diversion of effort away from economically beneficial innovation to regulation-avoiding innovation. In a complicated regulatory framework, there is just as much scope for entrepreneurial activity focused on regulatory gamesmanship as entrepreneurial activity focused on satisfying consumer preferences. Firms cannot passively accept the increased costs caused by regulation, and so engage in strategies to avoid those costs. Regulators are reluctant to let the avoidance slide because avoidance threatens their bureaucratic turf. Kane describes regulators as defenders of their jurisdictions by noting that regulatory agencies are keenly aware that "an unchallenged regulatory circumvention rapidly earns squatters' rights. As a consequence, and frustrated by their seeming ineffectiveness, regulators are tempted to "shore up" the existing suite of regulation with as much added regulation as they have the legal power to enact.

Furthermore, regulators have an incentive to act quickly, rather than effectively. This political imperative can lead them towards over-regulation or over-enforcement.

Horizontal regulatory expansion

Regulation also expands horizontally, to encompass a broader array of firms whose activities might parallel the activities of those in the original jurisdiction. Such expansion is partly the consequence of similar expansion in the economy.

For example, competition law is now applied to digital services, a market not envisioned by the policy-makers who drafted the original Trade Practices Act. As Clyde Wayne Crews argues:

Agencies face overwhelming incentives to expand their turf by regulating even in the absence of demonstrated need, since the only measure of agency productivity -- other than growth in its budget and number of employees -- is the number of regulations. (60)

So in many cases, it is likely that the regulatory agencies themselves are, at least in part, responsible for the expansion of regulation across the economy -- a conclusion perhaps borne out by the regular appeals by regulators for expanded power and jurisdiction. (61) Regulators act as stakeholders within their own jurisdictions just as much as any firm, consumer group or NGO does. A range of other (more personal) factors can influence the regulator towards lobbying for increased regulation, including ideological preference, or a hostile relationship to regulated firms.

Furthermore, their nominal independence from the political process and from the economic interests of those they regulate gives them substantial public authority to comment and recommend legislative change. A warning may perhaps be sounded here about the possibilities of a reverse regulatory capture; that is, capture of the legislator by a regulator determined to expand its jurisdiction or scope. The expertise claimed by regulators within their jurisdictions provides them with a strong platform to recommend regulatory changes which increase their own powers.

"Arm-twisting" tactics can also be used to expand the powers of the regulator, by manipulating firms to exceed the legal requirements for compliance.

Regulatory spread is often the result of a concerted effort by the regulator itself to expand its powers in order to fulfil its original purpose, or at least what it considers to be its original purpose. The legislative imposition of greater regulation can be easily tracked through published indices of consolidated legislation and subordinate legislation, but the creeping expansion of a regulator's jurisdiction and power is more obscure.

Both the legislator and the regulator, for different but often overlapping reasons, add to the burden of regulation upon the economy.

CONCLUSION

Regulation is not only a drain on economic efficiency and activity. The increase in regulatory activity and the consolidation of regulatory responsibility into "mega-regulators" raise a number of political governance questions -- as regulators hold increasing power over the economy, their activity takes on a political dimension.

Ronald Reagan's 1976 criticism of the undemocratic power of regulatory and bureaucratic agencies in the United States applies just as well to Australia in 2007 when he argued that:

We are governed more and more by people we never elected, and who can't be turned out of office by our votes and who want more power than they ever have. (62)

Regulatory agencies have presided over the most intense period of regulatory and legislative activity in Australian history. This position gives them enormous influence -- for which they are largely separate from the traditional chains of democratic accountability. Furthermore, as we have seen, this independence has the capacity to encourage regulatory growth and expansion, increasing the burden on the economy.

To mitigate the growth of excessive economic intervention in the short term, legislation needs to be more carefully drafted to be clear about its objectives, the type of behaviour that the regulation is intended to target, and, importantly, the objective principles guiding the need for, and conduct of, the regulation. These may be obvious requirements, but they are not always met. The Productivity Commission found that the National Access Regime, as innovative and imposing a regulatory mechanism as could be imagined, failed on all of these counts. (63)

To stem the increase in regulation-making -- and to ensure what regulation is made is as effective and efficient as possible -- Alan Moran has recommended a number of requirements for new regulations:

- Require a review to ensure the new regulation is fully consistent with the letter and spirit of the freedom of inter-state commerce provisions of the Constitution.

- Introduce the regulation under a two stage process approach: the first simply setting out the issues in a dispassionate and non-committal manner and the second seeking comment on the agency's preferred approach.

- Require an independent analysis to verify that the regulation is merited. This might be a scientific review in the case of measures mooted that guard against health or environmental externalities. And it may use formalised and independent economic analysis to review alleged economic benefits from an externality.

- Establish disciplines that ensure the regulatory burden does not increase. In this respect a useful approach would be that of the UK Prime Minister's direction to the Better Regulation Task Force to look at:

- First measuring the administrative burden, then setting a target to reduce them (the Dutch approach); and

- A "one in, one out" approach to new regulation, which forces a prioritisation of regulation and its simplification and removal. (64)

But while regulation dominates economic life, it is nonetheless a specific problem with a larger cause -- the extended reach of government into the economy. Concerns about the manipulation of firms by regulators or the growth of regulatory power are more generally symptoms of interventionist government.

Unfortunately, on this ultimate point, there can be no "silver bullet" solution. The "one in, one out" approach may slow the growth in regulation, but achieve no overall reduction of the burden and the costs. Independent analysis, greater and more structured consultation processes and increased rigour to ensure that new regulations are constitutional will similarly do little to increase economic freedom.

As regulation is first and foremost a political act, the problem of regulatory expansion ultimately requires a political solution. A reduction of regulation and regulatory activity is a challenge which requires a concerted effort from regulators and legislators alike.

Elected representatives need to be cognizant not only of the economic and social impact of the vastly expanding body of regulation, but also of the impact it has on political governance and the dispersion of power in Australia's democracy.

REFERENCES

1. Ian Turnbull, "Plain Language and Drafting in General Principles", April 1993.

2. Rethinking Regulation: Report of the Taskforce on Reducing the Regulatory Burden on Business, January 2006.

3. Australian Construction Industry Forum, Submission to the Australian Government Regulation Taskforce, November 2005.

4. pers. comm.

5. Insurance Council of Australia, Submission to the Australian Government Regulation Taskforce, November 2005.

6. Glenda Korporaal, "Coping With the Collapse", Charter, November 2006.

7. Credit Union Industry Association, Submission to the Taskforce on Reducing the Regulatory Burden on Business, December 2005.

8. Business Council of Australia, Submission to the Taskforce on Reducing the Regulatory Burden on Business, December 2005.

9. Australian Bankers Association, Submission to the Taskforce on Reducing the Regulatory Burden on Business, November 2005.

10. Many of these are due to the complex regulatory framework under which the telecommunications sector is governed, but it is worth noting that more than 100 are from quasi-regulatory agencies such as the Australian Communications Industry Forum. Telstra also notes that it provides the government with an estimated 486 reports annually -- a total of 162,000 pages. The company has, to contextualise that figure, noted that this would be the equivalent of 163 editions of Tolstoy's War and Peace. See "The regulatory paperwork mountain", Now We Are Talking, Facts & Figures.

11. Telstra Corporation Limited, Submission to the Australian Government Regulation Taskforce, November 2006

12. Australian Chamber of Commerce and Industry, Holding Back the Red Tape Avalanche: A Regulatory Reform Agenda for Australia, Position Paper, November 2005.

13. Richard J. Wood (ed.), Impact and Outcome of Regulation on the Economy, May 2005.

14. Insurance Council of Australia, Submission to the Australian Government Regulation Taskforce, November 2005.

15. Richard J. Wood, Paperburden costs of economic regulation of the gas and electricity supply industry, Submission to the Productivity Commission, Energy Issues Paper 29, November 2003.

16. Gary Banks, "The good, the bad and the ugly: economic perspectives on regulation in Australia". Address to the Conference of Economists, Business Symposium, Hyatt Hotel, Canberra, 2 October 2003.

17. Productivity Commission, Regulation and its Review, 2004-05, Annual Report Series, 2005.

18. Victorian Competition and Efficiency Commission, The Victorian Regulatory System 2006: Quantitative Final Data, 2006.

19. Victorian Competition and Efficiency Commission, The Victorian Regulatory System 2006, Annual Reports, various.

20. Australian Prudential Regulatory Agency, "APRA and the Financial System Inquiry", Working Paper, January 2000.

21. Di Thomson and Malcolm Abbott, "Australian Financial Prudential Supervision: An historical view", Australian Journal of Public Administration, vol. 59, no. 2, June 2000.

22. RC Merton and Z Bodie, "A conceptual framework for analyzing the financial environment" in The Global Financial System: a Functional Perspective, Harvard Business School, Boston, 1995.

23. Colin Beardsley and John O'Brien, "The Financial Services Reform Act 2001: Impact on systemic risk in Australia", ICMA Centre Discussion Papers in Finance, DP2005-12.

24. Mervyn K Lewis, "The Wallis Inquiry: its place in the evolution of the Australian financial system", Accounting Forum, vol. 21, no. 2, 1997.

25. Bijit Bora and Marvyn K Lewis, "The Australian Financial System: Evolution, regulation and Globalization", Law and Policy, vol. 28, 1997.

26. Financial System Inquiry Final Report, March 1997.

27. Caner Bakir, "Who needs a review of the financial system in Australia? The case of the Wallis Inquiry", Australian Journal of Political Science, vol. 38, no. 3, 2003.

28. Australian Financial Review, 14 March 1996

29. The New South Wales Financial Institutions Commission (FINCOM), the Victorian Financial Institutions Commission (VicFIC), the Registrar of Financial Institutions (N.T.), the Western Australian Financial Institutions Authority (WAFIA), the Queensland Office of Financial Supervision (QOFS), the South Australian Office of Financial Supervision (SAOFS), Registrar of Financial Institutions (A.C.T.) and the Tasmanian Office of Financial Supervision (TOFS).

30. Australian Prudential Regulatory Agency, "APRA and the Financial System Inquiry", Working Paper, January 2000.

31. APRA, Commonwealth Regulatory Plans, 2001–2006.

32. APRA/ASIC Working Group Status Report, 5 February 2007.

33. Charles Littrell, "General insurance regulation: The Australian experience" 2 December 2002.

34. Loc. Cit.

35. Allens Arthur Robinson, Annual Review of Insurance Law, 2002.

36. Association of Superannuation Funds of Australia, Submission to Taskforce on Reducing the Regulatory Burden on Business, December 2005.

37. See, for instance, the Financial Sector (Collection of Data) Act 2001, which came into effect in July 2002.

38. Credit Union Industry Association, Submission to the Taskforce on Reducing the Regulatory Burden on Business, December 2005.

39. Jillian Segal, "ASIC -- The new regulatory regime". Keynote address to the Australian Association of Permanent Building Societies, 30 April 1999.

40. ASIC, Annual Report, 2005–06.

41. Helen Bird, Davin Chow, Jarrod Lenne and Ian Ramsey, "ASIC Enforcement Patterns", Research Report, Centre for Corporate Law and Securities Regulation, 2003; ASIC Annual Reports.

42. "Insider Trading -- Position and Consultation Paper"; Review of the Operation of the Infringement Notice Provisions of the Corporations Act 2001; Review of Sanctions in Corporate Law.

43. ASIC website.

44. Association of Superannuation Funds of Australia, Submission to the Taskforce on Reducing the Regulatory Burden on Business, December 2005.

45. Trevor Sykes, Two Centuries of Panic: A History of Corporate Collapses in Australia, Sydney, Allen and Unwin, 1988.

46. Australian Bankers Association, Submission to the Taskforce on Reducing the Regulatory Burden on Business, November 2005.

47. CPA Australia, Perceptions of Audit Reform -- Impact on auditing and public confidence: Survey Findings, August 2006.

48. Independent Committee of Inquiry into Competition Policy in Australia, 1993.

49. Prices Surveillance Authority, Submission to National Competition Policy Review, February 1993.

50. Ed Willet, "The AER and its 'fit' with the ACCC model", Trade Practices Workshop, 23 July 2006.

51. ACCC, Annual Report, 2005-06.

52. Hansard, House of Representatives Standing Committee on Economics, Finance and Public Administration, Thursday 23 August 2001.

53. Warren Pengilley, "Competition regulation in Australia: A discussion of a spider web and its weaving", Competition & Consumer Law Journal, vol. 8, no. 3, 2001.

54. See, generally, William A Niskanen Jr, Bureaucracy and Public Economics, Edward Elgar Publishing, England, 1994.

55. David CL Nellor, "Public bureau budgets and jurisdiction size: An empirical note", Public Choice, no. 42, 1984.

56. Tony Blair, "Common sense culture not compensation culture". Speech to the Institute of Public Policy Research, 26 May 2005.

57. Anthony Giddens, "Risk and Responsibility", The Modern Law Review, vol. 62, no. 1, 1999.

58. This description of regulatory expansion as "vertical" and "horizontal" is drawn from Warren Pengilley, "Competition regulation in Australia: A discussion of a spider web and its weaving", Competition & Consumer Law Journal, vol. 8, no. 3, 2001.

59. Edward J Kane, "Accelerating Inflation, Technological Innovation, and the Decreasing Effectiveness of Banking Regulation", The Journal of Finance, vol. 36, no. 2, 1981.

60. Clyde Wayne Crews, "No Regulation without Representation: A snapshot of the Federal Regulatory State from Ten Thousand Commandments 2005", Monthly Planet, Competitive Enterprise Institute, 12 October 2005.

61. Pengilley, op. cit.

62. Ronald Reagan, quoted in Steven F. Hayward, "Reagan and the Historians", Claremont Review of Books, vol. 7, no. 4, Fall 2007

63. Gary Banks, "Competition regulation of infrastructure: getting the balance right". Presentation to the IIR Conference, National Competition Policy Seven Years On, 14 March 2002.

64. Richard J. Wood, "Impact and Outcome of Regulation on the Economy". Address to the Monash Law School's Rethinking Regulation Forum, 15 November 2006.

No comments:

Post a Comment